Global| Aug 06 2019

Global| Aug 06 2019German Orders Break Out of Their Torpor for One Month; Hold the Confetti

Summary

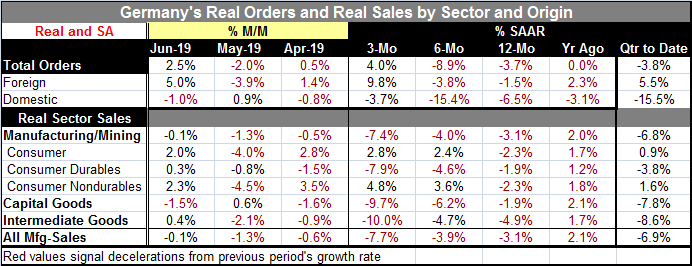

German orders jumped for joy in June, tempering a period of order weakness and declines. The rise is all on the back of 'foreign orders' that spurted by 5% one month after a 3.9% decline. That fact may temper any enthusiasm by itself. [...]

German orders jumped for joy in June, tempering a period of order weakness and declines. The rise is all on the back of 'foreign orders' that spurted by 5% one month after a 3.9% decline. That fact may temper any enthusiasm by itself. Moreover, foreign orders have run with more than 50% more volatility than domestic orders on a month-to-month basis. The last three months are just a small example of how volatile foreign orders can be.

German orders jumped for joy in June, tempering a period of order weakness and declines. The rise is all on the back of 'foreign orders' that spurted by 5% one month after a 3.9% decline. That fact may temper any enthusiasm by itself. Moreover, foreign orders have run with more than 50% more volatility than domestic orders on a month-to-month basis. The last three months are just a small example of how volatile foreign orders can be.

Temper your enthusiasm

Moreover, there may be little room for enthusiasm about the future with EU Brexit officials setting a record for keeping their word by stonewalling the U.K. as Boris Johnson keeps beating on the doors asking to renegotiate an exit deal because he does not like the one that he among others forced Theresa May to negotiate. Beyond that, there is the expanding of the trade war between the U.S. and China and that now seems destined to spread it shock waves even further as the U.S. has named China as a currency manipulator. That designation does not count for much now since the two countries already have a slew of 'tit-of-tat' tariffs in place.

Has the trade war spread to currencies?

Some people are writing that the trade war has spread to become a currency war (this is the WSJ take on it). That would be wrong. What this is fundamentally is a currency war that spread to become a trade war and now is reflecting back on currencies again. It is largely because there is no global currency value enforcement mechanism that trade imbalances have become so large and have had such staying power! Persistent trade imbalances are not part of 'free trade' nor part of a well-functioning currency system.

A systemic diagnosis

Let's look at how one can tell that the currency situation is what has primarily been what has been out of sync. (1) In a true floating rate system, currencies are supposed to move to expunge balance of payments imbalances (current account surpluses and deficits). Instead in this 'system' it has become much more likely that we can identify countries as surplus or deficit countries since exchange rates DO NOT move to rid countries of these imbalances. (2) China, a fast growing developing economy that should be importing capital to develop, is instead running a large and persistent current account surplus (exporting capital)! (3) The U.S. that is not investing heavily at all and that is a high cost country is attracting all sorts of capital inflows but only to purchase U.S. treasury paper and other financial assets not for real 'economic investment.' The U.S. is not importing capital to invest. Inflows are supporting consumption and the financing overly large government sector deficits. These perpetuate instead of eradicate the U.S. payments imbalance! The U.S. is using capital inflows to keep interest rates lower. This is hardly an 'expected' or 'textbook' result.

A nonfunctioning currency system

A nonfunctioning currency system has been at the root of the systemic burgeoning trade problems from the start. A properly functioning currency system would have caused currencies to move to re-establish equilibrium. China's currency should have moved up. The dollar should have moved down. Instead, as China and other countries interposed their government sector preferences to stoke their own export growth huge amounts of foreign exchange reserves piled up. This has been long-term currency manipulation. Had they not done that, currencies long ago would have shifted to remove the deficits that now so vex U.S. President Donald Trump. After all, free trade and comparative advantage are not supposed to combine to make specialized consumer and producer countries!

Hold the confetti

In this world, the German situation, while somewhat better on the day/month, is much more likely to be a one-off situation than a new more desirable trend. The U.S.-China dispute will spread its impact and then there will be an addition shock from Brexit unless something there shifts unexpectedly. German trends only show orders rising over three months for foreign orders and also quarter-to-date for foreign orders. Domestic German orders are still contracting on all horizons although their pace of contraction has slowed over three months.

The Global 'cold war' heats up?

The oxymoronic heading for this sector may be the perfect one to explain what is actually going on. Globally, the economy is shifting as are basic geopolitical relationships. All of these shifts are important to the economy. Donald Trump has decided against policies of appeasement and dissolved the U.S. Iran nuclear deal that the Europeans still want to cling to. The U.S. also wants Europeans to step up and pay for more of their own protection in NATO. The need to coddle them and provide a protective umbrella is over. Yet, Germany still pays the smallest amount possible to NATO and continues to prioritize creating fiscal surpluses over stepping up to provide more funding for its own defense while agreeing to increase its dependency on Russian-supplied energy. Clearly, the transition to a post Post-War period is having a hard time. The U.K.'s own assertion of a life independent from Europe has caused Europe to seek harsh conditions against its former WWII ally (well save Germany and for a tie Italy) that saved Europe's bacon. Europe is not grateful for that any more- or so it seems.

American first meets 'me' first everywhere else

Donald Trump's decision to put America First –in my view- simply exposes how much other countries have long been prioritizing their own interests and how quickly they have turned on the U.S. for repossessing the training wheels on their economies now that it expects them to ride a big-boy bike on their own. The U.S. has supported European and other economies long beyond their post-war period of need. It is time for everyone to stand on their own two feet. That does not mean that there are not alliances. It does not mean that old alliances need to be dissolved. Neither does it mean that those who should be grateful for a long period of being helped should turn angry when the degree of aid is reduced. America is being mindful of its own interests and its own persistent economic deficits and has become attuned to the need for addressing them. Of course, there are aging populations everywhere and everyone is feeling the same pinch. The political disharmony over direction in America itself does not make any of this easier. But neither does it make a shift to more self-sufficiency wrong for U.S. allies.

Conflict resolution

Meanwhile, it is unfortunate that the U.S. has had to take such an aggressive stand with China. But one of the realities of the more integrated world is that we all must live and work and trade together and the same rules need to apply to all. No one country can impose its sovereignty on others. But China has been that sort of trade partner. It did seize the South China Sea and has kept and fortified it despite the World Court ruling against its land grab...err sea grab. China is the 'Animal Farm' of the international community 'more equal' than everyone else. And that is no longer working. No one likes the trade war; but I can't help believing that everyone is glad that the U.S. has chosen to fight this fight so they won't have to. And it's much better to get China on the same page as everyone else than a policy of appeasement, special treatment and hope that 'this' act of appeasement, 'this grab,' will be the last one....

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief