Global| Mar 30 2009

Global| Mar 30 2009EMU Still Sinking In EU Index Report

Summary

In the EMU framework it is pretty clear that things are not going very well. In the March report even though the Markit (formerly Reuter) PMIs had bottomed and risen, the similar gauges from the EU Commission show no such trend. [...]

In the EMU framework it is pretty clear that things are not going very well. In the March report even though the Markit (formerly Reuter) PMIs had bottomed and risen, the similar gauges from the EU Commission show no such trend. Indeed, the EU Commission framework shows universal weakness and near universal worst case readings. The overall sentiment index as at a low as is the industrial measure, consumer confidence, and the service sector barometer. Above their lowest readings are the retail and construction sectors each of which is still in about the lower 10% of its respective range. And that’s as good as it gets - bottom 10% - a clear ‘F’ if we were grading.

Moreover, the overall sentiment gauges for EMU are at their lowest in EMU as a whole, in Germany and in Italy . The UK , an EU member, is also on a low. France and Spain are not at their respective all time (since 1985) lows, but are not far from them.

If we turn to the industrial sector details we find that most of the component readings are at or near all time lows except for inventories; they are in the top 10% of their range – not a good ‘top-10’ reading at all.

Consumer confidence is also at its all-time low although its components are not so universally at extremes. Still, the economic situation in the past 12-months and expectations for the next 12-months are each at all time lows. The environment for making major purchases now is only ‘only’ in the bottom 30% of its range. For the next 12months the reading is in the bottom 15% of its range, a bit worse that eh current reading: that is not good. Still the consumer does not seem as beleaguered as the industrial sector. German and French consumer responses are at all-time lows. Italy , the UK and Spain are, respectively, in the bottom 17th, 17th and 9th percent of their ranges.

With the consumers not being as impacted as badly as industry it is not surprising that the retail sector is ‘only’ in the bottom 10% of its range. Across the largest EMU/EU countries the results are even better. In France the responses are only in the bottom 63rd percentile of their range (top 37%!), Italy’s retail sector is in the bottom 34th percentile, Germany and Spain are in the lower 20th percentile and the UK is the weakest in the bottom 17th percentile.

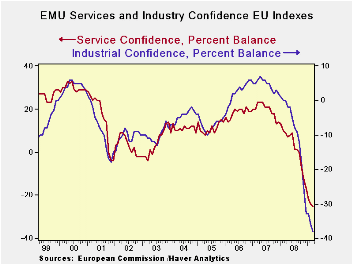

The services sector has no bright spots or readings. The overall gauges for EU is at its all time low as are all its component readings; the main countries have readings that are at their all-time lows or quite near them.

Construction as a sector is in the lower 25th percentile of its range on an EU-wide basis. Across countries, Germany and Italy show near midpoint readings in construction; France is a 30th percentile reading; the UK is a bottom 25th percentile reading; Spain is a bottom 20 percentile reading.

Expected and current employment readings are at their worst or bottom 10% across the various sectors with the obvious exception of the expected unemployment reading which is at an all time high.

The EU/EMU is a still every weak region. It is not showing the upward momentum or abatement of downward momentum that is becoming increasingly common in the US . Its leaders are less active in implementing new stimulus programs, although in fairness, Europe in general has a better social safety-net than does the US . Still As I pointed out at the time of the Obama plan, ‘cushion’ is not ‘stimulus’.

| EU Sectors and Country level Overall Sentiment | R-SQ | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| EU | Mar 09 |

Feb 09 |

Jan 09 |

Dec 08 |

%tile | Rank | Max | Min | Range | Mean | w/ Overall |

| Overall | 60.3 | 60.9 | 63.2 | 66.6 | 0.0 | 220 | 116 | 60 | 56 | 99 | 1.00 |

| Industrial | -39 | -37 | -33 | -32 | 0.0 | 220 | 7 | -39 | 46 | -8 | 0.89 |

| Consumer Confid | -32 | -32 | -31 | -28 | 0.0 | 219 | 2 | -32 | 34 | -11 | 0.86 |

| Retail | -22 | -24 | -25 | -25 | 9.7 | 217 | 6 | -25 | 31 | -6 | 0.62 |

| Construction | -38 | -38 | -36 | -32 | 8.9 | 205 | 3 | -42 | 45 | -18 | 0.44 |

| Services | -31 | -29 | -28 | -23 | 0.0 | 145 | 32 | -31 | 63 | 15 | 0.87 |

| % m/m | Mar 09 |

Based on Level | Level | ||||||||

| EMU | -1.1% | -2.8% | -2.5% | 64.6 | 0.0 | 220 | 117 | 65 | 52 | 99 | 0.96 |

| Germany | -1.1% | -1.6% | -4.0% | 72.4 | 0.0 | 220 | 121 | 72 | 48 | 99 | 0.70 |

| France | -1.3% | -0.9% | -0.7% | 73.1 | 2.4 | 219 | 119 | 72 | 47 | 99 | 0.81 |

| Italy | -6.3% | -0.4% | -1.4% | 67.1 | 0.0 | 220 | 121 | 67 | 54 | 99 | 0.82 |

| Spain | 1.2% | -3.2% | 3.7% | 67.8 | 2.2 | 218 | 117 | 67 | 50 | 100 | 0.72 |

| Memo:UK | -0.7% | -6.3% | -10.9% | 56.0 | 0.0 | 220 | 117 | 56 | 61 | 100 | 0.58 |

| Since 1990 except Services (Oct 1996)247 | -Count | Services: | 145 | -Count | |||||||

| Sentiment is an index, sector readings are net balance diffusion measures | |||||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief