Global| Dec 22 2015

Global| Dec 22 2015GfK Confidence Set to Rise in January in Germany

Summary

German confidence is estimated to rise by the smallest measurable amount in January 2016. While this result is less than stunning, there is little that is more surprising at the moment than the notion that German consumer confidence [...]

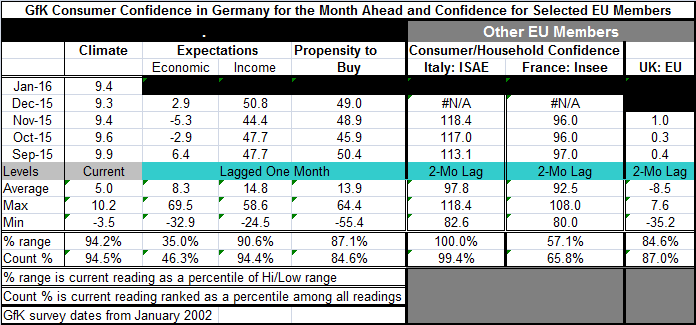

German confidence is estimated to rise by the smallest measurable amount in January 2016. While this result is less than stunning, there is little that is more surprising at the moment than the notion that German consumer confidence is going to rise, given the struggling state of the European and German economies, the desperate stimulus effort by the ECB, and the ramping up of migrant problems. Yet, that is exactly what his happening. GfK, which produces a month-ahead view of confidence in Germany, shows a tick up in confidence to 9.4 in December after four straight drops and with the last rise in German confidence in June. Germany seems to be swimming against the current.

German confidence is estimated to rise by the smallest measurable amount in January 2016. While this result is less than stunning, there is little that is more surprising at the moment than the notion that German consumer confidence is going to rise, given the struggling state of the European and German economies, the desperate stimulus effort by the ECB, and the ramping up of migrant problems. Yet, that is exactly what his happening. GfK, which produces a month-ahead view of confidence in Germany, shows a tick up in confidence to 9.4 in December after four straight drops and with the last rise in German confidence in June. Germany seems to be swimming against the current.

German confidence has not been weak for some time despite its erosion and plateauing in 2015. As a result the current level of confidence, the first rise since June, is still in the 94.5th percentile of its queue of values; it has been this high or higher only 5.5% of the time.

It is clear that despite the lagging German manufacturing sector, the influx of migrants and the commitment by Chancellor Merkel to absorb even more against the weight of public opinion, German confidence has remained resilient. Industrial confidence in December, as measured by the Ifo, stands in its 80th percentile with investor confidence as measured by the ZEW survey a bit more circumspect with expectations in their 40th percentile and current conditions in their 84th percentile. Consumers are leading the confidence parade in Germany which is quite unusual.

On component metrics that lag one month, German consumers assess the economic situation as being in its 46th percentile, below their historic median assessment. Income, however, is still assessed as being quite good with a ranking that has been higher only 6% of the time. The consumers' propensity to buy index has an 84th percentile standing, which is quite solid. Consumers continue to feel quite good on their own particulars, albeit with a nagging feeling that the overall economy is still not quite up to snuff.

Italy, France and the U.K. have confidence measures that lag by two months. But even here we see European consumers are relatively upbeat despite the lagging manufacturing sector and moderately firm services sector growth. Italian consumers rate confidence as this good or better only 0.6% of the time. The November reading for Italy, in fact, is its highest on this timeline. In France, confidence is lagging a bit with a 65th percentile reading, a reading that is more middling than it is weak. The U.K., an EU member, has a queue standing for confidence in its 87th percentile, quite robust.

Clearly consumers have been propping up growth in Europe. They continue to be upbeat about their circumstances. However, in Germany, we find undercurrents of concern about the performance of the economy. It appears that issues related to migrants in Europe simply have not had much impact on peoples' perceptions of their welfare despite all the hoopla about it and despite the terrorist attacks in Paris. Reports today chronicle migration in 2015 as having sent over 1 million displaced people to Europe. A further 3,600 are estimated to have died trying to make the journey. And so far this is having no discernible impact on measured European assessments of consumer confidence.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief