Global| Sep 10 2014

Global| Sep 10 2014Euro Area Members' IP Mostly Rebounds

Summary

Among the eight reporting countries of the European Monetary Union, five of these early reporters showed increases and three showed declines for industrial production in July. Output is lower by 0.3% in France, by 0.4% in Finland and [...]

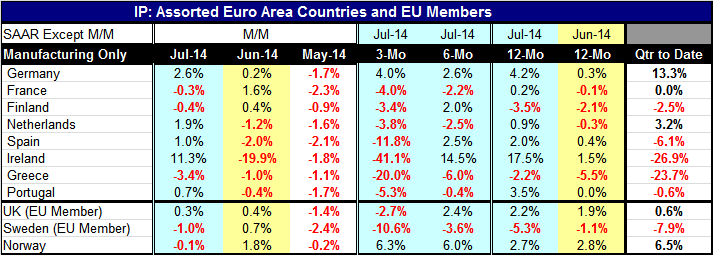

Among the eight reporting countries of the European Monetary Union, five of these early reporters showed increases and three showed declines for industrial production in July.

Among the eight reporting countries of the European Monetary Union, five of these early reporters showed increases and three showed declines for industrial production in July.

Output is lower by 0.3% in France, by 0.4% in Finland and by a large 3.4% in Greece. Output is increasing in Ireland, Germany, the Netherlands, Spain, and Portugal.

Despite strong results in July, the three-month growth results show declines in seven of the eight countries with Germany being the only exception.

German industrial production trends have held up well; the 12-month growth rate is at 4.2%, six-month growth slips to 2.6% and three-month growth is back to 4.0%. For the rest of the EMU member countries, 12-month growth rates are positive everywhere except in Finland and Greece. Most of them are showing declining trends in their growth rates for industrial production form 12-months to three-months.

July marks the start of a new quarter. We calculate the growth rates in this new quarter to date. These calculations are rather sensitive as they take the July level of output over the average for the previous quarter and compound the results over a two-month period. On this basis, output in Germany is flying up at a 13.3% annual rate. The Netherlands is up at a 3.2% annual rate. Output in France is flat. Everywhere else output is declining in the quarter to date.

We also have industrial production data for the U.K., Sweden and Norway. Among this group only the U.K. has an increase in July. Over three months only, Norway has an increase in industrial output while both the U.K. and Sweden are declining. Trends from 12-months to three-months show weakness in the U.K. and Sweden. Norway differs and shows industrial production growth acceleration on this horizon. In the quarter to date, the U.K. and Norway show gains while Sweden shows a substantial decline.

The euro area has been under a great deal of pressure and we can see that in the statistics for industrial production. Not surprisingly, Germany has held up better than the rest of the euro area as its economy is the most competitive economy in Europe. Even with the geopolitical issues that disrupted German trade relatively more than in other EMU nations, Germany's output has been resilient. However, its resiliency and strength stem a lot from its 2.6% gain in July, marking that trend as somewhat vulnerable as it depends substantially on one month's strength.

In other news today, we find that France is projecting that it will not reach its anticipated growth rate and that debt relative to GDP will be outside of the ratio previously agreed to with the European Commission. The news on weak growth in France is not too surprising. But the shortfall in the ratio to GDP is going to raise some questions, particularly about what the European Commission is going to do to deal with France's miss. Smaller countries have been put under a great deal of pressure to restore the debt to GDP ratio, a process that, in retrospect, appears to have been misguided. The question is whether France will be let off and how the rest of the Community will deal with any leniency toward France as one of the large EMU economies. Should France be spared the pain that Spain and Portugal and Greece and others have been made to bear? Has EMU learned from its past mistakes?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief