Global| Apr 25 2008

Global| Apr 25 2008German Export and Import Inflation Trends Blunted in March

Summary

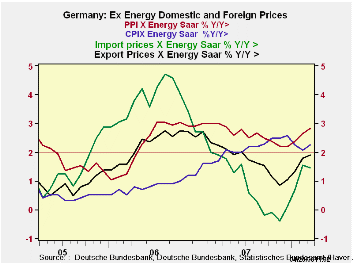

I don’t expect the ECB to declare inflation victory based on this German external price report. But, German ex energy prices are coalescing around the 2% level. That’s not headline inflation. And the result is for Germany not EMU and [...]

I don’t expect the ECB to declare inflation victory based on this German external price report. But, German ex energy prices are coalescing around the 2% level. That’s not headline inflation. And the result is for Germany not EMU and Germany consistently has one of the very best inflation records in EMU. So while the German figures show signs of inflation coming into line, we can expect figures for the Euro Area as a whole to fall short of this progress.

Even for Germany there remain question marks on inflation. Three month export and import headline price trends are, respectively at 4.5% and 6.7% over thee months, at 3% and 8.5% over 6-months and at 2.2% and 5.9% over 12-months. The twelve month results while better are still an acceleration over the previous March of 2007 12-month period (marked as Yr-ago in the table).

Since the ex-petroleum indices are NSA so the sequential growth rates calculations are not to be relied on. There, the 12-mnth growth in ex petrol export and import prices is at 1.9% and 1.5%, respectively: within ECB boundaries at least for an HICP headline rate.

But the actual German CPI headline rate is up by 3% yr/yr accelerating sharply from 1.9% over the previous March’s 12-month pace. Ex-energy the German CPI is up at a 2.3% pace, something the Fed in the US would be pleased with but it’s still accelerating from 1.7% in the 12-month period ending in March of 2007. While the ECB may look at ex-food and ex petrol HICP measures, its standard is for headline inflation alone and that is running ‘wild’ in the ECB’s mind. Still, the sequential growth rates for Germany’s overall and core CPI (which are based on seasonally adjusted data) are actually showing diminishing pressures.

The German PPI and its core remain rogue. The same inflation twist is at work in the US, but the US CPI report continues to perform well at least for Core inflation. Wholesale prices place a greater weight on raw goods. At a time of spiking commodity prices, that’s going to be a problem. Consumer goods industries use industrial prices as an input but have another stage of processing and therefore have another chance for productivity to keep price trends in check.

The German figures, while not up to the ECB’s lofty standards are nonetheless showing a lot of progress especially for a period with such repeated and strong commodity price shocks. One hopes that behind closed doors the ECB is really more pleased than what it reveals in its public comments.

Europe still has some inflation to fight. The situation in the UK seems to be worse than in the Euro Area. But the ECB seems to have matters more under control especially with the strong euro to help. The German price trends aren’t perfect but there are some good things in train there. As Euro Area economies are getting weaker maybe ECB rhetoric can tone down its concerns a notch or two – okay, maybe a half-notch or so….

| German International and Domestic Inflation Trends | |||||||

|---|---|---|---|---|---|---|---|

| % m/m | % Saar | ||||||

| SA: | Mar-08 | Feb-08 | Jan-08 | 3-Mo | 6-Mo | 12-Mo | Yr-Ago |

| Export Prices | 0.1% | 0.5% | 0.6% | 4.5% | 3.0% | 2.2% | 2.1% |

| Import Prices | 0.0% | 0.9% | 0.7% | 6.7% | 8.5% | 5.9% | 0.8% |

| NSA | |||||||

| Exports excl Petroleum | 0.2% | 0.6% | 0.7% | 5.8% | 2.6% | 1.9% | 2.2% |

| Imports excl Petroleum | 0.0% | 0.9% | 0.9% | 7.2% | 3.7% | 1.5% | 1.9% |

| Memo: SA | |||||||

| CPI | 0.4% | 0.1% | 0.2% | 2.7% | 3.5% | 3.0% | 1.9% |

| CPI excl Energy | 0.3% | 0.0% | 0.1% | 1.5% | 2.3% | 2.3% | 1.7% |

| PPI | 0.5% | 0.6% | 0.5% | 6.4% | 6.5% | 4.2% | 2.5% |

| PPI excl Energy | 0.4% | 0.4% | 0.4% | 4.7% | 3.1% | 2.8% | 3.0% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief