Global| Oct 27 2017

Global| Oct 27 2017French Consumer Confidence Continues to Move South (Not the South of France)

Summary

French consumer confidence from INSEE continued to step back in October, falling to 100 from September's 101. Confidence had spiked at 108 in the midst of French election fever; however, June was a one-hit wonder as confidence jumped [...]

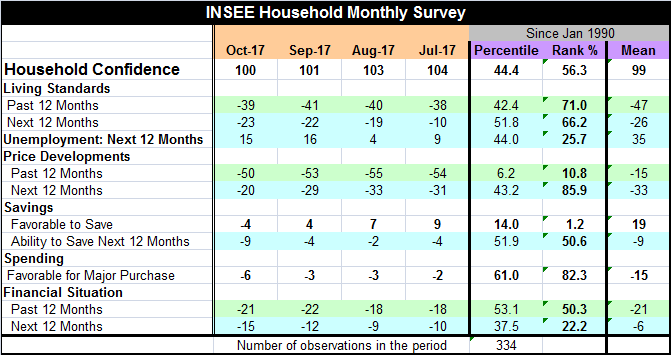

French consumer confidence from INSEE continued to step back in October, falling to 100 from September's 101. Confidence had spiked at 108 in the midst of French election fever; however, June was a one-hit wonder as confidence jumped to 108 from May's 102 then fell back to 104 in July and has edged lower month-by-month since then. Still, confidence averaged 97 for all of 2016 and ended the year at 99. The value 99 is the average for the confidence reading back to January 1990. So in October, confidence is a thin tick above average. The ranking for the monthly confidence standing is at its 56th percentile, implying that it is just a small margin above its median (which occurs at a rank percentile reading of 50). Confidence in France is only slightly above 'normal' according to comparisons with the mean and the median. While that is not a poor standing, it is a weaker one than might be expected given the relatively elevated Markit-survey private sector readings being posted by France. Its services sector and manufacturing sector each are being assessed as only having been better less than 10% of the time over the past six years. Yet, consumer confidence is only middling.

French consumer confidence from INSEE continued to step back in October, falling to 100 from September's 101. Confidence had spiked at 108 in the midst of French election fever; however, June was a one-hit wonder as confidence jumped to 108 from May's 102 then fell back to 104 in July and has edged lower month-by-month since then. Still, confidence averaged 97 for all of 2016 and ended the year at 99. The value 99 is the average for the confidence reading back to January 1990. So in October, confidence is a thin tick above average. The ranking for the monthly confidence standing is at its 56th percentile, implying that it is just a small margin above its median (which occurs at a rank percentile reading of 50). Confidence in France is only slightly above 'normal' according to comparisons with the mean and the median. While that is not a poor standing, it is a weaker one than might be expected given the relatively elevated Markit-survey private sector readings being posted by France. Its services sector and manufacturing sector each are being assessed as only having been better less than 10% of the time over the past six years. Yet, consumer confidence is only middling.

The French PMI scores from Markit have been strong by recent standards as the French economy has been recovering. Hollande may not have been very popular (beware: understatement), but he did turn over the economy to the new PM, Emmanuel Macron, in good shape.

In October, the French household rate for past living standards is at a -39, an improvement from September's -41. Their anticipation for the next 12 months, however, slips this month to -23 from -22 in September. Despite the difference in the actual values of the monthly diffusion indexes, the past living-standard rating is actually a higher ranking than is the outlook for the next 12 months. The past living standard ranks in its 71st percentile while the next 12-month outlook stands in its 66th percentile. Still, the ranks are reasonably well-elevated above their respective medians (at 50) and represent solid assessments for living standards.

The prospect for unemployment over the next 12 months is seeing a slippage to 15 from 16 and a percentile standing value of 25.7. A low ranking for unemployment expectations is a good sign. Unemployment 'fears' are lower than this month's value only about one-quarter of the time.

Price developments assessed over the past 12 months as well as over the next 12 months show less price weakness. The 12-month past diffusion score rises to -50 from -53 while the outlook score rises relatively sharply to -20 from -29. Price weakness in the past has been weaker only about 11% of the time. The outlook for prices finds prices having been expected to be stronger only about 14% of the time. While the raw diffusion scores are solidly negative, the outlook reading on inflation expectations is getting into relatively strong territory for the outlook.

French households note that the environment for saving slipped in October relative to September and the outlook is slipping as well. The past environment deteriorated by 8 points month-to-month; the outlook is now weaker by five points. The assessment of being favorable to save is at one of its lowest levels over the past 12 months at a 1.2 percentile ranking. However, the ability to save is now close to its mean value as firms look ahead and as the October reading has a 50.6 percentile standing, a slight margin above its historic median.

The current environment for spending grades out pretty well in October. Conditions slip on the month and form a reading of -6, a drop from a reading of -3. But the current reading still has a historic standing in its 82.3 percentile, marking it as better only about 18% of the time.

Households are concerned about their financial situation. Over the last 12 months, the assessment slipped by one point to a near neutral 50.3 percentile standing. Looking ahead over the next 12 months, the standing slips to -15 from -12 to a 22.2 percentile standing. That means expected financial conditions have been worse between one fifth to one quarter of the time.

There have been some very consistent and strong PMI readings for France that are not filtering through to the consumer. The two big current readings are in good shape; I refer to low fears of unemployment and a solid-to-strong assessment of spending conditions. Despite a long period of very contained inflation, inflation fears seem to be creeping. That is surprising since the ECB has been trying to boost inflation up to its target (near 2%) but has been unsuccessful. In a separate survey today for all of the EMU, it was reported that inflation expectations for the whole euro area rose by just one small tick in a survey conducted by the ECB. While living standards are on firm-footing, the future is somewhat in doubt as we see in the low ranking for expected financial conditions. Things are fine. Things have been fine. Fears of unemployment are low. It's a good time to spend (now)...but the future? That's the problem.

As the ECB gets ready to dismantle some of its growth support programs, we find the German economy operating at a strong pace with extremely low unemployment and very high confidence. But France, as the second largest EMU economy and having strong PMI readings, does not have the bravado to match Germany. French households are worried about the future. Some of the Macron labor market reforms, while good for the economy - especially one that has to compete in the same currency area with Germany, a next-door neighbor - are not popular and may give rise to some anxiety in households. Labor market reforms can be good for increasing a country's competitiveness since the conditions in competitor countries may be more favorable for producers there. But if being competitive policy changes cause some reduction in living standards, wages and job security, the public will not see those changes are for the better. It's a paradox of sorts. But it is true that businesses and countries must change to meet the competition. The economics of denial may keep an economy running under what seem to be constant conditions for a while, but eventually that will end if it is not competitive. And it might end in a bang. France is going through such a tension now as Macron has championed labor market reforms which are not popular but may very well be necessary for survival. Consumer confidence may be undergoing a tug-of-war over how it now views the future. And while the Macron reforms have not been popular, he did not make so many changes as to anger unions. France may yet have to take another step to move its labor rules into the 21st century, but it is done for now.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief