Global| Apr 10 2008

Global| Apr 10 2008French and Italian IP: Both Strong in 2008-Q1

Summary

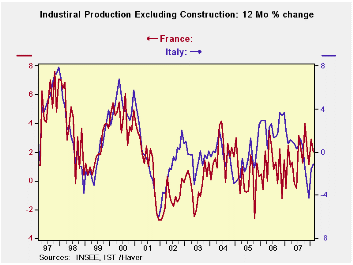

France and Italy often put their respective industrial sectors on a common trend. Although French IP has been expanding from mid 2006 to late 2007, Italy’s IP was declining and losing momentum in that period. However from late 2007 [...]

France and Italy often put their respective industrial sectors on a common trend. Although French IP has been expanding from mid 2006 to late 2007, Italy’s IP was declining and losing momentum in that period. However from late 2007 forward Italy and France appear to have industrial output on an upward path again. In the first quarter French IP is up at a 3% annual rate. In Italy the pace of expansion is a stronger 5.8%. Italian consumer goods output is stronger too at 7.4% compared to 2.2% for consumer goods in France. Both are seeing strong capital goods output again with Italy’s 18.5% leading but France’s 6.5% is still strong.

The sequential growth rates tell the story with France showing steady growth over 12 months, 6 months and 3 months. Italy, however, has been in a slump. Its 12-month and 6-month growth rates are negative with the six-month pace the weaker of the two. In the recent three months Italy has sprung back to life. Both Italy and France have posted growth in IP of about 6% over the recent three months. In this period, France’s growth is more balanced while Italy’s growth is from the capital goods sector.

With Europe undergoing various financial and exchange rate pressures it is not clear that France and Italy are really joined at the hip again as they once were. They’re in step over the past three months but beyond that growth is a question mark and so too must be the outlook for French and Italian IP. Germany’s IP echoes the strength we see in the French and Italian industrial sectors. But German orders have been flagging. Europe remains an enigma.

| French IP Excluding Construction | |||||||

|---|---|---|---|---|---|---|---|

| Saar exept m/m | Feb-08 | Jan-08 | Dec-07 | 3-mo | 6-mo | 12-mo | Qtr to-date |

| IP total | 0.3% | 0.6% | 0.7% | 6.3% | 1.1% | 2.0% | 3.0% |

| Consumer Goods | 0.2% | 1.5% | -0.7% | 4.0% | -4.7% | -1.0% | 2.2% |

| Capital Goods | 1.3% | 0.5% | 0.0% | 7.7% | 4.8% | 6.4% | 6.5% |

| Intermediate Goods | 0.2% | 1.4% | 0.1% | 7.1% | 1.4% | 1.0% | 4.8% |

| Memo | |||||||

| Auto | -1.9% | 2.1% | 3.4% | 15.3% | 3.9% | 0.3% | 8.7% |

| Italy IP Excluding Construction | |||||||

| Saar exept m/m | Feb-08 | Jan-08 | Dec-07 | 3-mo | 6-mo | 12-mo | -Qtr to-date |

| IP-MFG | -0.3% | 1.8% | 0.0% | 6.1% | -5.2% | -1.9% | 5.8% |

| Consumer Goods | -2.6% | 3.6% | -1.0% | 0.0% | -8.3% | -0.7% | 7.4% |

| Capital Goods | 0.0% | 6.3% | -2.4% | 15.6% | -0.8% | -0.7% | 18.5% |

| Intermediate Goods | -0.6% | 1.4% | 0.1% | 3.5% | -6.1% | -2.4% | 3.3% |

| Memo | |||||||

| Transportation | 1.5% | 2.9% | -3.0% | 4.9% | -5.7% | 1.2% | 0.0% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.