Global| Jul 20 2015

Global| Jul 20 2015EMU Trade Surplus Drops

Summary

Exports and the EMU trade surplus fell in May. Exports fell by 1.5%. Imports were flat. The trade surplus fell to 21.2 billion euros in May from 23.9 billion euros in April. Exports fell on a broad front in May with manufacturing [...]

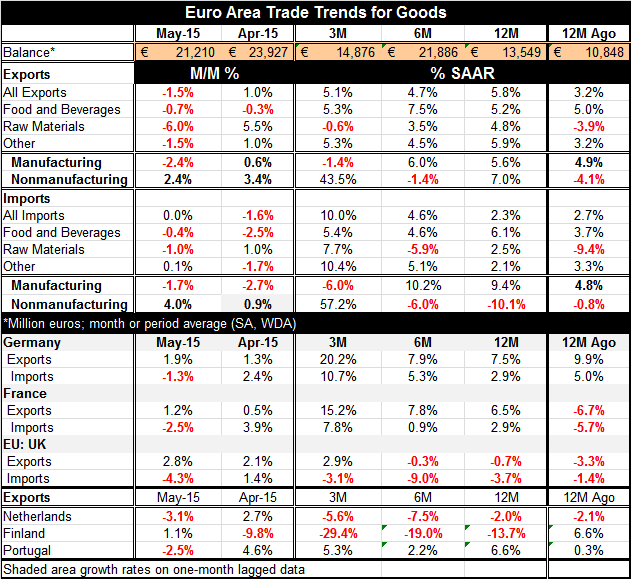

Exports and the EMU trade surplus fell in May. Exports fell by 1.5%. Imports were flat. The trade surplus fell to 21.2 billion euros in May from 23.9 billion euros in April.

Exports and the EMU trade surplus fell in May. Exports fell by 1.5%. Imports were flat. The trade surplus fell to 21.2 billion euros in May from 23.9 billion euros in April.

Exports fell on a broad front in May with manufacturing exports off by 2.4%. Nonmanufacturing exports rose by 2.4% to buffer the overall drop. Over 12 months, six months and three months, total exports continue to grow at an approximately 5% annualized pace. However, the bellwether, manufacturing exports, are lower, falling at a 1.4% pace over three months.

Imports into the euro area are flat in May after falling by 1.6% in April. But overall imports are showing acceleration as growth steps up from 2.3% over 12 months to 4.6% over six months to 10.0% over three months. Rising imports are a sign of strengthening domestic demand even though they tend to widen the trade deficit or erode the surplus.

However, on closer inspection, much of the import strength turns out to be in nonmanufacturing goods. As imports on nonmanufacturing goods rose at a 57% annual rate over three months, that strength masked that manufactured goods imports were falling over three months at a 6% annual rate. Still, manufacturing imports are rising at about a 10% pace over six months and 12 months. As a result, the import picture is in flux and confusing.

By country, exports are accelerating in France and Germany. Exports are growing steadily in Portugal. But the Netherlands and Finland show sharp weakness in exports. These flows mirror the strength of the underlying economies in the EMU.

The country-level results remind us that the exchange rate may be a palliative, but it is not a cure-all. The weak and weakening euro has not succeeded in bringing growth to all the EMU economies. Countries must first have their own houses in order to benefit from a weak exchange rate. Even heavily export-oriented economies need a stable structure at home to exploit trade. They also need export markets that are growing. Since many EMU member country exports stay in the EMU, that is a problem.

Overall the EMU gauges for growth in this report hit a speed bump in May and also over the last three months. Over those periods, manufacturing exports declined along with manufacturing imports. These trends leave us skeptical of the performance of the EMU economy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief