Global| Feb 04 2009

Global| Feb 04 2009EMU Services PMI's Slow Descent Signal In January

Summary

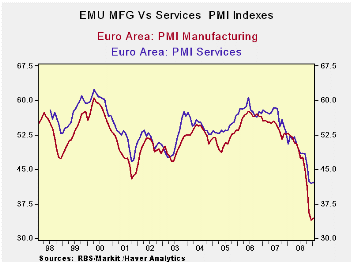

The EMU Services PMIs from Market show continued weakness in EMU and UK service sectors but not accelerating weakness. The signal for the Zone is just one month up from its low. Country indices are low in their respective ranges, but [...]

The EMU Services PMIs from Market show continued weakness in

EMU and UK service sectors but not accelerating weakness.

The signal for the Zone is just one month up from its low.

Country indices are low in their respective ranges, but generally they

are not on their bottoms. Germany for example saw its service sector

slip further this month; it now lies in the bottom 10 percentile of its

range. Italy and the UK each saw some of their weakness dissipate yet

they remain the worst tow countries with the lowest services diffusion

readings in this grouping. . The EU Commission’s measures on services

and confidence are generally a bit weaker and are at or nearer all time

lows compared to the Market treatment for services.

The bounce in services in Europe is echoed by the bounce in

the US non-MFG ISM, the closest US measure to these European service

sector indices. The US ISM is in the bottom 23% of its range. Europe

and the US seem to be passing though this cycle with remarkably similar

impacts on their respective goods and services sectors.

| NTC Services Indices for EU/EMU | |||||||

|---|---|---|---|---|---|---|---|

| Jan-09 | Dec-08 | Nov-08 | 3Mo | 6Mo | 12Mo | Percentile | |

| Euro-13 | 42.16 | 42.06 | 42.47 | 42.23 | 44.89 | 47.77 | 0.5% |

| Germany | 45.20 | 46.57 | 45.14 | 45.64 | 47.81 | 50.40 | 10.7% |

| France | 42.56 | 40.57 | 46.17 | 43.10 | 45.84 | 49.27 | 8.0% |

| Italy | 41.10 | 40.30 | 39.46 | 40.29 | 44.07 | 46.03 | 7.0% |

| Spain | 31.84 | 32.10 | 28.23 | 30.72 | 33.24 | 37.17 | 11.1% |

| Ireland | 33.94 | 34.14 | 32.60 | 33.56 | 36.23 | 40.52 | 3.7% |

| EU only | |||||||

| UK (CIPs) | 42.48 | 40.21 | 40.06 | 40.92 | 43.38 | 46.76 | 11.8% |

| US NONFMG ISM | 42.90 | 40.10 | 37.40 | 40.13 | 44.23 | 47.21 | 22.9% |

| EU Commission Indices for EU and EMU | |||||||

| EU Index | Jan-09 | Dec-08 | Nov-08 | 3Mo | 6Mo | 12Mo | Percentile |

| EU Services | -28 | -23 | -18 | -28.67 | -24.67 | -19.67 | 0.0% |

| EMU | Jan-09 | Dec-08 | Nov-08 | 3Mo | 6Mo | 12Mo | Percentile |

| Services | -22 | -17 | -12 | -17.00 | -9.50 | -2.58 | 0.0% |

| Cons Confidence | -31 | -30 | -25 | -28.67 | -24.67 | -8.28 | 0.0% |

| Consumer confidence by country | |||||||

| Germany-Ccon | -27 | -22 | -15 | -21.33 | -15.67 | -9.50 | 0.0% |

| France-Ccon | -35 | -34 | -29 | -32.67 | -29.50 | -23.75 | 0.0% |

| Ital-Ccon | -26 | -30 | -26 | -27.33 | -25.17 | -24.17 | 12.5% |

| Spain-Ccon | -44 | -46 | -44 | -44.67 | -42.33 | -35.58 | 4.2% |

| UK-Ccon | -35 | -29 | -27 | -30.33 | -27.50 | -21.50 | 0.0% |

| percentile is over range since May 2000 | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief