Global| Apr 11 2007

Global| Apr 11 2007French Trade Deficit Widens

Summary

Frances trade deficit widened in February as imports outpaced exports. Import growth continues to look more vibrant than export growth as the trends are accelerating more uniformly across trade categories. Over the recent three [...]

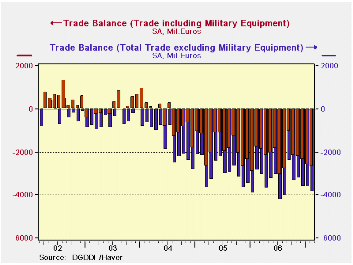

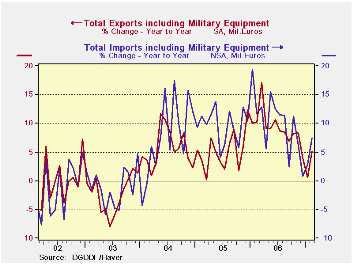

France’s trade deficit widened in February as imports outpaced exports. Import growth continues to look more vibrant than export growth as the trends are accelerating more uniformly across trade categories.

Over the recent three months imports are growing at a pace of 7.5% nearly the same as the Yr/Yr pace. For exports the overall pace for three month is barely positive and well under the Yr/Yr growth rate of 5%. For the rest of imports growth rates are quite solid. For capital goods the pace of acceleration is quite clear with blow-off type growth over the last three months. That pace is sure to cool from the near 40% it currently posts. Motor vehicle imports are strong, running at a super strong 28% pace and 14% Yr/Yr. Other consumer goods however show weakness: imports at -6.4% for three months and they are steadily decelerating.

This is the mixed picture for France. Export growth is cooling. Imports are strong and seem to point to strong domestic demand. But consumer goods imports (non-auto) are very weak and do not signal that same type of domestic demand strength form the consumer. For the moment France is a bit enigmatic.

After seeing export and import trends wither steadily throughout 2006 and early 2007 both exports and imports have sprung to life in February of 2007.

| M/M% | % SAAR | ||||

| Feb-07 | Jan-07 | 3M | 6M | 12M | |

| Balance* | -€€ 2,702.00 | -€€ 2,612.00 | -€€ 2,565.67 | -€€ 2,185.83 | -€€ 2,245.17 |

| Exports | |||||

| All Exports | 2.8% | -1.4% | 0.2% | 4.0% | 5.1% |

| Capital Goods | 1.3% | 1.3% | -1.1% | 18.9% | 1.8% |

| Motor Vehicles | 4.8% | 0.7% | 2.8% | -1.8% | 4.7% |

| Consumer Goods | 0.5% | -4.3% | -6.2% | 2.6% | 3.6% |

| IMPORTS | |||||

| All Imports | 3.2% | -1.2% | 7.5% | 2.6% | 7.6% |

| Capital goods | 6.4% | 2.6% | 39.1% | 10.8% | 9.0% |

| Motor Vehicles | 3.0% | 0.8% | 28.2% | 16.8% | 14.0% |

| Consumer goods | 2.0% | -1.9% | -6.4% | 0.5% | 6.2% |

| *Bil. Euros; mo or period average | |||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief