Global| Apr 24 2019

Global| Apr 24 2019Germany’s IFO Erodes

Summary

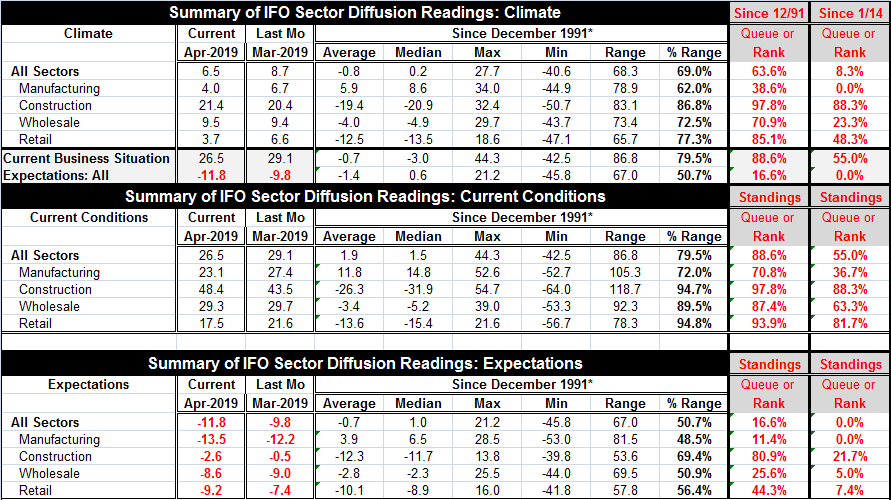

The German IFO gauge fell month-to-month to 6.5 in April from 8.7 in March in its diffusion presentation. The headline was last weaker for one month in February 2016. It was weaker for a series of four months in a row ending December [...]

The German IFO gauge fell month-to-month to 6.5 in April from 8.7 in March in its diffusion presentation. The headline was last weaker for one month in February 2016. It was weaker for a series of four months in a row ending December 2015. However, it was last persistently weaker than this in July 2013 (that was a period of 14 months consecutively). Previous to those instances, it was weaker in the period of the great recession for a period of 26 months).

The German IFO gauge fell month-to-month to 6.5 in April from 8.7 in March in its diffusion presentation. The headline was last weaker for one month in February 2016. It was weaker for a series of four months in a row ending December 2015. However, it was last persistently weaker than this in July 2013 (that was a period of 14 months consecutively). Previous to those instances, it was weaker in the period of the great recession for a period of 26 months).

The rank standing at the far right show that since January 2014, the IFO diffusion headline has been weaker only 8.3% of the time. But from a longer period back to December 1991, it has been weaker only 64% of the time. But a perusal of actual data shows that whichever time period you think is more correct for comparison the instances of the IFO index being much weaker than this were not very good economic times.

In some sense, the IFO index is at a watershed. If it recovers from this level, the economy is probably going to continue to revive. But any further slippage on the IFO gauge would cause us to have to consider the prospect of a much grimmer future.

Month-to-month two sectors improved in April. One was the still-strong and resilient construction sector whose standing is above or near its 80th percentile on a ranking over either period. The other is a one tick meager gain in wholesaling where performance is moderate-to-lackluster, depending on the ranking period one prefers for assessment. However there were sharp step backs in manufacturing (to 4.0 from 6.7) and in retailing (to 3.7 from 6.6). Manufacturing reaches a new low for its ranking in the January 2014 period while the retail ranking is at its 48th percentile for the shorter period- a ranking that is nonetheless below its historic median for that period. Retailing is still strong at its April reading on a longer period ranking even though it is only just below its median on a ranking over the January 2014 period.

The current business situation deteriorated in April to a reading of 26.5 from March’s 29.1 to an above median standing over the shorter ranking period and a relatively strong ranking over the longer period. Expectations, however, are where the problem lies as expectations standings are abysmal on either ranking metric. Concerns are for the future more than for the present.

The current sector details show strength or firmness depending on the ranking metric for all sectors except manufacturing. Manufacturing has a moderate long cycle rank and a weak below median short cycle rank at its 37th percentile. Apart from manufacturing, the current situation is solid-to-strong on either set of rankings.

Turning to expectations the summary picture changes by a lot. Construction is still strong on a long cycle rank, but it is weak on a short cycle rank. Manufacturing and wholesaling have extremely weak readings on either ranking metric. Retail is below its median on a long cycle ranking, but it is much weaker, below its 10th percentile mark on a short cycle ranking.

I offer the chart (on left) as a sort of Rosetta Stone for those who do not get the full Markit PMI database. You can see that the IFO period is much longer than the period that a generalized database offers for Markit’s PMI data. But we can also see the strong correspondence between the Markit manufacturing PMI and the IFO diffusion gauge. The comparison underscores how weak the current data are in manufacturing compared to a longer historic experience.

I offer the chart (on left) as a sort of Rosetta Stone for those who do not get the full Markit PMI database. You can see that the IFO period is much longer than the period that a generalized database offers for Markit’s PMI data. But we can also see the strong correspondence between the Markit manufacturing PMI and the IFO diffusion gauge. The comparison underscores how weak the current data are in manufacturing compared to a longer historic experience.

On balance, the IFO data are disturbingly weak. This month the ZEW data showed Germany with a worsened current reading but with improvement in its expectations. Both still had standings well below their respective medians ranked on data back to 1999. The various reports on Germany seem to be more or less in agreement about what is happening. There may be some difference on momentum as the IFO assessment is clearly weaker while the ZEW assessment is mixed. The IHS Markit assessment shows a deteriorating manufacturing sector with some evidence of a bounce in services. None of this is radically different across these reports. Germany and Europe still seem to be in a fragile period and there is no clear evidence that it is coming to an end. Today’s report from the IFO does nothing to dispel that assessment.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief