Global| Apr 06 2016

Global| Apr 06 2016German IP Takes February Setback Without a Dent to Momentum

Summary

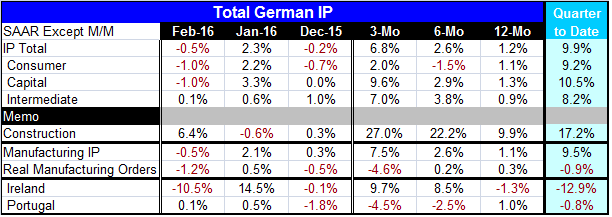

German IP fell by 0.5% in February as manufacturing IP fell at the same pace. Both series continue to demonstrate acceleration profiles in output from 12-month to six-month to three-month. IP is up at a 6.8% annual rate over three [...]

German IP fell by 0.5% in February as manufacturing IP fell at the same pace. Both series continue to demonstrate acceleration profiles in output from 12-month to six-month to three-month. IP is up at a 6.8% annual rate over three months with manufacturing IP is up at a 7.5% pace. Germany is unique to have such strength.

German IP fell by 0.5% in February as manufacturing IP fell at the same pace. Both series continue to demonstrate acceleration profiles in output from 12-month to six-month to three-month. IP is up at a 6.8% annual rate over three months with manufacturing IP is up at a 7.5% pace. Germany is unique to have such strength.

Germany's output of capital goods and intermediate goods is accelerating sequentially too. After a period of weakness over six months, consumer goods output is advancing and accelerating again as well. Construction output also is sequentially accelerating with extremely strong rates of growth over three months and six months.

Quarter-to-date growth rates are balanced with annual growth rates of between 8% and 10% for IP and all its sectors. Construction IP is an exception as output there is exploding at a 17% annual rate in the quarter-to-date.

The fly in the ointment is that German real factory orders are not nearly so buoyant and show instead a decelerating pace with a decline over three months. Despite very strong output trends for Germany, order trends raise a question about where output might be headed in the future.

Two early-reporting EMU members, Ireland and Portugal, show mixed trends in February. Over three months Ireland shows rapid IP expansion with IP growing at a 9.7% annual rate and accelerating from 12-month to six-month to three-month. Portugal shows the opposite trends with output decelerating on that same timeline.

European trends have had considerable variation over the entire expansion period. While few countries are as of now reporting February output at all, trends generally point to expansions with only a few countries showing output contraction. Trends are generally reassuring. But forward-looking measures are less reassuring. And globally manufacturing PMI gauges are still weak.

Globally services remain weak

Today Markit released its global PMI readings for the services sector. The JP Morgan global services index gained to 51.4 in March from 50.9 in February but still has only a 14% queue standing since late-2008. This marks a one-month improvement that leaves the indices still very weak. Of 16-key countries and regions we monitor all but five show service sector expansion. The exceptions are France, Japan, Brazil, South Korea and Turkey. Month-to-month service sector output accelerated in nine of 16 of these places. Still, nine of 16 of these metrics have queue standings that are below their respective medians. Two countries have extremely weak reading below their respective 15th percentile: Brazil and Turkey. Only Indonesia and Canada have readings that lie at or above their respective 80th queue percentiles.

Services sectors have been the back-bone of ongoing expansion while global manufacturing has been weak. But nine of 16 of these places have March readings that are below their respective 12-month averages. The services sectors are having a hard time holding up amid all the manufacturing weakness. Of course, as the trends above show, Germany has been in a different world with solid manufacturing output having continued and with acceleration in train as the euro exchange rate has weakened. The IMF yesterday issued a warning about the fragility of the recovery. Meanwhile, exchange rates have continued to oscillate creating new competitiveness `winners and losers' in the search for stimulus. Monetary tricks continue to try to coax more growth out of the woodwork generally with slow or no success or worse. The IMF seems to realize that the global economy has reached a stage where the best policy options already have been laid upon the table. With so many fading or flat trends globally, that assessment is not very reassuring.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief