Global| May 29 2015

Global| May 29 2015German Retail Sales Rebound in April

Summary

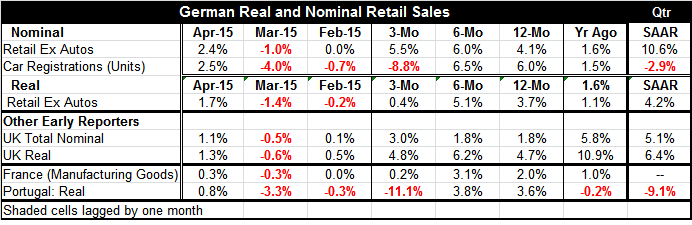

With the rebound in sales in April, trends in German retail sales show signs of stabilizing. Both six-month and year-over-year trends are starting to snake sideways at firm rates of growth. The three-month pace is still erratic. Real [...]

With the rebound in sales in April, trends in German retail sales show signs of stabilizing. Both six-month and year-over-year trends are starting to snake sideways at firm rates of growth. The three-month pace is still erratic.

With the rebound in sales in April, trends in German retail sales show signs of stabilizing. Both six-month and year-over-year trends are starting to snake sideways at firm rates of growth. The three-month pace is still erratic.

Real retail sales excluding autos are up strongly in April, rising by 1.7%. This is after two months of drops. There have been five monthly drops in German retail sales (real sales ex-autos) out of the last 12 months. The series obviously is somewhat `noisy.' But the increases do outnumber the drops and they are generally larger than the declines. That is why the broader trends are showing increases.

Auto registrations in Germany show strong and steady growth over six months and 12 months but demonstrate a sharp falloff over three months.

In the quarter to date (one month into the new, second quarter), German nominal and real sales show strength. But auto registrations are off on this measure.

Other early retail sales reporters include the U.K., France and Portugal. Each of these reports shows a sales gain in April, and all show firm and steady sales growth over six months and over 12 months. The U.K. follows up these trends with further gains over three months. France also shows sales gains over three months but a gain that is weaker. Portugal shows a sizeable drop over three months. These trends translate into solid sales gains early in Q2 for the U.K. and into a large drop for Portugal.

On balance, the consumer sector in Germany seems solid. France is showing some life. The U.K. appears to be strong as well. Portugal has posted another gain in Q1 GDP, but unfortunately it is showing some weakness in retail sales trends. With drops in two of the past three months and an outsized drop in sales in the current quarter, Portugal's success story may be opening to a less advantaged chapter.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief