Global| Sep 02 2014

Global| Sep 02 2014EMU PPI Is Still Declining

Summary

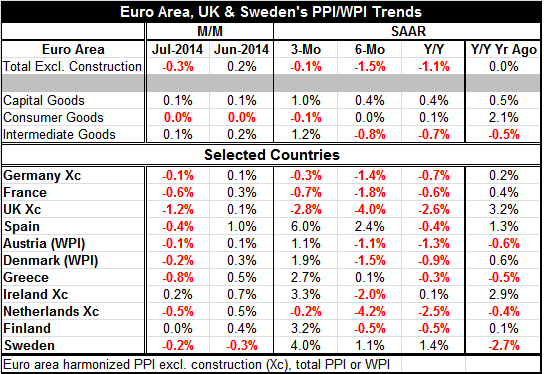

The EMU PPI fell in July and its 1.1% year-over-year drop is the largest since April. Capital goods prices are eking out gains over all horizons (in the table), but the increases are marginal. Consumer goods prices over all horizons [...]

The EMU PPI fell in July and its 1.1% year-over-year drop is the largest since April. Capital goods prices are eking out gains over all horizons (in the table), but the increases are marginal. Consumer goods prices over all horizons are a tick either side of flat. Intermediate goods prices are falling over 12 months and six months but are rising at a 1.2% annual rate over three months.

The EMU PPI fell in July and its 1.1% year-over-year drop is the largest since April. Capital goods prices are eking out gains over all horizons (in the table), but the increases are marginal. Consumer goods prices over all horizons are a tick either side of flat. Intermediate goods prices are falling over 12 months and six months but are rising at a 1.2% annual rate over three months.

Headline PPI trends show declines on all horizons with the 3-month pace barely lower at -0.1% saar. Producer prices look to be weak everywhere and on all horizons - but perhaps not weakening further.

Looking at the profiles of eleven EMU members, we see PPI drops in all but two members in July, a contrast to increases in 10 of 11 members in June.

Over three months PPI prices are falling in only 4 of 11 members, but PPI prices are falling in 7 of 11 over six months and in 9 of 11 over 12 months.

There is less breadth for the PPI weakness over three months, but the three-month reading is erratic. We can see that in the difference in the breadth of declines in June vs. July.

We see continued PPI weakness because of ongoing weakness in manufacturing. Germany's manufacturing PMI for August reported yesterday was last lower in September 2013. Even France, a country that has been struggling, saw conditions worsen; they were last weaker in May 2013. Italy's PMI was last weaker in June 2013. Spain was last weaker in April 2014. That is a lot of weaknesses in the big four EMU members. There can't be too much surprise that producer prices are slumping again.

EMU trends for prices, output and growth in general are still being adversely impacted by the events in Ukraine which seem to have gotten worse. Ukraine is now referring to Russian intervention as `undisguised.' News reports are saying that Russia will be adopting a new military strategy with more troops on its eastern front to be ready to help when the needs arises. This has all the look of a new more aggressive cold war posture.

I wonder if the western forces are going to let Russian continue to push into Ukraine and effectively to partition it. Russia could control a big bite of it and allow Russia to imperil all the other former eastern bloc nations to which it may at some point wish to lay claim (because there are Russians living there). In the future there is also the issue of European dependence on Russian energy supplies. Between that and an increased military presence, Europe will be feeling a definite pinch. Is that where we are heading? Isn't this the time to head it off?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief