Global| May 20 2020

Global| May 20 2020Euro Area Inflation Remains Low...Heads Lower

Summary

Inflation in the euro area is low and has been persistently undershooting with very few exceptions since end-2012. Over that span of over seven years, HICP inflation has averaged 1% per year. Over that same period, the core rate has [...]

Inflation in the euro area is low and has been persistently undershooting with very few exceptions since end-2012. Over that span of over seven years, HICP inflation has averaged 1% per year. Over that same period, the core rate has averaged 1.1% per year. Inflation in the euro area has been persistently low and persistently undershooting its targeted pace of just under 2%. But during this period, the ECB had undertaken some extraordinary stimulus measures in the wake of the Great Recession and financial crisis and did not have a chance to unwind those policies when the coronavirus hit Europe. As a result, the ECB has adopted more policies of stimulus and these have elicited protests from Germany and others.

Inflation in the euro area is low and has been persistently undershooting with very few exceptions since end-2012. Over that span of over seven years, HICP inflation has averaged 1% per year. Over that same period, the core rate has averaged 1.1% per year. Inflation in the euro area has been persistently low and persistently undershooting its targeted pace of just under 2%. But during this period, the ECB had undertaken some extraordinary stimulus measures in the wake of the Great Recession and financial crisis and did not have a chance to unwind those policies when the coronavirus hit Europe. As a result, the ECB has adopted more policies of stimulus and these have elicited protests from Germany and others.

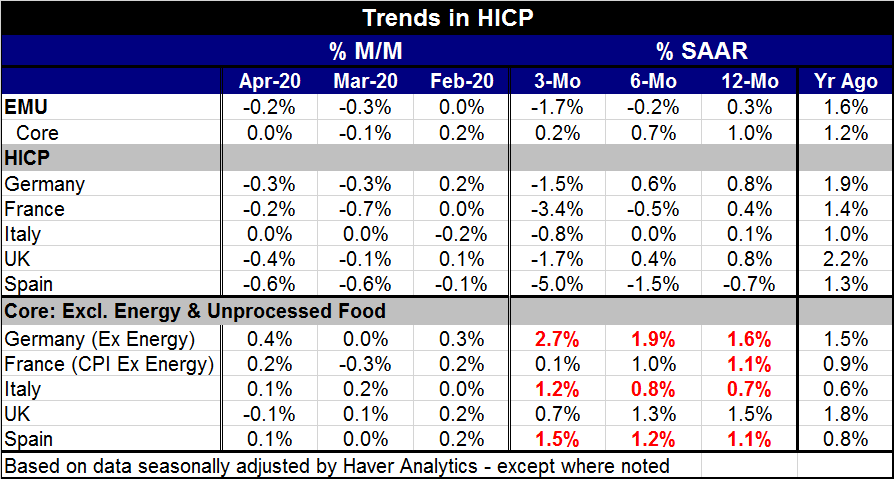

In April, the EMU inflation posted a -0.2% change month-to-month against a core rate that was flat. Sequentially from one-year to six-months to three-months, headline inflation has been falling starting with a 12-month pace of 0.3% and ending the sequence with a three-month annualized pace of -1.7%. The core on the same timeline also shows persistent deceleration, falling from a 12-month annualized pace of 1% to just 0.2% over a three-month pace.

All of this establishes inflation has been low, as being still low and looking like it will continue to be low.

Inflation is also low across the EMU as the four largest EMU economies Germany, France, Italy and Spain. Monthly data show headline inflation that is falling in each case except for Italy where inflation is flat month-to-month. Inflation also is decelerating in each of these countries as its pace dropped from its 12-month rate to its six-month rate to its three-month rate – without exception.

For inflation in each country over three months as well as over six months and 12 months, headline inflation is falling faster than core or ex-energy inflation. That development is true for each of these countries as well as in the EMU. Clearly, falling oil prices have had a large impact on inflation trends in the EMU, driving the headline pace lower followed by weaker core inflation.

However, the trends of core or ex-energy inflation show a more mixed nature than do the headline trends. German ex-energy inflation is clearly accelerating and up to a 2.7% annual rate over three months. Italian and Spanish core inflation rates also show persistent inflation acceleration, but for each of them it's on a more modest scale. Italy's three-month rate of inflation is still low at 1.2% and Spain's is moderate at 1.5%. France continues to show inflation deceleration for its core trend with three-month inflation at just 0.1%.

Falling oil prices have fed into weak inflation patterns. The chart shows Brent and WTI as well as some of the wildness in trending that WTI has seen in recent weeks. However, those days are over and oil prices are now beginning to firm. A combination of supply cuts and some firmness in demand albeit at a very weak level has helped to stop the bleeding in the oil market.

Falling oil prices have fed into weak inflation patterns. The chart shows Brent and WTI as well as some of the wildness in trending that WTI has seen in recent weeks. However, those days are over and oil prices are now beginning to firm. A combination of supply cuts and some firmness in demand albeit at a very weak level has helped to stop the bleeding in the oil market.

However, countries in the Northern Hemisphere are just starting to come out of their lockdowns. No one is quite sure how fast the return to something more like normal will be. But in most cases, countries are progressing slowly and for that reason inflation pressures either intrinsic pressures or pressures derived from oil and commodity prices should remain tempered.

I think it will be a long time before high inflation is a problem anywhere. As for all the government spending, stimulus and debt…all that debt is just going to have to be serviced and that is going to make growth weaker in the period ahead. I do not see the rise in debt as inflationary; it will help to depress growth ahead.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief