Global| Apr 24 2013

Global| Apr 24 2013German IFO reading drops

Summary

The IFO index, a survey of the German economy, fell sharply from a +6 reading in March to a reading of 1.5 in April. While a small positive number, the 1.5 reading stands in the 66.7 percentile or the top third of its historic range. [...]

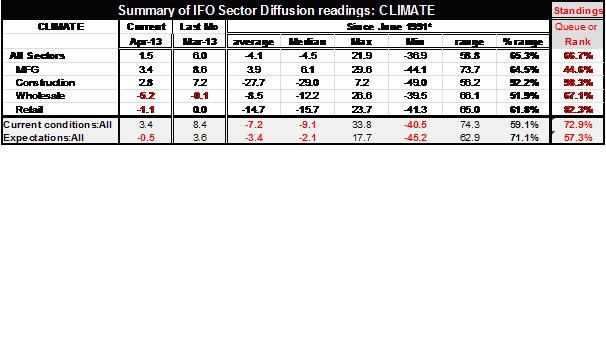

The IFO index, a survey of the German economy, fell sharply from a +6 reading in March to a reading of 1.5 in April. While a small positive number, the 1.5 reading stands in the 66.7 percentile or the top third of its historic range. Manufacturing that slipped from an 8.6 level in March to 3.4 in April is substantially weaker, standing in its 44th queue percentile; it is below its median as well it's as average. The construction sector continues to be strong despite the substantial slippage in April. The construction reading slipped from a +7.2 in March to a reading of +2.8 in April. At that the construction sector stands in the 98th percentile of its historic queue higher than this less than 2% of the time. Wholesaling slipped into the more substantial negative territory, dropping from a -0.1 reading in March to a reading of -5.2 in April. However, the average and median for wholesaling is an even weaker negative number for the wholesaling index that still stands in the top third of the range and is only stronger than its current value about one third of the time. Retailing crossed over from a zero reading in March to a -1.1 standing in April. At this level retailing is still in the top 18% of its range at the 82nd percentile. Like wholesaling retailing has a negative average and median.

The IFO index, a survey of the German economy, fell sharply from a +6 reading in March to a reading of 1.5 in April. While a small positive number, the 1.5 reading stands in the 66.7 percentile or the top third of its historic range. Manufacturing that slipped from an 8.6 level in March to 3.4 in April is substantially weaker, standing in its 44th queue percentile; it is below its median as well it's as average. The construction sector continues to be strong despite the substantial slippage in April. The construction reading slipped from a +7.2 in March to a reading of +2.8 in April. At that the construction sector stands in the 98th percentile of its historic queue higher than this less than 2% of the time. Wholesaling slipped into the more substantial negative territory, dropping from a -0.1 reading in March to a reading of -5.2 in April. However, the average and median for wholesaling is an even weaker negative number for the wholesaling index that still stands in the top third of the range and is only stronger than its current value about one third of the time. Retailing crossed over from a zero reading in March to a -1.1 standing in April. At this level retailing is still in the top 18% of its range at the 82nd percentile. Like wholesaling retailing has a negative average and median.

The overall index for current conditions fell from 8.4 in March to 3.4 in April. This leaves current conditions at the 73rd percentile of their historic range, meaning that the index is stronger about 27% of the time. Current conditions are still relatively firm in Germany despite the slippage this month. Expectations also slipped from a +3.6 in March to -0.5 in April. Overall expectations also tend to be negative a good deal of the time; this -0.5 reading leaves expectations still in the 57th percentile of their range above your average above their median stronger 43% of the time.

The chart shows that the IFO index, like the index from the European Community for Germany, demonstrates a very slight improving mode or is holding steady in this substandard state.

Germany's leading economic index for February from the Conference Board increased. So there is a positive data in the hopper for Germany. Still, today markets are reacting to the IFO survey which is a standard and bellwether for the German economy. The performance is not good as the Eurozone continues to underperform.

With Giorgio Napolitano serving another term in Italy there is yet another attempt being made to form a government based on the results of the last election which so far proved to be a complete and utter stalemate. This time, President Napolitano called Enrico Letta, deputy head of the center-left Democratic Party, to the Quirinale Palace, indicating he was likely to be asked to form a new coalition government: It's musical chairs Italian style.

Conditions in the rest of the zone and its environs are still uneven Dutch producer confidence slipped in April as did Czech business sentiment. Retail sales in Italy fell.

Today's reports leave us pretty much where we were before we had today's reports except without the hope that the IFO would provide some turnaround. Instead, the IFO is another weak reading, echoing the sentiment of the Markit sector surveys. We are confronted with another example of encroaching weakness in core countries of the eZone which continue to see their performance erode.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief