Global| Jun 27 2008

Global| Jun 27 2008EU and Country Sentiment Indices Falling Except for Italy

Summary

Setting the tone: The EU sentiment indices set the tone for the month’s upcoming reports. Overall EU sentiment, with its sharp drop over the past three months now resides below the mid point of its range in the 49.8th percentile and [...]

Setting the tone: The EU sentiment indices set the tone for the month’s upcoming reports. Overall EU sentiment, with its sharp drop over the past three months now resides below the mid point of its range in the 49.8th percentile and is about 5.5% below is average. Despite a raw negative reading, the industrial index is above its midpoint at the 67th range percentile; it edged one point lower in the month. Consumer confidence at -17 also fell in the month and is in its 34th range percentile. Retail’s reading fell but remains above the April low. It stands in the 59th percentile of its range and is right at is period average. The raw construction sector reading slipped in the month. It stands in the 62nd percentile of its range. The service sector carries a positive reading and did notch up this month but still stands in weak stead, in the 34th percentile of its range.

Countries are having differing experiences: Overall country ratings find Germany’s sentiment is the 67th percentile of its range, a still firm reading (top third). France’s sentiment stands in the 57th percentile of its range. For EMU as a whole the range standing is just below its mid-point at 49.7. Italy is in its 47th range percentile. Spain is very weak at its 12th overall range percentile. Spain tends to be least correlated with the EU index among these countries. Italy, despite its relative weakness is showing some rebound as its Yr/Yr sentiment gauge is dropping with noticeable deceleration.

Trends differ too: One balance these are weak readings for Europe. They are not recessionary as the main drivers for growth are showing relatively firm results. But the UK, an EU member has slipped below the mid point of its overall sentiment range. Italy has been there, too, but actually has slowed is rate of descent. Spain is very weak with the Zone’s worst property market and, therefore, the most to lose from an ECB rate hike. Meanwhile Germany and France are supporting the EU readings. But in France consumer confidence has been falling and Germany has been undergoing erosion in confidence and in MFG measures.

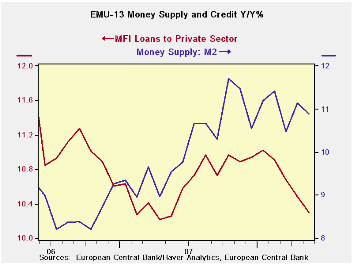

All the usual Bug-a-boos still haunt growth prospects: The usual culprits are still beating on these economies. High energy prices threaten, rate hikes from the ECB are awaited, too-high inflation lingers, financial turmoil persists, real estate problems dog some members more than others, and under capitalized banks are like a constant foot on the brake pedal… These are serious issues. And they have undermined consumer confidence across the board. To some extent Europe’s export prowess has helped keep it aloft but that is being pressured as global growth slows and the euro has ticked back up. Now there is the new step up in oil prices to contend with. Europe is under pressure and with downward revisions to growth in several countries (made on Friday June 27th) the future for growth in EMU remains challenged. The Governor of the BOE, Mervyn King, has been the most outspoken in saying that growth will have to slow to rein in inflation. But how far is the BOE and how far is the ECB willing to go? These key lingering questions are the keys points in the current outlook and real uncertainties especially as inflation averse Germany notches an even higher preliminary CPI rate at 3.3% in June.

| EU Sectors and Country level Overall Sentiment | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| EU | Jun 08 |

May 08 |

Apr 08 |

Mar 08 |

%tile | Rank | Max | Min | Range | Mean | R-SQ w/ Overall |

| Overall | 94.6 | 97.1 | 98 | 101.9 | 49.8 | 156 | 116 | 73 | 43 | 100 | 1.00 |

| Industrial | -4 | -3 | -2 | 0 | 67.6 | 86 | 7 | -27 | 34 | -7 | 0.87 |

| Consumer Confidence | -17 | -14 | -12 | -11 | 34.5 | 192 | 2 | -27 | 29 | -10 | 0.83 |

| Retail Sales | -5 | -3 | -6 | 1 | 59.3 | 98 | 6 | -21 | 27 | -5 | 0.48 |

| Construction | -14 | -11 | -11 | -9 | 62.2 | 105 | 3 | -42 | 45 | -17 | 0.42 |

| Services | 7 | 6 | 6 | 11 | 34.2 | 101 | 32 | -6 | 38 | 16 | 0.81 |

| % m/m | Jun 08 |

Based on Level | Level | ||||||||

| EMU | -2.8% | 0.5% | -2.5% | 94.9 | 49.7 | 149 | 117 | 73 | 44 | 99 | 0.96 |

| Germany | -1.5% | 0.2% | -1.2% | 101.5 | 67.9 | 101 | 112 | 79 | 34 | 99 | 0.75 |

| France | -2.7% | -1.8% | -2.4% | 98.5 | 57.3 | 129 | 119 | 72 | 47 | 100 | 0.79 |

| Italy | -0.1% | 3.3% | -1.7% | 95.0 | 47.4 | 146 | 121 | 71 | 50 | 100 | 0.79 |

| Spain | -7.8% | -0.4% | -4.1% | 73.0 | 12.3 | 200 | 118 | 67 | 51 | 100 | 0.61 |

| Memo: UK | 2.3% | -5.4% | -8.5% | 92.7 | 44.6 | 172 | 118 | 72 | 46 | 101 | 0.45 |

| Since 1990 except Services (Oct 1996) | 222 | -Count | Services: | 126 | -Count | ||||||

| Sentiment is an index, sector readings are net balance diffusion measures | |||||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief