Global| Apr 15 2015

Global| Apr 15 2015EMU Trade Surplus Unbalances Global Growth

Summary

With global growth sputtering and the euro plunging on foreign exchange markets, the EMU region's trade surplus has reached its second highest point in at least the last 16 years. While everyone is obsessed about how low the euro can [...]

With global growth sputtering and the euro plunging on foreign exchange markets, the EMU region's trade surplus has reached its second highest point in at least the last 16 years. While everyone is obsessed about how low the euro can go and for how long it can fall, the fact is that EMU growth already is hugely befitting from the growth in economies overseas. And yet, at a time when global growth is scarce, the EMU is hogging more and more of it for its own purposes.

With global growth sputtering and the euro plunging on foreign exchange markets, the EMU region's trade surplus has reached its second highest point in at least the last 16 years. While everyone is obsessed about how low the euro can go and for how long it can fall, the fact is that EMU growth already is hugely befitting from the growth in economies overseas. And yet, at a time when global growth is scarce, the EMU is hogging more and more of it for its own purposes.

The European central bank has adopted a program of QE to stimulate a moribund economy that is being held back by ongoing austerity programs around the region. I am not arguing that the EMU should use fiscal policy instead of monetary policy. But maybe it should? The fact of the matter is that its excessive use of excessive monetary policy has pushed the euro to extremely weak levels and enhanced EMU competitiveness, driving its trade surplus- which already is large- to its second highest level in 16 years.

The point of this discussion is to make clear how exchange rates are being misused. Why is the EMU with a near-record trade surplus cheapening its currency and driving the dollar higher when the U.S. needs a weaker dollar to deal with its huge trade deficit? Exchange rates are not being used for their primary intended purpose: to help ameliorate trade and current account imbalances. They are worsening existing imbalances! They have been hijacked to make up for domestic growth shortfalls. And that leads to beggar-thy-neighbor policy issues and global instability.

When people talk of foreign exchange rates, talk usually gravitates to which currencies are over-valued or under-valued. The point is not that a country should keep a strong or a weak currency but that currency rates should be appropriate to allow two-way trade to occur in circumstances that are amenable to the evolution of free trade. Free trade is often talked about, but like the weather no one does anything about it. When exchange rates are manipulated, trade occurs at less than optimal exchange rates and leads to excesses. While countries that run surpluses are considered virtuous and those running deficits are considered to be undisciplined, the fact is that when one country runs a surplus it CAUSES another to run a deficit. The EMU surplus is causing deficits to occur elsewhere and making it harder for others to achieve a state of growth in an already difficult global environment.

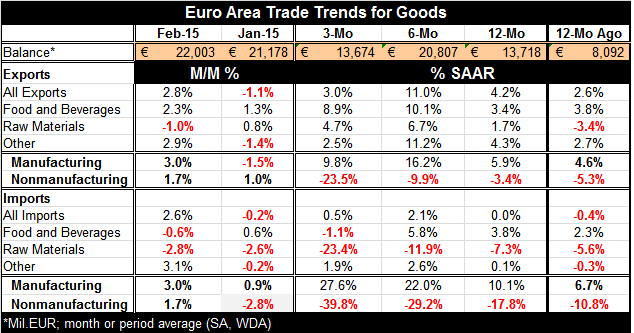

Both the chart and the table show how weak EMU imports are. The EMU is offering no increase in its domestic demand to stimulate countries outside the region. Yet, EMU exports are at 4.2% growth over 12 months and will probably accelerate as the euro continues to weaken.

The EMU is not alone in using its exchange rate to boost its domestic economy in order to make domestic tradeoffs less painful. But this sort of trade mercantilism always winds up widening the U.S. current account and trade deficits which have been in a perpetual state of deficit recently. This condition is not only non-optimal it is not sustainable and it is thrust on the U.S. because of other countries' foreign exchange practices. It also is one of the main reasons that the U.S. economy is struggling to create higher quality jobs. In a country where its currency is continually forced higher and not allowed to fall to bring its current account into balance, its labor will always expensive on world markets. It is one of the reasons that the U.S. does and cannot create competitive high quality employment. Maybe this will be the realization that someday will cause the U.S. to fight over the value of the dollar. But that day is not this day.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.