Global| Sep 28 2018

Global| Sep 28 2018Euro Area HICP Shows Mixed Trends/EU Shows Mixed Up Priorities

Summary

I suppose if you are German you look at this chart and see inflation ‘spiraling out of control’ as it tops the pace of 2% in a number of countries, a pace that inflation is supposed to stay below. However, a less dogmatic view on this [...]

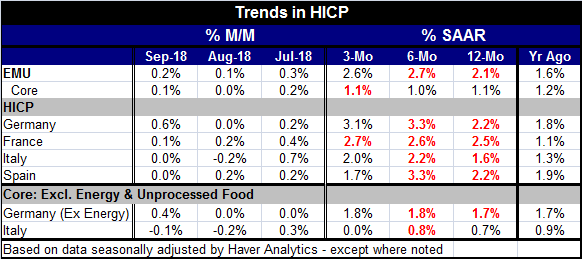

I suppose if you are German you look at this chart and see inflation ‘spiraling out of control’ as it tops the pace of 2% in a number of countries, a pace that inflation is supposed to stay below. However, a less dogmatic view on this chart shows inflation very near the 2% limit and flattening out. Beyond this chart, there is the additional possibility of watching the core inflation rate, where for the EMU, the pace is at a very moderate 1.1% and has been 1% or 1.1% over 12 months, three months and six months. Twelve months ago it was ‘higher’ at 1.2%. Core inflation has been very well-behaved and stable. While the Bundesbank never acknowledged a core inflation target or surrogate target as a fall back, the ECB under Mario Draghi has emphasized the core especially during a period when oil prices have been rising steadily driving headline inflation higher due to one-off forces.

I suppose if you are German you look at this chart and see inflation ‘spiraling out of control’ as it tops the pace of 2% in a number of countries, a pace that inflation is supposed to stay below. However, a less dogmatic view on this chart shows inflation very near the 2% limit and flattening out. Beyond this chart, there is the additional possibility of watching the core inflation rate, where for the EMU, the pace is at a very moderate 1.1% and has been 1% or 1.1% over 12 months, three months and six months. Twelve months ago it was ‘higher’ at 1.2%. Core inflation has been very well-behaved and stable. While the Bundesbank never acknowledged a core inflation target or surrogate target as a fall back, the ECB under Mario Draghi has emphasized the core especially during a period when oil prices have been rising steadily driving headline inflation higher due to one-off forces.

Core inflation...not rotten to the core

German ex-energy inflation continues to cruise below the 2% mark in the 1.7% to 1.8% range while Italy’s core rate has died in its sleep and is dead flat over three months while it is rising by only 0.7% over 12 months.

Pressures build...but

The inflation progressions show that German and French inflation is accelerating from 12-months to six-months to three-months. Both Italy and Spain show some headline acceleration from 12-months to six-months then deceleration from six-months to three-months. Spain’s three-month pace is below its 12-month pace. That is not the case for Italy, but its core is flat and tranquil especially over three months. The earlier ‘headline’ numeric citations were for inflation distorted by rising oil prices. How disturbing is that really? Should policy move for that?

Inflation risks boil...over?

If you are a staunch inflation targeter, I can see things in this report that might disturb you. Inflation is over its upper limit and it is accelerating over three months for a number of members but not for the EMU overall. The pace over three months for all of the EMU still is more than one half of one percentage point too-high. But such things are always looked at as background pressure indicators; central bankers focus on the more stable year-over-year trends. On that ground, the EMU overall inflation pace is just barely excessive while the German, French and Spanish inflation rates all are too high. Italy has plenty of breathing room still. Worry-warts can worry, but what’s the point?

ECB policy

The ECB is not going to change its focus or method overnight. Under Mario Draghi, the performance of the core has been elevated especially when the core and headline have a large gap and oil prices have fed that gap - and that is still the case. But some in the EMU are looking to make the case to end the special stimulus and the ECB itself has adopted a plan to begin its exit. Still, the data and trends raise all kinds of questions on both sides.

Synchronicities...

One interesting question is how the Italian inflation undershoot and how Italy’s dramatic under performance of growth relates to Italy’s budget restrictions. The EU Commission, after being very lax about budget rules, really came down hard in this cycle and subjected a number of EU members to austerity rules to get their budgets back in shape. While this procedure has reduced inflation around the euro area and has made all members either inflation complaint for the past few years or every close to it, an ancillary fact is that this has been done at the cost of growth, and in some places, like Greece and Italy, the cost has been extremely high. Chemotherapy in medicine is very uncomfortable and patients suffer under its application. It is not supposed to kill the patient, but some do not survive the procedure. A procedure that the patient does not survive is not a good one. And in the case of Italy, while the country has survived, its real GDP has been for a decade below its pre-crisis peak. And that is a very high price to pay to reduce the inflation rate. It is fair to ask if that was a ‘cure’ or a new disease?

The Italians jobbed...

Italy now seeks a budget that is more expansive than Maastricht rules allow. The EU Commission does not seem to be of any mind to let Italy off the hook- rules are rules. And this has become a big problem and it now is a point of conflict. I have always thought we should refer to this currency-zone arrangement as the ‘euro-Area’ instead of the ‘Euro-Area.’ The lower case ‘e’ reminds us that this arrangement is not about Europe, the continent, but is about ‘euro’ the currency. Of course, not all EU members are in the EMU but with a few agreed exceptions the rest are supposed to be matriculating toward the goal of EMU membership. Is no sacrifice too great to keep the Euro-Area intact?

The cost of membership

There is nothing ever specified about what the cost of this membership might be. Italy labored under the yoke of austerity and now with a new government it seeks to use fiscal policy to restart its growth and the EU Commission opposes it. Is that blanket opposition wise? Since there is no fiscal redistribution in the EMU, there is just a monetary union. There is no limit to the amount of pain a single member might have to endure without any assistance to meet the ongoing requirements of EMU membership. Moreover, what is there to say about an EU Commission that enforces rules with laxity then suddenly comes down hard with letter-of-the-law enforcement?

Dysfunctional Europe- no wonder these people kept going to war

Currently, the decision of membership is made harder on members by the choice of Germany to take this opportunity to run a contractionary fiscal policy complete with a budget surplus. Some stimulus from Europe’s most financially sound economy could help alieve suffering elsewhere, but none is forthcoming. Germany could even pay more to help the joint NATO defense effort but it does not because it has prioritized a fiscal surplus over defense. To put all that in a bit more of an odd position, the EU is taking a very hard line against the U.K. that is exiting the EU arrangement even though the U.K. is the most militarily accomplished country in the region and the EU military position is very weak with the U.K. out. I have no idea what Europeans are using to set priorities these days instead of brains.

Migrant issues

The EU’s treatment of border countries, especially Italy and Greece who have absorbed the brunt of the migrant influx, has been deplorable. Greece was forced to use its own austere budget resources to support migrants without help as it struggled with austerity. Italy is now so fed up with EU treatment that it has closed its ports to rescue ships and refused to be the port of first entry which damns a country to all sort of obligations under the EU rules. Of course, the centrally-located EU countries that have no water borders or only extreme northern access are essentially immune to this sort of migration.

Burden-sharing? No

I see Europe as an area with huge problems because its members are not willing to share the burden of their policy on anything like an equal basis. And when a country like Italy or Greece goes under the yoke of austerity and that creates obvious economic pain and suffering, there is no relief from the rest of the community. And because of budget austerity, these countries are not able to provide help for their own population using fiscal means.

Inflation transgressors brought to heel...but at a cost

Inflation transgressors brought to heel...but at a cost

Got Flexibility?

We can look back at the progress of inflation in formerly high inflation countries and can call that success... But at what cost? Cost is always an issue. The cost to Italy and to Greece of their austerity has been very high. The rest of the Community acts as if it has no obligation to do anything other than to engage in a strict enforcement of rules. Yet, countries were given a pass in the past for budget violations including France and Germany. Couldn’t the EU find a way to work with Italy to provide some structured variance for it rather than to maintain its hard line and whip up the obvious festering wrath of the Five Star Movement and the Northern League in Italy? What kind of ‘Community’ is this supposed to be? Where is its sense of ‘community?’ And who is setting its priorities when there are clashes? So far, there appears to be very little at work other than a slavish dedication to enforcement of existing rules. And for a community that offers no fiscal or cross border assistance, that approach can dish out very harsh medicine.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief