Global| Apr 30 2014

Global| Apr 30 2014German Retail Sales Drop in March

Summary

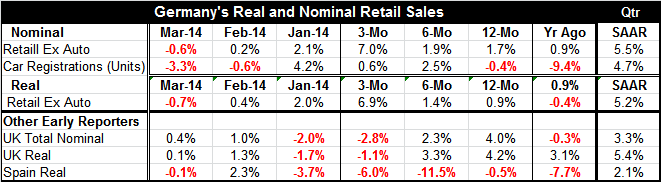

German retail sales fell by 0.6% in March after rising by 0.2% in February. Nonetheless, over three months German retail sales excluding autos are rising at a 7% annual rate on the strength of the strong gain back in January. Ex-auto [...]

German retail sales fell by 0.6% in March after rising by 0.2% in February. Nonetheless, over three months German retail sales excluding autos are rising at a 7% annual rate on the strength of the strong gain back in January. Ex-auto sales are still weak over six months and 12 months, running at under 2% annual rate on both horizons.

German retail sales fell by 0.6% in March after rising by 0.2% in February. Nonetheless, over three months German retail sales excluding autos are rising at a 7% annual rate on the strength of the strong gain back in January. Ex-auto sales are still weak over six months and 12 months, running at under 2% annual rate on both horizons.

Because inflation is low, real German retail sales are doing almost as well as nominal sales. Over three months real ex-auto retail sales are up at a 6.9% annual rate compared to 1.4% over six months and 0.9% over 12 months. That sequence of growth rates indicates acceleration, but most of that signal is really built upon the strong three-month growth rate.

Auto registrations have undergone some of the same stresses as retail sales. Current registrations fell by 3.3% in March after falling by 0.6% in February. Still, because of strong January gains, auto registrations are up 0.6% over three months. This is a deceleration from six months when sales were up at a 2.5% pace. Year-over-year car registrations are lower by 0.4%.

On the chart, retail sales year-over-year show a relatively stable pace that is somewhat less than 2%. However, as we can see over shorter periods, German retail sales growth rates have vacillated widely; the same is true for car registrations.

Among the other countries that are early reporters of retail sales, the UK shows the opposite pattern from Germany with sales up in the last two months on the back of sharp declines in January. As a result, UK retail sales, both real and nominal, are down over three months but gaining 2% to 3% over six months and in the range of 4% in both nominal and real terms over 12 months. For Spain, real retail sales fell in March by 0.1%, but they are down at a 6% annual rate over three months because of a sharp drop in January. Spanish sales are down at 11.5% annual rate over six months but down by only 0.5% over 12 months.

However, the quarterly figures show remarkable stability. The German retail sales are up at a 5.5% annual rate in the quarter with car registrations up at a 4.7% annual rate. Real Germans ex-auto sales are up at a 5.2% annual rate in the quarter. UK nominal retail sales are up at a 3.3% annual rate in the quarter, compared to real sales being up at a 5.4% annual rate in the quarter. Even Spain, with its weak three-month growth rate, shows real retail sales up at a 2.1% pace in the quarter.

The quarterly growth rates reflect growth rates calculated from an averaging process; in this calculations, we are looking at the average of sales over the current three months compared to the average over the previous three months and, of course, we take these readings four times a year in the terminal month of the quarter. The sequential growth rates (in the table) can be quite volatile because there's no averaging involved even though the growth rate periods change over the various sequences that we assess growth. Quarterly numbers, for all their variations, are still more stable that the various horizons for the monthly data. While the US surprised us with a very weak growth rate for GDP in the first quarter of 2014, it looks like Europe is in place to have fairly solid consumption to help boost growth. Even Germany, with weakness in March, is posting a solid first-quarter growth rate for retail sales. On the other hand, the UK and Spain with their dismal growth rates in January are getting over it to post positive growth rates in the first quarter. This looks like good news for first-quarter European GDP.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief