Global| Sep 15 2014

Global| Sep 15 2014Euro Area Trade Surplus Shrinks

Summary

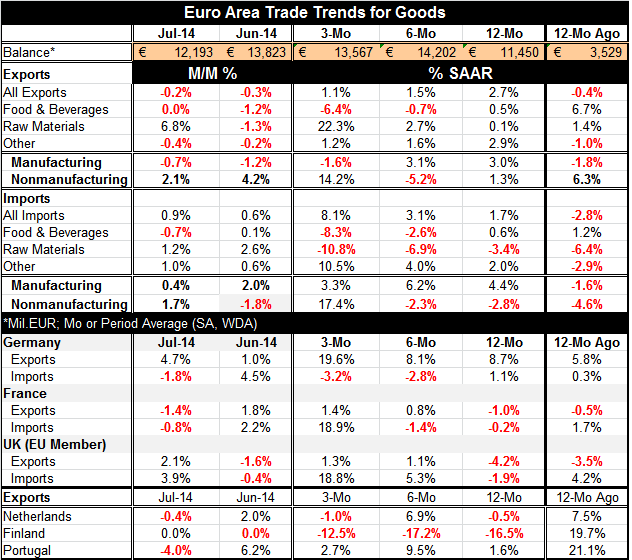

The euro area trade surplus shrank to 12.2 billion euros in July from 13.8 billion euros in June. The surplus is still higher than it was 12 months ago when it stood at 11.4 billion euros. Export growth fell by 0.2% in July as imports [...]

The euro area trade surplus shrank to 12.2 billion euros in July from 13.8 billion euros in June. The surplus is still higher than it was 12 months ago when it stood at 11.4 billion euros.

The euro area trade surplus shrank to 12.2 billion euros in July from 13.8 billion euros in June. The surplus is still higher than it was 12 months ago when it stood at 11.4 billion euros.

Export growth fell by 0.2% in July as imports rose by 0.9%. Manufacturing exports fell by 0.7%; manufacturing imports rose by 0.4%. Nonmanufacturing exports rose by 2.1% as nonmanufacturing imports rose by 1.7%.

The trends for manufacturing exports and imports show that manufacturing exports have weakened after having been relatively steady for the past year. The 12-month growth rate for manufacturing exports is 3%. Over six months the pace stays at 3.1%, but over three months it dips to -1.6%.

For manufacturing imports, the 12-month growth rate is 4.4%. That rises to 6.2% over six months and then tails back to 3.3% over three months.

Manufacturing imports are stronger and steadier than manufacturing exports that seem to be under some recent downward pressure in the last three months.

While the short-term trends in trade are somewhat mixed, the longer-term view shows that on year-over-year trends, exports have steadily been rising faster than imports. That export growth rate margin has narrowed recently. Also, both exports and imports are showing steady increasing growth from early 2013 onward. While the trade surplus is falling for two consecutive months, the surplus level is still relatively high.

Looking at the trends for some early reporters, we see that Germany's three-month imports are declining and imports are on a progressively expanding negative profile- not a good sign for German demand growth. France has opposite import trends with negative growth rates over 12 months and six months, giving way to a nearly 19% growth rate over three months. The U.K. shows progressively expanding imports, rising from -1.9% growth over 12 months to 19% growth over three months. The U.K. profile underpins the notion of improving U.K. economy. The German profile points to a slowing that has been in place in Germany in the wake of the Russian sanctions. France's upward reversal is only for three months and so it's too soon to count on.

On the export side, German exports are still robust despite its weak imports. Exports are up at a nearly 20% rate over three months after posting growth rates of 8% over six months and 12 months. This strength seems to underpin German growth while import weakness seems to undermine it!

French exports are clawing back to positive growth from -1% over 12 months to 0.8% over six months to 1.4% over three months.

The U.K. is rebounding with exports down by 4.2% over 12 months then bouncing back to gain 1.1% over six months and 1.3% over three months.

Finland shows chronically weak exports, dropping at a 16.5% pace over 12 months and a 12.5% pace over three months.

The Netherlands shows a tendency to contraction as exports fall 0.5% over 12 months, rebound over six months, then decline again at a 1% rate over three months.

Portugal shows some export progress as the growth rate of 1.6% over 12 months rises to a very strong 9.5% over six months and then moves back to 2.7% over three months.

Summing up

The overall European Monetary Union trend for exports shows some slight erosion in the growth rates from 12 months to three months. For manufacturing, the export erosion is sharper with growth rates of 3% falling at a 1.6% annual rate over three months. The member detail is somewhat mixed, but Germany tells the story of still strong exports that is not echoed in the rest of the member community.

EMU imports show growing strength, while manufacturing imports show sustaining growth, albeit with a slight moderating trend. The country detail shows German imports getting progressively weaker, while French imports reveal a nascent rebound.

The broad trend shows that export and import flows have moderated their uptrend in recent months. The detailed data show a good deal of irregularity within the EMU in both import and export trends. Strength of imports reassures us that growth in the EMU is still relatively firm and exports tend to echo that trend. Germany, a country that relies on export-led growth, continues to put up very good export numbers.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief