Global| Dec 10 2015

Global| Dec 10 2015French IP Makes Surprise Gain

Summary

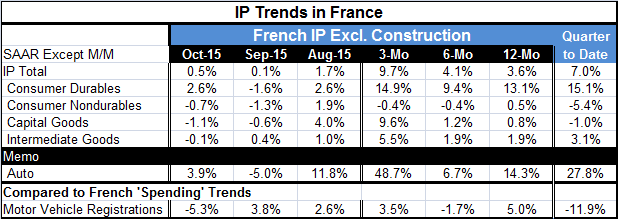

French industrial production rose by 0.5% in October. This marks three straight months of IP increases in France and gains in nine of the last 12 months. With the fourth quarter having just begun, IP is advancing at a 7% annual rate [...]

French industrial production rose by 0.5% in October. This marks three straight months of IP increases in France and gains in nine of the last 12 months. With the fourth quarter having just begun, IP is advancing at a 7% annual rate over its third quarter level.

French industrial production rose by 0.5% in October. This marks three straight months of IP increases in France and gains in nine of the last 12 months. With the fourth quarter having just begun, IP is advancing at a 7% annual rate over its third quarter level.

In October, the output gain was wholly on the back of consumer durable goods where output rose by 2.6% month-to-month. All other major categories of output, consumer nondurable goods, capital goods and intermediate goods showed output declines in October. In the quarter to date, consumer durable goods output is very strong, advancing at a 15.1% annual rate while nondurables output is shrinking at a 5.4% pace; capital goods output is falling at a 1% annual rate. The output of intermediate goods, however, is advancing in the new quarter.

The sequential growth rates from 12 months to six months to three months show acceleration for overall output as the pace rises steadily from 3.6% to 4.1% to a robust 9.7% over three months. Consumer durable goods trends are anchored by double digit growth over 12 months and three months with slightly slower growth over six months. Consumer nondurables show a deceleration to -0.4% from 0.5%. Capital goods output has an accelerating growth pattern with extremely strong growth over three months, at 9.6%. Intermediate goods also show a gain as the 1.9% growth rate for 12 months and six months rises to 5.5% over three months.

On balance, French IP shows a solid base of firm-to-strong growth rates. Only output for consumer nondurables is weak and that is likely due to the weakness in oil prices and in the energy sector at large.

French auto production has ramped up enormously, posting a 48% annual rate of change over three months. It posts a strong growth rate in two of the three recent months. Auto output has been underpinned by strong vehicle registrations. Registrations are up by 5% year-on-year and slow to 3.5% over three months. While registrations are up in two of the three most recent months, registrations fell off sharply in October, falling by 5.3%. This development and the weakness in nondurables are the sole indications of encroaching weakness for French industry.

In an unrelated report today, France posted a drop in its HICP of 0.1% in November, the same as for its domestic inflation reading. The domestic core index fell to flat from 0.2% in October. France saw consumer prices decelerate month-to-month in 6 of 11 categories with inflation rising monthly in only two. Weak and decelerating inflation generally is not a sign of an accelerating economy. However, with renewed weakness in global oil prices, we can expect many signs to be hard to read in the coming months.

For now, France is posting weak inflation numbers, but these are accompanied by firm industrial output trends. The recent weakness in motor vehicle registrations is something to keep an eye on. For the moment, France is in a bit of a sweet spot. The Bank of France projects only a slight negative impact from the recent Paris terrorist attacks.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief