Global| May 28 2008

Global| May 28 2008German Export and Import Prices Show Mixed Trends: Pick Your Horizon

Summary

Near term pressures: The German CPI and PPI may have slammed on the brakes in April but export and import prices are still advancing- even ex-energy. The German PPI is generally unruly but the CPI has flattened out over three months [...]

Near term pressures: The German CPI and PPI may have slammed

on the brakes in April but export and import prices are still

advancing- even ex-energy. The German PPI is generally unruly but the

CPI has flattened out over three months with an annual rate of gain of

1.9% and an ex-energy reading of just 1.2%. German export prices in the

past three months are up at a 2.6% rate and imports at a 5.1% rate –

those numbers are not acceptable. While they are

not-seasonally-adjusted, German ex petroleum import prices are up at a

4.7% annual rate – over three-months -- and that is not much of an

improvement over the import headline pace. Moreover, the sequential

growth rates show acceleration in the ex-petrol import price trend,

12-Mo to 6-Mo to 3-Mo, just as for the PPI ex-energy. Even so,

ex-energy CPI prices are decelerating on this series of measures.

Some progress but not enough: Yr/Yr comparisons show a very different

story, at least for ex-energy prices. German CPI prices are up by 2.5%

overall and by 1.8% ex energy. For imports the total Yr/Yr gains is

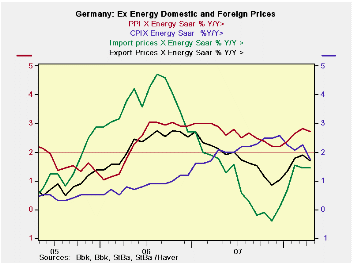

5.6% with an ex energy rise of just 1.5%. The chart above shows that

the key German prices Yr/Yr ex-energy all are below the 2% magic number

dictated by the ECB –that is except for the PPI. The ECB, however, does

not recognize any other target or ceiling for inflation except for the

HCIP headline rate and there the ceiling rate is 2% PERIOD.

Are the pressures peaking? Yr/Yr gains in the CPI ex-energy

peaked in December of 2007. Ex petrol import prices peaked in August of

2006. Even the Yr/Yr PPI ex petrol prices shows signs of peaking in the

last few months. Of course with oil prices having spurted again it is

too soon to tell how robust this phenomenon will prove to be. For the

time being year-over-year inflation trends, at least in Germany, seems

to reveal the symptoms of being contained. And the ECB, like the Fed in

the US, seems to prefer gauging inflation on its Yr/Yr performance

instead on a shorter annualized pace. Still, inflation is too high on

the all-important headline measures to let the ECB breathe freely.

Moreover, the ECB has other countries to worry about besides Germany.

Germany is making a solid contribution to an improved EMU rate of

inflation but problems in the zone continue to linger and perhaps to

fester.

| German International and Domestic Inflation Trends | |||||||

|---|---|---|---|---|---|---|---|

| % m/m | % Saar | ||||||

| SA; | Apr-08 | Mar-08 | Feb-08 | 3-Mo | 6-Mo | 12-Mo | Yr-Ago |

| Export Products | 0.1% | 0.1% | 0.5% | 2.6% | 3.2% | 2.2% | 1.9% |

| Import Products | 0.4% | 0.0% | 0.9% | 5.1% | 7.5% | 5.6% | 0.5% |

| NSA | |||||||

| Export excl Petroleum | 0.1% | 0.2% | 0.6% | 3.4% | 2.8% | 1.7% | 2.1% |

| Import excl Petroleum | 0.3% | 0.0% | 0.9% | 4.7% | 3.5% | 1.5% | 1.8% |

| Memo: SA | |||||||

| CPI | 0.0% | 0.4% | 0.1% | 1.9% | 2.7% | 2.5% | 2.1% |

| CPI excl Energy | 0.0% | 0.3% | 0.0% | 1.2% | 1.5% | 1.8% | 2.1% |

| PPI | 0.9% | 0.5% | 0.6% | 8.1% | 7.7% | 5.2% | 1.6% |

| PPI excl Energy | 0.2% | 0.4% | 0.4% | 4.0% | 3.1% | 2.7% | 2.9% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief