Global| May 06 2004

Global| May 06 2004German Industry Relying on Foreign Demand

Summary

Factory orders in Germany eased in March by 0.5%, but maintained their relatively high levels of the prior five months and extended a mostly rising trend into an 11th month. German data are classified according to the origin of the [...]

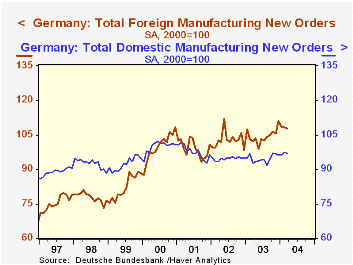

Factory orders in Germany eased in March by 0.5%, but maintained their relatively high levels of the prior five months and extended a mostly rising trend into an 11th month.

German data are classified according to the origin of the order, domestic or foreign. While both categories are up sharply from a year ago, it is evident in the graph that foreign orders have provided the firmer support to German manufacturing over the past 2-1/2 years. In fact, remarkably, capital goods orders from foreign customers did not experience a yearly decline during the recent recession. Scattered months showed 12-month decreases, but yearly totals rose without exception, albeit only a very little in 2001. Foreign orders for consumer goods were actually strong in 2001 and 2002, although they have trailed off somewhat since then.

The domestic German appetite for manufactured goods is more languid. Even after large increases last September and October, the level of domestic orders in March remains 3% lower than the 2000 base-year level. Consumer orders are the major weakness, as the first quarter this year averaged 86.0, off markedly from last year's average of 90.0. This sluggishness could well be related to a downtrend in employment. Both jobs and job vacancies have also been declining, suggesting that prospects are not particularly favorable for an early upturn in employment and a consequent rebound in domestic demand for manufactured consumer goods.

| SA, 2000=100 | Mar/Feb, SA %Chg | Mar/Mar NSA %Chg | Year/Year %Chg|||||

|---|---|---|---|---|---|---|---|

| Mar | Feb | 2003 | 2002 | 2001 | |||

| Total Orders* | 101.7 | 102.2 | -0.5 | 13.5 | 0.8 | -0.2 | -2.0 |

| Domestic | 97.0 | 97.3 | -0.3 | 12.8 | 0.0 | -3.2 | -2.6 |

| Foreign | 107.6 | 108.3 | -0.6 | 14.3 | 1.6 | 3.6 | -1.2 |

| Capital Goods | 104.3 | 103.6 | 0.7 | 15.3 | 1.2 | 0.1 | -0.9 |

| Domestic | 99.4 | 100.3 | -0.9 | 15.4 | 1.4 | -3.5 | -2.2 |

| Foreign | 108.8 | 106.7 | 2.0 | 15.2 | 1.1 | 3.3 | 0.3 |

| Consumer Goods | 91.4 | 93.1 | -1.8 | 10.5 | -3.5 | -2.6 | 1.2 |

| Domestic | 84.8 | 85.6 | -0.9 | 12.4 | -4.8 | -5.4 | -0.3 |

| Foreign | 106.3 | 110.1 | -3.5 | 11.4 | -0.9 | 3.5 | 4.6 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief