Global| Apr 17 2014

Global| Apr 17 2014European Car Sales Rise But Lose Momentum

Summary

Auto registrations in Europe have risen again on a year-over-year basis, posting an increase of 1.6% over 12 months. This, however, is down from a 6.8% year-over-year gain in February and is the smallest gain since October 2013. [...]

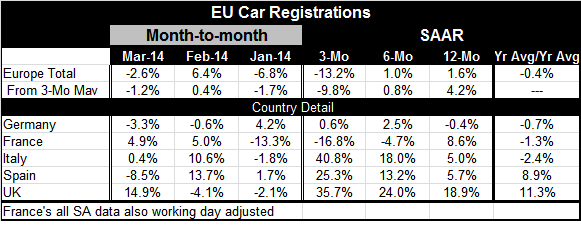

Auto registrations in Europe have risen again on a year-over-year basis, posting an increase of 1.6% over 12 months. This, however, is down from a 6.8% year-over-year gain in February and is the smallest gain since October 2013. Registrations were last weaker in September 2013 when registrations last declined. Smoothed percentage changes calculated from three-month moving averages show that year-over-year gains in overall registrations are 4.2% year-over-year. That's weaker than the 5.9% gain from February and the weakest since November 2013, with October 2013 being the last time that the year-over-year moving average was negative.

Auto registrations in Europe have risen again on a year-over-year basis, posting an increase of 1.6% over 12 months. This, however, is down from a 6.8% year-over-year gain in February and is the smallest gain since October 2013. Registrations were last weaker in September 2013 when registrations last declined. Smoothed percentage changes calculated from three-month moving averages show that year-over-year gains in overall registrations are 4.2% year-over-year. That's weaker than the 5.9% gain from February and the weakest since November 2013, with October 2013 being the last time that the year-over-year moving average was negative.

By country, in March there were two declines in Germany and Spain. For Germany, this is the second consecutive decline in registrations. For Spain, the 8.5% drop offsets only some of the 13.7% gain in February.

The three-month percentage changes for total European sales are at a 13.2% annual rate decline, with a 16.8% annual rate decline for France; Germany shows a small increase of 0.6% at an annual rate over three months. However, Italy Spain and the UK show huge growth rates over three months.

Sequential growth rates show there is explosive growth in registrations from 12-months to six-months to three-months in Italy, the UK and Spain. However, France shows the opposite pattern of sales becoming progressively weaker. Germany shows sales remaining listless over most of those periods, shrinking in two out of three of them. For Europe as a whole, the pattern is one of decelerating growth with growth going from an annual rate of 1.6% over 12 months to 1% over six months to -13.2% over three months. Europe's moving average echoes this trend.

While the headline, which focuses on the year-over-year growth rates, catches most of the attention, the trends should not be ignored. The trends show that there's a great deal of loss of momentum even though some of the countries, notably the Mediterranean countries of Italy and Spain, are showing some explosive growth. The UK continues to post what are eye-popping numbers; after two months of decelerating, UK year-over-year growth patterns are back to acceleration.

This month auto registrations data can't be taken as confirmation of European recovery. There continue to be somewhat erratic trends and it's for sure that the explosive growth in the Mediterranean countries will not be sustained. With auto sales there is always the additional problem of seasonal adjustment; although the data here are adjusted for most of the members in this table, seasonal adjustment of these big ticket items still leaves erratic movements. Car sales always are volatile. The real questions concern momentum and sustainability. Sustainability is a question to be answered in the future, while momentum already seems to be losing its grip on the overall trends for Europe as well as for Germany. The strength in Italy and Spain is interesting and notable but undoubtedly not sustainable. For overall sales, that question still hangs in the air.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief