Global| Feb 25 2015

Global| Feb 25 2015French Confidence Takes the High Road (From a Low Start)

Summary

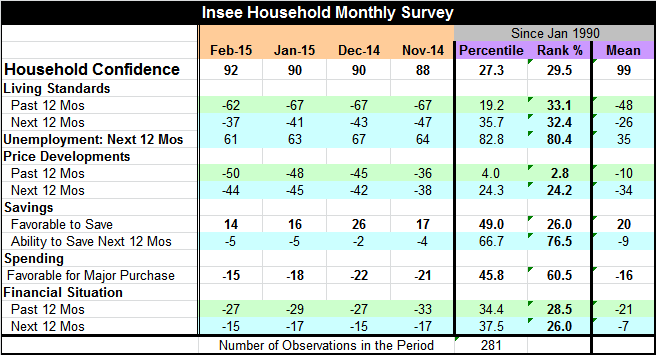

French household confidence moved higher to 92 in February from 90 in January, a nice two-point rise. At 92, French confidence was last at that level in May 2012 and last higher (for one brief reading) in November 2010. Confidence was [...]

French household confidence moved higher to 92 in February from 90 in January, a nice two-point rise. At 92, French confidence was last at that level in May 2012 and last higher (for one brief reading) in November 2010. Confidence was last persistently higher only in 2007 and earlier. So this spurt in confidence has taken France back closer to the pre-recession days of 2007. It's not there yet, but it is making a move in that direction.

French household confidence moved higher to 92 in February from 90 in January, a nice two-point rise. At 92, French confidence was last at that level in May 2012 and last higher (for one brief reading) in November 2010. Confidence was last persistently higher only in 2007 and earlier. So this spurt in confidence has taken France back closer to the pre-recession days of 2007. It's not there yet, but it is making a move in that direction.

At its current level, household confidence is still relatively weak as it stands only in the 29th percentile of its historic queue of values. And most of the report's metrics are sequestered in the lower reaches of their respective historic queues. France is not breaking out, but it is making some progress. We have seen the numbers for Germany improve as well. For France, in particular, the progress seems to be more in its services sector and that should translate into better conditions for French households. At a level of 98 French household confidence would be nearly back at its midpoint and that is only six points higher than the index stands now. It has already risen six points in the last four months. It is not as far from getting back to an even keel reading as its queue standing may make you think because the survey points are moving into a relatively dense portion of their respective distributions. The potential for improvement relative to past stands is becoming easier to attain.

Households in France report that living standards improved in the last 12 months but still stood only in the 33rd percentile of their historic queue of data. Similarly, the outlook for living standards over the next 12 months is four points better with a queue standing in its 32nd percentile. Expected unemployment is lower by two points but still stands at an elevated 80th percentile level in its historic queue. France is not yet out of the woods in terms of putting households' fears of unemployment behind them.

Price developments remain modest with assessments of prices over the last 12 months weaker only about 3% of the time historically, but over the next 12 months with the ECB becoming more activist price developments are expected to be higher with expectations in their 24th percentile, still low in a global environment where oil prices are putting the fear of deflation in force from the United States all the way to China.

French households saw the favorability of the environment for saving step back to a 26th percentile reading, but the ability to save has been steady at a 76th percentile standing. The environment for making a major purchase has been improving and it's up to the 60th percentile, one of the higher positive readings in this survey. The past and future financial situation is evaluated between its 25th and 30th percentile with both metrics on an improving trend.

France continues to struggle. But it appears also to be making progress. Falling oil prices are a double edged sword because they lower inflation and boost the flirtation with deflation but also put more funds into consumers' pockets and raise their real wage. On balance, as France is not an oil producer, there should be more consistent positive influences in play from oil prices. The European Central Bank is busy trying to stave off any deflation effects with several programs to boost the economy from the monetary side of things.

It is also helpful that the Greek situation seems to have passed without much incident. The Greeks had their moment of rebellion and then read the handwriting on the wall. They will not be protesting and rioting their way out of this one. They need to buckle down and get to business and that process seems to be underway. I think that will help to foster a more workman-like tone across the euro area as well. The burdens of adjustment may be heavy, but it's time to bend down and pick them up and to move forward. It is no use wishing for things the way they used to be. That's over. France seems to be making progress. Let it continue.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief