Global| Apr 30 2015

Global| Apr 30 2015EU/EMU Unemployment Rates Unchanged in March

Summary

Unemployment rates in Europe were largely unchanged in March. The EU and EMU regions both showed no change in their region-wide unemployment gauges. Under the surface, huge differences among national rates of unemployment, of course, [...]

Unemployment rates in Europe were largely unchanged in March. The EU and EMU regions both showed no change in their region-wide unemployment gauges. Under the surface, huge differences among national rates of unemployment, of course, remain.

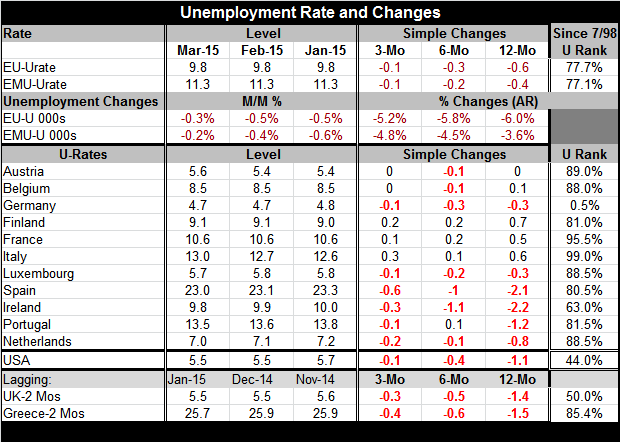

Unemployment rates in Europe were largely unchanged in March. The EU and EMU regions both showed no change in their region-wide unemployment gauges. Under the surface, huge differences among national rates of unemployment, of course, remain.

A calculation of diffusion among the various unemployment rates in the EMU shows that national differences are still at extreme divergence. Diffusion (or differences among national rates of unemployment) in the euro area is in the top 25% of what it has been since 2004. Put another way the unemployment differences are 78% above their average divergence for this period.

The chart shows the unemployment rate rates for several countries and for the EU region as a whole. It is obvious that some huge differences persist. And remembering that there is only one central bank for the EMU region, this variation gives you a clear perspective on the difficulties of running one monetary policy for the whole region.

The table shows some clear differences in trends. Roughly the top six countries in the table and the bottom five seem to be experiencing very different trends. Among the top six, only Germany is still seeing ongoing declines in its unemployment rate over three months as well as over other horizons. But German unemployment is unchanged in the last two months and its trend of dropping rates of unemployment also is fading. Italy, France and Finland, also in the top six, show unemployment rates edging higher over three months, six months and 12 months. Austria and Belgium have no clear trends and have unemployment unchanged over the last three months.

In the bottom of the table, Luxembourg, Spain, Ireland, Portugal and the Netherlands each shows still declining rates of unemployment. All but Portugal shows declines over all the horizons in the table. Spain and Ireland show declines may still be on trend as well as Luxembourg and the Netherlands where the drops are much slower. Portugal shows that its declines are slowing.

Many challenges remain for the ECB. In today's inflation report, year-over year inflation stopped declining. Monthly inflation is up for three months running. Headline inflation is rising at a 2.6% annual rate over three months as oil prices continue to show some upward movement. But core inflation in the euro area is only very mildly accelerating with a three-month pace of 1.2% compared to year-over-year pace of 1.0%.

As oil gives prices less downward momentum, the inflation picture will normalize. But it is not clear that will in any way help nations to lower their unemployment rates. However, if inflation begins to matriculate back toward its long terms goal of 2% in the euro area, we could find members with less tolerance for stimulative policies like the QE program that the ECB has only recently launched.

Still, it is far too soon to start worrying about inflation rising. There is still quite a legacy of inflation undershooting. And globally growth is still hampered. Recent reports in the U.S. have soured as GDP barely rose in the first quarter and with job growth looking as though it too might be slowing. If the U.S. growth rate steps down, there will be no dependable source of growth in the world economy. Europe is struggling, Japan is too, and China, while still posting an official rate of 7% in 2015-Q1, is well below its recent growth rates. The Chinese government is implementing special programs to try to keep higher growth rates on the books.

It is good to see that some needy EMU members are still able to reduce their unemployment rates while the overall EMU rate is unchanged. But the trends for growth in the EMU are still not very solid and prospects for this sort of progress to last are not very certain either. The recent backtracking in Italian and French unemployment rates is particularly disturbing. Europe continues to be a one-trick pony relying solely on stimulative monetary policy to give it a boost. So far it has worked, but progress now seems to be slowing. And the dropping euro that has breathed life into so many EMU economies has hit a sticking point. As unemployment drops are harder to get, as the euro slippage abates and as inflation starts to rise, is Europe at a crossroads?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief