Global| Sep 24 2009

Global| Sep 24 2009Germany's IFO Continues Steady Gain; Still Pessimists Deride Result

Summary

A slower pace of improvement in September - The pace of improvement in the diffusion and headline index barometers for Germany’s IFO are slowing their rate of gain this month. After averaging increases of 3.3 points per month since [...]

A slower pace of improvement in September -

The pace of improvement in the diffusion and headline index barometers

for Germany’s IFO are slowing their rate of gain this month. After

averaging increases of 3.3 points per month since they began to turn

positive in April, this month’s headline gain in the diffusion index

was 1.6. For the expectations index, similarly, the average gain has

been 5.4 but this month the rise was a more meager 1.4 diffusion points.

CONTEXT! While the Sept gain is smaller than what

has been on average in this nascent recovery it is also true that

September’s report comes on the heels of a very strong August reading

where the headline diffusion index improved by 6.1 points and

expectations rose by 9.1 points. In the spirit of recognizing

volatility, if we average the two months, we are ahead of what has been

the average. There are in fact past experiences in this cycle that have

seen a slowdown followed by a spurt. For example in June, the IFO

expectations diffusion index soared by 7.1 points only to rise by just

1.7 points in July but then to spurt again by 9.1 points in August. So,

why make so much of a one month partial stumble?

Separating the wheat from the chaff has always been hard -

What is hard in these early recovery periods to separate volatility

from trend. In this business cycle in both in the US and in Europe

there seems to be a lot of pessimists that are eager to grasp the first

sign of bad news and to extrapolate it. I would warn against that here.

Rolling up our sleeves…the recovery trends show us -

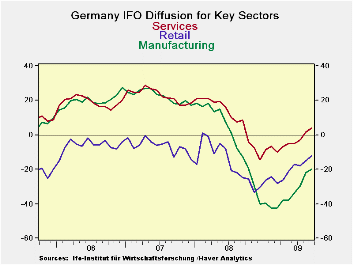

The diffusion values are somewhat more telling when looked at by

sector. Three of five sectors have had their largest in-recovery gain

in August. Even so two of those three still posted about as large gain

in September as they had in July before the August spurt. Manufacturing

is one exception to that and it still had a 2 diffusion point gain in

September after an August gain of 7.7 points. Services and wholesaling

displayed the strong resilience of spurting in August and still posting

a September value about as strong as they had before the spurt in July.

Retailing has been fickle in the recovery with its largest diffusion

gain in June followed by an outright drop in July which was then

followed by two solid-to-strong increases of more than two points in

each of August and Sept. Lastly, the construction sector is simply

erratic. In the seven months that the other indicators have been

increasing almost without fail, the construction index has dropped four

times. Among the other four sectors there is only one monthly set-back

(in retailing) for all of them.

Summing up - On balance given that the recovery

cycle is still young it is hard to look at this month’s IFO sector

recovery patterns and to become a pessimist even on the likely speed of

recovery. Recovery itself is still in train and we saw improvement in

four of five key sectors on their diffusion gauges. The pace of

recovery did slow when compared to the previous month but that month

was a spike for many sectors. When placed in context, the recovery

speed still seems to be quite good with only the one-month result to be

a harbinger of a slowdown - and we all know how dangerous it is to base

assessments on one single data observation. That the Zew index showed

the same sort of soft spot in Sept says only something about September,

not about the future. So I will remain upbeat in the wake of this

report despite the fact that the weight of opinion is on the other side

and despite the euro taking a cue to back-off after this report. The

euro back-off makes sense because the trade-weighted and inflation

adjusted euro is already so strong. Recovery will be hard to sustain if

the euro continues to advance has it has regardless of whether the

recovery has already started to slow or not.

| Summary of IFO Sector Diffusion readings: CLIMATE | ||||||||

|---|---|---|---|---|---|---|---|---|

| CLIMATE Sum | Current | Last Mo | Since Jan 1991* | |||||

| Sep-09 | Aug-09 | Average | Median | Max | Min | Range | % Range | |

| All Sectors | -18.1 | -19.7 | -9.5 | -9.9 | 17.5 | -36.1 | 53.6 | 33.6% |

| MFG | -19.9 | -21.9 | -2.2 | -0.8 | 27.6 | -42.7 | 70.3 | 32.4% |

| Construction | -25.7 | -24.0 | -29.4 | -30.4 | 0.0 | -50.1 | 50.1 | 48.7% |

| Wholesale | -12.2 | -14.5 | -14.8 | -16.3 | 23.9 | -39.0 | 62.9 | 42.6% |

| Retail | -12.4 | -14.9 | -16.1 | -15.1 | 16.2 | -40.4 | 56.6 | 49.5% |

| Services | 3.8 | 1.4 | 10.9 | 9.5 | 28.5 | -14.5 | 43.0 | 42.6% |

| * June 2001 for Services | ||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief