Global| Dec 19 2016

Global| Dec 19 2016IFO Heads Higher Again

Summary

The IFO survey shows pretty much across-the-board sector increases in December (the retail index is unchanged). Except for construction, all sectors have risen by more in the last four months than they have over the last 12 months. [...]

The IFO survey shows pretty much across-the-board sector increases in December (the retail index is unchanged). Except for construction, all sectors have risen by more in the last four months than they have over the last 12 months. There is definitely some sort of revival in the German economy.

The IFO survey shows pretty much across-the-board sector increases in December (the retail index is unchanged). Except for construction, all sectors have risen by more in the last four months than they have over the last 12 months. There is definitely some sort of revival in the German economy.

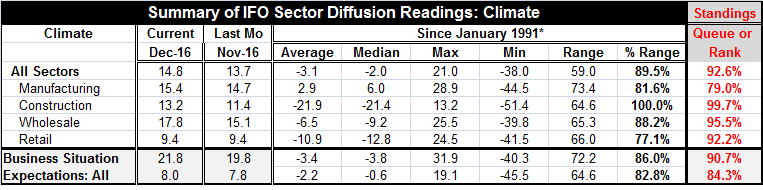

Activity performance remains solid and strong. The diffusion climate readings (see Table below) are extremely strong across most sectors while expectations are still quite strong but a step or so behind the performance of the business situation index. Expectations have an 84th percentile standing while the business situation has a 90th percentile standing.

By sector, the diffusion climate readings show ranking by all sectors in the top 10% of their historic queues of data with the exception of manufacturing having a still-firm 79th percentile standing. Among sectors manufacturing has made the second largest gains in terms of diffusion index points over the last four months; wholesaling has made the most, followed by manufacturing, construction and retailing, in that order.

The chart of the IFO sector indices is particularly interesting; I have taken it back to the start of the IFO survey. It shows clearly how the German economy has come to dominate the EMU after a rougher start. The IFO index, except for the very start which marked the very earliest days of German reunification, shows readings prior to 2006 had been oscillating in a much lower band than they are now. Since 2006 the German gauges have generally occupied much higher ground than they did before that date and they do so on a very consistent basis, except for the period when Germany was hit by the effects of the global recession and financial crisis. The current conditions index is particularly striking for its recent consistent high readings. There are only three previous episodes of current conditions doing as well or better than they are now: 2010-2011, 2006-2007 and 1991. Expectations are somewhat less skewed to high readings than the other gauges, but that index too is higher after 2005 than it had been before as a general statement of conditions.

This month's readings take the IFO up to particularly strong readings. The reading for current conditions has run up to its strongest reading since late 2011, a five-year span. Expectations were last higher in October of this year; otherwise they were last higher in April 2014.

The diffusion indices in the table and the levels indices in the chart both show strong momentum in place concentrated in the current performance and buttressed by solid to strong expectations. The German economy shows no sign of any vulnerability. And while inflation maybe creeping up, it is around the 1% in Germany and well below target for the EMU as a whole.

The global environment is touch and go, however. China's outlook for the year ahead is for growth of just of 6.5%. This was just announced by its Academy of Science and would be the slowest growth for it in the last 25 years. Japan announced a trade surplus that was short of expectations as it posted a drop in both exports and imports. U.S. data have been more upbeat, but they are still mixed with U.S. consumer and income data having slowed down and industrial output being weak despite some reported step up in PMI-type survey data. Globally, nothing seems to be kicking into gear. The Bundesbank, however, is looking for some pick up in Germany and the IFO is looking for a mild step up in German activity as well. On balance, there is a whiff of progress in the air but nothing too tangible just yet.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief