Global| Oct 31 2008

Global| Oct 31 2008German Retail Sales Run Soft

Summary

The German consumer has kept a stiff upper lip according to the November reading on the consumer from GfK. Still the consumer has been stiffening more than just his and her lip. The old wallet seems to have become a bit less pliable [...]

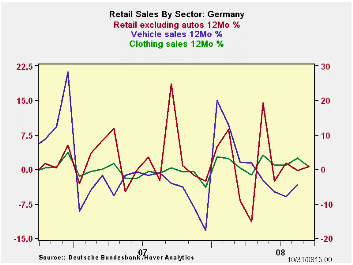

The German consumer has kept a stiff upper lip according to the November reading on the consumer from GfK. Still the consumer has been stiffening more than just his and her lip. The old wallet seems to have become a bit less pliable as Germans have tightened up on spending. Retail sales plunged in September, dropping by 2.5% and obliterating the 2.4% pop in August. The drop will still leave NOMINAL German retail sales advancing in Q3 but real ex auto German sales are shrinking in Q3 at a 0.5% annual rate.

The sequential growth rates on German nominal retail spending are very flat. The real retail sales ex auto sequential growth rates are similarly steady but at shallow negative rates of growth.

The good news for Germany is that the September drop in retail sales can be called a plunge but it only offsets the spike in August. There is nothing in the data or trends that suggest things are about to get much worse. But that does not mean that they won’t either.

| German Real and Nominal Retail Sales | QTR | |||||||

|---|---|---|---|---|---|---|---|---|

| Nominal | Sep-08 | Aug-08 | Jul-08 | 3-MO | 6-MO | 12-MO | YrAgo | Saar |

| Retail Ex auto | -2.5% | 2.4% | 0.2% | 0.0% | 0.8% | 0.8% | 0.4% | 2.2% |

| Food, Bev & Tobacco | -1.6% | 3.1% | -0.2% | 5.0% | 0.4% | 0.9% | 0.0% | 2.6% |

| Clothing footwear | 8.7% | -1.2% | 4.1% | 56.7% | 30.0% | 0.6% | 18.5% | 10.8% |

| Real | ||||||||

| Retail Ex auto | -2.3% | 1.9% | -0.1% | -2.0% | -1.4% | -2.1% | -0.6% | -0.5% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief