Global| Jan 02 2015

Global| Jan 02 2015EMU PMI Gauges Weaken as Divergence Reappears

Summary

Weakness is a problem for the European Monetary Union and it has been a problem of increasing magnitude - if not worry- over the course of 2014. But a bigger problem for EMU is divergence. In 2013 the divergence among EMU member [...]

Weakness is a problem for the European Monetary Union and it has been a problem of

increasing magnitude - if not worry- over the course of 2014.

But a bigger problem for EMU is divergence. In 2013 the divergence

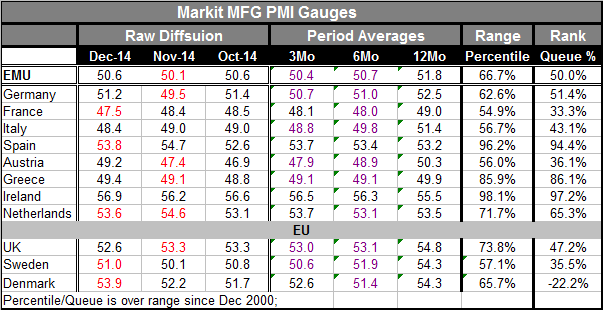

among EMU member manufacturing PMIs fell sharply and, since then,

the differences among members (those reporting this month) came into closer

alignment for a while. But in the past two months a greater divergence has emerged.

Divergence is a difficult problem for EMU since it has only a single monetary

policy that applies to the whole of the union. There is no EMU-wide fiscal

policy and several weak members are bumping up against fiscal rules eliminating

the possibility of unilateral stimulative action. Moreover, the ECB has no mandate

for addressing growth weakness and is only formally responsible for inflation relativ

e to its 'target' of 2% (something close to but less than 2%).

Weakness is a problem for the European Monetary Union and it has been a problem of

increasing magnitude - if not worry- over the course of 2014.

But a bigger problem for EMU is divergence. In 2013 the divergence

among EMU member manufacturing PMIs fell sharply and, since then,

the differences among members (those reporting this month) came into closer

alignment for a while. But in the past two months a greater divergence has emerged.

Divergence is a difficult problem for EMU since it has only a single monetary

policy that applies to the whole of the union. There is no EMU-wide fiscal

policy and several weak members are bumping up against fiscal rules eliminating

the possibility of unilateral stimulative action. Moreover, the ECB has no mandate

for addressing growth weakness and is only formally responsible for inflation relativ

e to its 'target' of 2% (something close to but less than 2%).

Call to action for the ECB The EMU continues to see price level undershooting. Today, Mario Draghi, head of the ECB, noted that if undershooting were to continue, action would be required. "The risk that we don't fulfill our mandate of price stability is higher than it was six months ago," Draghi said in an interview with German newspaper Handelsblatt. "We are in technical preparations to alter the size, speed and composition of our measures at the beginning of 2015, should this become necessary, to react to a too-long period of low inflation. There's unanimity in the ECB council on that."

Central banks have different target-miss responses This puts the ECB on guard for the ongoing inflation undershoot that is mostly likely to persist in the wake of falling global oil prices. And, unlike the Fed that clearly has plans to RAISE rates in 2015 even as its long inflation undershoot continues, the ECB apparently is prepared and its members are unanimous in their assessment of the need to take action on the undershoot. The reference to unanimity is the most important part of this statement by Draghi, but agreeing that the undershoot should be addressed and deciding how to do that will be two different things.

Since central banks do not have a magic key to raise or lower inflation, the ECB will take steps, probably enacting program of QE to try to reflate growth and prices too.

Policy limitations What we can see from the manufacturing sectors in Europe it that substantial differences remain among members. There is no ECB policy of fine tuning that would allow more stimulus to go one place compared to another. And we still have to wonder the extent to which the ECB's actions will be as bold as Draghi's words.

EMU weakness getting worse In addition to the weakness and the differences in conditions among members, there is some evidence that weakness is cumulating. For EMU as whole the average PMI level deteriorates steadily when calculated over 12-months, then six months, then three months. That is true for several member states: Germany, Italy, Austria and Greece and it is almost true for France, but for a tick higher in its 3-month average. Only Spain and Ireland have a progression of values that show acceleration. In the EU-only members reporting this month, the U.K. and Sweden also demonstrate steady erosion in their Manufacturing PMIs.

Some members are doing better Spain is unique and the standing of its PMI reading is quite high, residing as it does in the 94th percentile of its historic rank of data - higher less than 6% of the time. Ireland is even stronger in relative terms standing in the 97th percentile of its queue. Greece has been so weak that its sub-growth 49.4 raw diffusion score stands in the 86th percentile of its historic queue of data-higher only 14% of the time! But France stands in its 33rd queue percentile, Italy is in its 43rd percentile, and Austria is in its 36th percentile. Germany stands only in its 51st queue percentile and in December it moved back into a phase of expansion from a one month contraction.

The danger of a slow policy response The ECB has been slow in adopting QE - if it does adopt it as we expect. Within the last month- despite today's comment by Draghi, Jens Weidmann, head of the Bundesbank, stated that he would be opposed to QE even if there were deflation. The Germans are now at risk to their own opposition. They have opposed QE for so long that if it commences soon, the prospect that QE will ultimately inflict losses on the ECB and require fiscal coverage down the road (from Germany!) is likely. When QE is begun with interest rates so low, it is more likely that when the QE-accumulated assets are liquidated their yields will be higher and their prices lower, inflicting loss on the central bank. This, I think, is the reason for ongoing German opposition to QE. The more that QE is needed, the more that markets respond by pushing yields lower, increasing the financial risk of a QE operation - creating a sort of financial markets Catch 22. QE may or may not revive Europe. But its instruments are likely to inflict dangerous losses on the ECB itself, unless the ECB takes steps to limit these losses. It could keep QE very small so that the losses are negligible or only it could accumulate relatively short term assets. In either case the bang from QE would be diminished.

Policy issues for 2015 It seems that despite unanimity, the ECB may have a hard time putting Draghi's words into effective action. Meanwhile, few community members show any real strength and several important members are showing a degrading trend for MFG, enough to impart that trend to the EMU has a whole.

My caution for 2015 is to be careful about getting too optimistic about (1) what the ECB will do, and (2) what impact that will have. Meanwhile, the stimulus from lower energy prices is at the behest of Saudi Arabia whose own eventual interests are NOT to keep prices so low. We should be careful about depending too much on the kindness of strangers.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief