Global| Oct 30 2008

Global| Oct 30 2008EU Indices Are Scraping Low Levels: It Will Get Worse…

Summary

The news this month for the EU/EMU region is bad. The EU reading is in the bottom 10% of its range of value. The EMU reading is a bit better, in the bottom 17% of its range. Both are quite weak. The drop in the index is the largest [...]

The news this month for the EU/EMU region is bad. The EU reading is in the bottom 10% of its range of value. The EMU reading is a bit better, in the bottom 17% of its range. Both are quite weak. The drop in the index is the largest since the data have been collected in 1991. All sectors made larger falls in Oct compared to Sept. The main EMU countries also saw large drops in their respective overall sentiment indices.

By sector, services is relatively the hardest hit standing at

the lowest point of its range since that survey began. But that only

goes back to October of 1996 instead of 1991 as for the other surveys.

Still this result parallels the sort of readings we have been getting

in the US with a very weak service sector checking in.

Is this more than coincidence? You bet! This crisis is

hitting intrinsically domestic sectors harder like real estate and

finance. Typically banks populate every community; the same with real

estate businesses. These sectors are not like mining or autos or

textiles that may have a particular regional representation. The

troubled sectors in this cycle are spread everywhere and the troubled

asset class ‘housing’ is everywhere, as well. It’s as true in Europe as

in the US.INDUSTRY

Europe’s industry reading at -18 (EMU) is only in the 32nd percentile of its range (bottom third of its range) and so is weak but not desperately weak. Germany and France carry percentile positions for their respective readings in the high thirty percentiles while Spain’s is at the 33rd percentile and the UK is at the 27Th percentile; Italy is looking desperate at the 17Th percentile. These are weak readings but the most troubling for Italy.

The components of the industry index show that the production trend is the weakest relative reading standing in the bottom 3% of its historic range. Production expectations are better but still weak in their 12th percentile. For some reason Europeans think that a worse time lies behind it not ahead of it. That explains a lot about the government attitudes. Europe has been in and seem to remain in DENIAL. Order volumes are still relatively firm in their 44th range percentile; export orders are in about the same relative range position and that is also where the expected selling price resides. Contrarily workers are more exposed with employment expectations in the bottom 16 percentile of their range. If worker readings are RIGHT then the rest of the readings are too high.CONFIDENCE

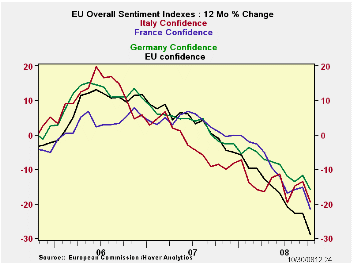

By main countries confidence readings are all over the map except that they are limited being to all over intrinsically weak territory. The EU’s UK reading is in the bottom 2.9% of its all-time range. Among large EMU nations Spain is weakest posting the lowest confidence reading ever. It is followed by France with a bottom 5 percentile reading. Germany’s percentile reading at the 43% mark and is similar to its industrial sector reading but at 37.5 Italy’s percentile reading is way above its industry percentile. So, Italian consumer confidence is more upbeat than it is for Italian industry.

As for the reason for this angst, ee find over all EMU responses on ‘time to buy’ are at the very worst for making major purchases now or in the next 12 months. The economic situation in the past 12-months is rated as the worst ever but looking ahead for the next 12-months the out look is ‘only’ a bottom 13% ordeal. Respondents may want to rethink that one. The financial situation for this past and this next 12-months each rate in their respective 12th percentile. In short the readings really are weak. Unemployment expectations are ‘only up to the 58th percentile of their range – elevated, but not by much.RETAIL

The retail readings across EU countries are weakest in the UK, residing in their bottom 3 range percentile followed by Spain (bottom 13%), Germany (bottom 26%), France (bottom 43%), and Italy (63rd percentile – still above its range midpoint). Retailers are not as downbeat as consumers and that could spell some troubles for them and for their inventories. Retail orders are put in the bottom 14% of their range. The expected business situation is only a bottom 38% rating similar to the present business situation. And maybe the retailers are just putting up a brave front since their orders are so weak. They may be planning for something even weaker than what they say they expect… SERVICES

Service sector reading span the gamut form bad to worst. The UK and Italy have the worst service sector readings ever. Spain’s reading is in the bottom 6% of its range. German is a bottom 25% reading; for France the reading is a bottom one-third of range reading. All of theses are weak. For EMU the overall reading is the worst ever. The business climate is a bottom 7% affair, but expected demand is worse in the bottom 2% of its range. Current demand is rated as in only the 16th percentile. Current and expected employment readings are in the 20th percentile of their respective ranges, and the reading is lower for expected unemployment. Things will get worse. Maybe industry workers are better protected by unions that service sector workers.CONSTRUCTION

The construction sector is the least impacted off all. For overall sentiment, construction stands in the 49th percentile of its range. Of course that implies a raw reading of -20. One issue for construction it that its participants have considered it sub-par all along. So now the outlook is being impacted construction respondents are not looking for things to get that much worse. Spain is an exception having had a boom its current reading; it is a bottom 19th percentile reading. For the UK the residential property bubble busting has helped to drag its reading to the 31st percentile. France and Germany still carry mid range readings at or above their expected range midpoints. Italy’s sector has a relatively strong construction reading in the 60th percentile.

| EU Sectors and Country level Overall Sentiment | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| EU | Oct 08 |

Sep 08 |

Aug 08 |

Jul 08 |

%tile | Rank | Max | Min | Range | Mean | R-SQ w/Overall |

| Overall | 77.5 | 84.9 | 86.7 | 88.8 | 9.8 | 209 | 116 | 73 | 43 | 99 | 1.00 |

| Industrial | -19 | -13 | -10 | -7 | 23.5 | 204 | 7 | -27 | 34 | -7 | 0.86 |

| Consumer Confidence | -23 | -19 | -19 | -20 | 13.8 | 205 | 2 | -27 | 29 | -11 | 0.83 |

| Retail | -16 | -13 | -14 | -11 | 18.5 | 214 | 6 | -21 | 27 | -6 | 0.51 |

| Construction | -25 | -20 | -18 | -17 | 37.8 | 150 | 3 | -42 | 45 | -17 | 0.41 |

| Services | -10 | -4 | -2 | 0 | 0.0 | 145 | 32 | -10 | 42 | 16 | 0.81 |

| % m/m |

Oct 08 |

Based on Level | Level | ||||||||

| EMU | -8.1% | -1.1% | -1.1% | 80.4 | 16.8 | 206 | 117 | 73 | 44 | 99 | 0.94 |

| Germany | -5.1% | -1.4% | -2.7% | 88.6 | 23.5 | 186 | 121 | 79 | 42 | 99 | 0.61 |

| France | -7.0% | -0.6% | -0.1% | 86.5 | 31.6 | 196 | 119 | 72 | 47 | 100 | 0.79 |

| Italy | -6.9% | 0.6% | 2.7% | 82.1 | 21.6 | 206 | 121 | 71 | 50 | 99 | 0.78 |

| Spain | -5.0% | -2.0% | -4.3% | 66.1 | 0.0 | 220 | 118 | 66 | 52 | 99 | 0.62 |

| Memo: UK | -7.5% | -5.2% | -6.1% | 70.4 | 3.4 | 219 | 118 | 69 | 50 | 100 | 0.42 |

| Since 1990 except Services (Oct 1996) 247-Count; Services: 145-Count | |||||||||||

| Sentiment is an index, sector readings are net balance diffusion measures. | |||||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief