Global| Aug 20 2004

Global| Aug 20 2004Energy Prices Rise as World Demand Increases, But US Energy Efficiency Alleviates Some Impact

Summary

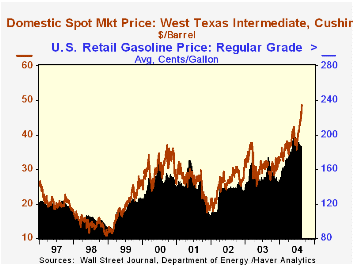

A piece of what is now "ancient" history: on December 10, 1998, the price of a barrel of West Texas Intermediate Crude oil was $10.73. Yesterday, it was $48.70. A page 1 story in today's Wall Street Journal highlights the role of [...]

A piece of what is now "ancient" history: on December 10, 1998, the price of a barrel of West Texas Intermediate Crude oil was $10.73. Yesterday, it was $48.70. A page 1 story in today's Wall Street Journal highlights the role of demand in helping to push up this price. And indeed, demand has risen. World oil demand was 82.2 billion barrels in the first quarter of this year, up by 2.3% over a year earlier, compared to a 10-year average of 1.6% growth.

The Journal cites the US market as the "price-setter" because it's the biggest market. With 20.77 billion barrels of consumption in Q1, it has the largest share of any country. However, that share, 25.2%, is down from about 27% in mid-1999. China's growth largely accounts for the offset. Its share in 1999 was about 5.7%, and has risen steadily to 7.6% in Q1 this year. Its demand, 6.25 billion barrels in that quarter, was up more than 19% from the year earlier period and a four-quarter moving average, 5.78 billion barrels, surpassed that of Japan, 5.50 billion, for the first time. All these Department of Energy data appear in the Haver database, "OGJ", compiled for us by the Oil and Gas Journal. Prices are maintained daily, weekly and for longer periods in USECON, WEEKLY, and DAILY.

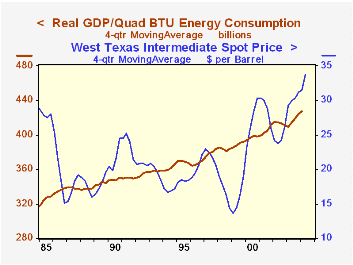

This isn't to diminish the importance of heavy energy consumption in the US. Annual data in Haver's USECON database show that as of 2002 there were 194.3 million licensed drivers in the US, but 225.9 million "personal" vehicles, that is, cars, light trucks and motorcycles. Light trucks, of course, have gained significantly as the vehicle of choice in recent years. In the early 1980s, there were fewer than 1/4 as many lights trucks on the road as there were passenger cars; in 2002, they were more than 60% as numerous as cars. Since the spring of 2001, sales of new light trucks have exceeded those of cars, so the share of these trucks in the total stock of vehicles has surely expanded even more. Trucks tend to use more gasoline than cars, so the rising volume of truck traffic would point to more gasoline consumption.

At the same time, even as energy consumption rises in the US, energy efficiency continues to increase. As evident in the second graph, the amount of GDP per unit of energy consumption (in this case, quadrillion BTUs) continues to increase. In the latest four quarters available, through Q1 this year, the gain was 3.4%, following even stronger yearly gains in the prior three quarters, averaging 4.6%. The graph further shows that energy efficiency has increased even when the price of oil has trended lower. So while the US economy is indeed a big user of energy, it is becoming more resourceful, helping to restrain the impact of energy prices on the economy. Carol Stone

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief