Global| Jul 29 2015

Global| Jul 29 2015German Consumer Sentiment Flat-Lines in August- and Nearly for Fifth Straight Month

Summary

The GfK consumer confidence climate measure was dead flat in August at a level of 10.1. It peaked at 10.2 in this cycle in June and registered 10.0 in April. It has been nearly flat since April with only minor variations. While the [...]

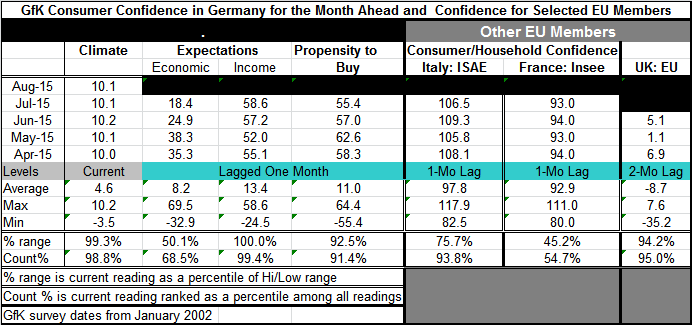

The GfK consumer confidence climate measure was dead flat in August at a level of 10.1. It peaked at 10.2 in this cycle in June and registered 10.0 in April. It has been nearly flat since April with only minor variations. While the German confidence measure may look as though it is stuck, it is stuck in a good place. At 10.1, the climate measure stands in the 98.8 percentile of its historic queue, pretty close to the top value ever. Income expectations stand in the 99.4 percentile of their historic queue; that is the top value. The propensity to buy stands in the 91.4 percentile of its historic queue, also a strong value. But holding the overall expectations back are economic expectations. These stand at 18.4 in July, down sharply from 24.9 in June. The July standing is in the 68th percentile of its historic queue, a moderate value and worlds apart from the standings of its fellow components. For GfK the expectations values lag by one month.

The GfK consumer confidence climate measure was dead flat in August at a level of 10.1. It peaked at 10.2 in this cycle in June and registered 10.0 in April. It has been nearly flat since April with only minor variations. While the German confidence measure may look as though it is stuck, it is stuck in a good place. At 10.1, the climate measure stands in the 98.8 percentile of its historic queue, pretty close to the top value ever. Income expectations stand in the 99.4 percentile of their historic queue; that is the top value. The propensity to buy stands in the 91.4 percentile of its historic queue, also a strong value. But holding the overall expectations back are economic expectations. These stand at 18.4 in July, down sharply from 24.9 in June. The July standing is in the 68th percentile of its historic queue, a moderate value and worlds apart from the standings of its fellow components. For GfK the expectations values lag by one month.

Fellow EU/EMU member confidence values lag Germany's GfK outlook survey by one month or more. Italy's report for July fell to 106.5 from 109.3, standing in the 93rd percentile of its historic queue, an extremely strong standing. France, however, has been struggling. Its confidence measure stands only in the 54th percentile of its historic queue of values, barely above its historic median (at the 50th percentile). The U.K., not a member of the single currency euro area, has a confidence reading that lags by two months. It, however, is strong standing in the 95th percentile of its historic queue of values.

The variations within the EMU are closing to some extent. A year ago, Italian confidence sat in its 57th percentile and French sentiment was in its 29th percentile while Germany and the U.K. were still extremely strong. Italy's consumer confidence has risen sharply to a very high standing over that period even though is economic performance continues to lag. Even France's standing has risen sharply, but it is still a substantial laggard. And those changes and standings go a long way toward explaining what has happened in the EMU.

And the situation with Greece drags on and on...

The future of the EMU still hangs in the balance. No one is quite sure what the Greek precedent will mean, but everyone is watching it closely. The rift with Greece now has more of its disagreements out in the open. While Europe has bent over backwards to give Greece a second chance, Greece does not seem to appreciate how far it has fallen off the wagon and wants to reserve some of the demands of its European creditors for later discussion. But there is nothing negotiable. This is just Greece trying to assert some sort of power over the proceedings where it has none.

What Greece does not seem to accept is that, yes, its sovereignty is being impinged upon and that is exactly what it wants if it is to stay an EMU member. Up to this point, Greece had been allowed a variance from EMU rules that other members were not allowed. Now Greece is being told that membership requires it to obey the rules that other members obey. Greece's case is not helped by the likes of Varoufakis, former finance minister, who talks of Greece as being a vassal state. It is not that. If it wants to remain in the euro-club, it must obey the euro-rules LIKE EVERYONE ELSE. But Greece wants to be different. It likes its own way of doing business. Unfortunately, that way does not lead to solvency, or to EMU membership. Greece must make a choice. So the Greek drama is back on stage; despite all the new proposals the legislature has passed, it is now known for the ones it refuses to move on. And that final decision will be a big factor for Greece and the EMU.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief