Global| Oct 24 2008

Global| Oct 24 2008Europe's PMIs Are Weak- Showing Contraction!

Summary

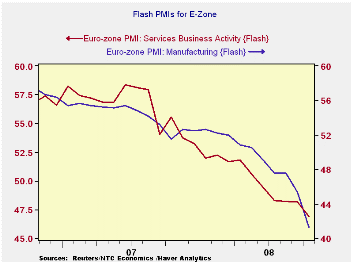

Europe’s PMIs are now weak. They are at or near the lows we have seen since the services PMI was issued in July of 1998. Both service sand MFG PMIs are below their respective neutral readings of 50 and are thus indicating CONTRACTION. [...]

Europe’s PMIs are now weak. They are at or near the lows we have seen since the services PMI was issued in July of 1998. Both service sand MFG PMIs are below their respective neutral readings of 50 and are thus indicating CONTRACTION.

The MFG PMI is even at its lowest level since June of 1997

when its survey began.

The month to month drop in the MFG index is the largest over this period while the services drop ranks as about the 18th smallest ‘gain’ in its history of the 63 drops in the 123 observation of the series. This months’ drop also ranks 45 in size among all drops or as the eighteenth largest drop when ranked among drops (or the bottom 28 percentile). In relative magnitude this month’s service sector drop is a bottom third affair. The MFG sector is taking the relatively larger hit for this month. It is taking its largest drop on record and falling to its lowest position in its history.

Europe has been a late comer to weakness but is catching up with the US. In September the US MFG PMI stood at a level 43.5, below where Europe was then but above where Europe is now. The US ISM may yet fall to a lower level in October and be weaker than Europe. But the two indices are clearly now sharing the same dimension of weakness regardless of which is the weaker. Last month the US non-MFG PMI stood at a level of 50 above the service sector reading for EMU. EMU’s drop to 46.91 seems clearly a weaker reading than what we get out of the US Non-MFG PMI (where 44.6 is the weakest reading ever) since sharp declines have not marked its recent trend. But things are changing fast and maybe the US non-MFG sector will weaken beyond Europe’s reading. We do not yet know how rapidly the economy descended in October. But this is not a time that has rewarded optimistic projecting. Maybe the message from Europe is that we should brace ourselves for even worse news from the US.

One message from Europe is nonetheless clear. Both MFG and

Services indices are quite weak and the MFG sector is falling very hard

right now. Expect the more conventional readings for Europe to start to

look a lot weaker. Since this report is topical and up-to-date as of

October it is a month or two ahead of the release of more conventional

economic reports form Europe.

| FLASH Readings | ||

|---|---|---|

| Market PMIs for the E-Zone-13 | ||

| MFG | Services | |

| Oct-08 | 41.33 | 46.91 |

| Sep-08 | 44.97 | 48.44 |

| Aug-08 | 47.55 | 48.46 |

| Jul-08 | 47.38 | 48.32 |

| Averages | ||

| 3-Mo | 46.63 | 47.76 |

| 6-Mo | 48.40 | 48.60 |

| 12-Mo | 50.37 | 50.52 |

| 33-Mo Range | ||

| High | 57.61 | 60.65 |

| Low | 41.33 | 46.68 |

| % Range | 0.0% | 1.6% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief