Global| Feb 01 2016

Global| Feb 01 2016Global Manufacturing PMIs Continue Weak

Summary

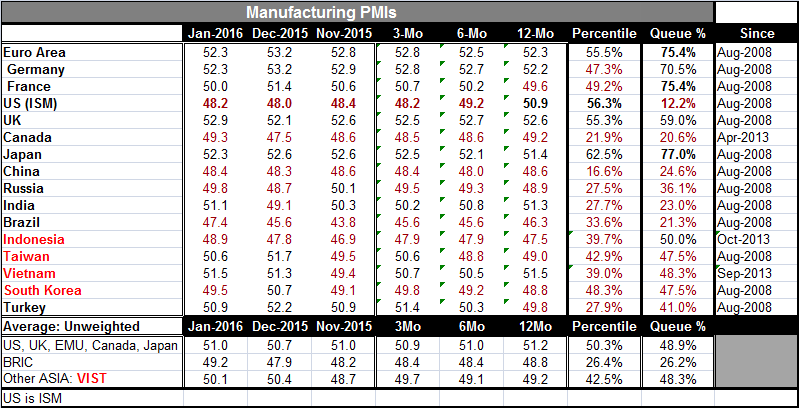

Among the manufacturing PMIs listed in the table, 7 of 16 of them reside below their breakeven diffusion value of 50. However, even more of them appear to be even weaker when simply expressed as their percentile rank or standing in [...]

Among the manufacturing PMIs listed in the table, 7 of 16 of them reside below their breakeven diffusion value of 50. However, even more of them appear to be even weaker when simply expressed as their percentile rank or standing in their historic queue of data. For example, 10 of 16 readings have standings in their respective historic queues below their historic midpoints (which occur at 50%). There are six of these that stand below their respective 40th percentile mark. The BRICs as a whole find their diffusion value is a simple average of 49.2, but the average of their members' respective queue ranking is 26.2%. As a group, this important batch of countries has been weaker only about one-third of the time. For other Asia, a group consisting of Indonesia, Taiwan, Vietnam and South Korea, the diffusion ranking is at 50.1, barely showing expansion. The queue standing is not much different, but at 48.3 this important group of Asian economies is on average below its members' average midpoint.

Among the manufacturing PMIs listed in the table, 7 of 16 of them reside below their breakeven diffusion value of 50. However, even more of them appear to be even weaker when simply expressed as their percentile rank or standing in their historic queue of data. For example, 10 of 16 readings have standings in their respective historic queues below their historic midpoints (which occur at 50%). There are six of these that stand below their respective 40th percentile mark. The BRICs as a whole find their diffusion value is a simple average of 49.2, but the average of their members' respective queue ranking is 26.2%. As a group, this important batch of countries has been weaker only about one-third of the time. For other Asia, a group consisting of Indonesia, Taiwan, Vietnam and South Korea, the diffusion ranking is at 50.1, barely showing expansion. The queue standing is not much different, but at 48.3 this important group of Asian economies is on average below its members' average midpoint.

Whether we look at the Europe (EU or EMU), at the U.S. or at China or Asia as a whole, the answer remains clear that early in 2016, the global manufacturing sector remains a mess of weakness. The BRICs are exceptionally weak because the strong dollar has crushed commodities and that has hurt them disproportionately. Brazil and Russia are being hurt by commodity price weakness and extreme exchange rate weakness. China, of course, has its own issues as it makes slow progress to a more services and consumption oriented economy. China also has developed a series of other problems ranging from extremely high debt levels to extreme pollution. China has reacted with its own extreme crack down on what it is calling graft, but this seems to be just a way to constrain and keep in the place those who had profited most under the old system. In China, nearly everyone with money wants to flee. You see it in China's exchange rate and in its extremely rapid drawdown and selloff of reserves. And yes, I am aware that I am using the word `extreme' a lot. It is because that is what characterizes China. There is little in moderation except the pace of the policy switch. And there is simply no way to do that rapidly. Moreover, China has brought so many people into its developed portion of the economy that too many people are intrinsically agrarian and do not understand city living let alone working in a more consumptive service sector economy. China's policy switch will take time.

The global glut in manufacturing seems to be understood by few. China's currency depreciation will not fix the glut of its firms, nor will euro weakness or yen weakness for that matter. Japan for its part has its firms doing most of their production outside Japan so the yen's value is not such a hot potato for it. In fact, Japan would prefer that the yen not weaken any more. In the U.S., the Fed seems to have lined up its impressive stable of economists and still not reached the right conclusion. Tightening policy will only make the dollar stronger and that will push the Fed farther from its objective of full employment and of 2% inflation. Yet, the Fed, as preparing for FOUR rate hikes (and many more after that), continued to speak of the dollar's strength as a temporary phenomenon. It's like Sir Isaac Newton dropping an apple, fully understanding gravity now, yet expecting that the Apple THIS TIME is not going to fall. Of course, in the U.S. stock market, even Apple is falling and it's not gravity at work.

Monetary policy at the Fed has been curious and curiouser. The Fed is unwilling to see the global glut in output and productive capacity as a worldwide dominate thing. It continues to believe that historic U.S. centric statistical models will carry the day. This is, in some sense, the Fed thinking that the U.S. labor market is going to dominate the global output glut. On the face of it, it is preposterous, but it is the only conclusion consistent with how the Fed is acting and preparing to make policy.

In Europe, the ECB is planning (it seems) to do more but always waiting and talking about it before doing anything. The Fed's and BOE's successes with QE are not being emulated because Europe and Japan have tried theses polices too late in the cycle with rates already having fallen low. Instead, now they are dabbling in the black art of negative interest rates, a real double-edged sword if ever there was one.

Fiscal policy is mostly shackled. In Europe, the Maastricht (pronounced: Mass-Trick) criterion keeps fiscal policy in check. In Japan, a huge debt-to-GDP ratio has handcuffed fiscal tools. In the U.S., there will be some let up in fiscal restraint this year, but probably not much. Fiscal policy will not be a real avenue of stimulus. Even China that has now used such huge amounts of domestic debt may find further reliance on debt as not useful. Like any monetary or fiscal tool, some success can be expected with a tool used in moderation, but excessive use of any of these tools can render them broken.

As a result, the ongoing global glut will be with us for some time. The Fed's worry about inflation as well as its forecasts that inflation will rise of the medium term will in all likelihood be squashed. The Fed will have to recalibrate policy and save face as well. The ECB will be stuck with no policy tool that can produce any real traction. The BOJ will find the same. China's floundering will simply go on because there is no way to turn it around any faster except through the magic of `let's pretend statistics.' Let's hope China does not go there. In fact, let's pretend it won't.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief