Global| Mar 27 2009

Global| Mar 27 2009EMU Orders: Still Sinking Fast

Summary

Egad! Still very weak: Euro industrial orders continued their steep rate of decline in January. The 3.4% mo/mo drop was less than the 8% plunge in December and the 9.4% stunner in November, but it fell far short of being reassuring. [...]

Egad! Still very weak: Euro industrial

orders continued their steep rate of decline in January. The 3.4% mo/mo

drop was less than the 8% plunge in December and the 9.4% stunner in

November, but it fell far short of being reassuring.

Weak Q1 in train, too: The three month pace

of decline is 57% at an annual rate. The rate of decline in the quarter

is also at a -50% annual rate. So 2009-Q1 is not an encouraging number

to look forward to at this point.

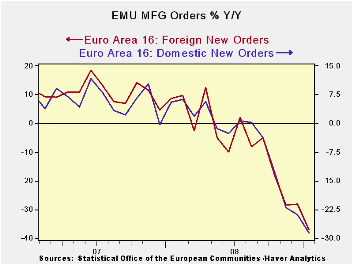

Imported weakness for Europe: The

domestic/foreign split for orders is somewhat illuminating. Domestic

orders fell at by 3.9% from December. Foreign orders fell by 7.3%. The

pace of decline for past growth rates also shows that the domestic rate

of decline has lagged the pace of the foreign orders decline. But that

growth gap has become more pronounced this month with domestic orders

off by so much less than foreign orders. Clearly the EMU is importing

weakness from abroad. Its foreign orders and exports are falling at a

faster pace than its domestic activity.

Dissent at home: While the ECB is coming

under more criticism from business groups (today it is Business Europe,

which represents national business federations and industry groups) the

industrial orders data strongly suggest that the pulse of weakness is

from beyond the ECBs border and reach. That does not mean that the ECB

or that fiscal stimulus could not make up for it, but that there is a

continuing drag of controllable influence on the euro-economy.

A glint or two of good news: Still, it is

encouraging that the Markit PMI indices for services and for MFG turned

higher in March. Today the CEPR index of activity echoed that signal

and turned just a little bit less negative in March compared to

February. This sort of statistic is not bankable but it is indicative

of an economy that may be passing from its most severe phase of

negative growth to a milder phase and perhaps eventually headed to

recovery.

Looking ahead to March data… For the bulk

of Euro-data the readings remain dispirited and grim. But the March

reports which are so few in number have begun to stake out a less

negative view. There it is: the precursor to a positive view. Not to

get too excited yet, but this is the way that the rebound will start.

So despite the discouraging data on the day the there is some good news

in train but it’s only found in the freshest of reports. That means we

are apt to see better news for COUNTRY level data first, since the EMU

reports lag the timeliest of national reports.

| E-zone-13 and UK Industrial Orders And Sales | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Saar except m/m | Mo/Mo | Jan-09 | Dec-08 | Jan-09 | Dec-08 | Jan-09 | Dec-08 | ||

| E- AREA Detail | Jan-09 | Dec-08 | Nov-08 | 3-Mo | 3-Mo | 6-mo | 6-mo | 12-mo | 12-mo |

| MFG Orders | -3.4% | -8.0% | -9.4% | -57.9% | -63.9% | -50.1% | -46.2% | -32.0% | -28.0% |

| MFG Sales | #N/A | -3.5% | -3.9% | #N/A | -34.7% | #N/A | -24.0% | #N/A | -11.6% |

| Consumer | #N/A | -0.4% | -0.4% | #N/A | -4.9% | #N/A | -4.3% | #N/A | -2.9% |

| Capital | #N/A | -1.7% | -2.1% | #N/A | -20.3% | #N/A | -16.1% | #N/A | -8.7% |

| Intermediate | -3.9% | -5.9% | -8.4% | -52.8% | -56.1% | -46.9% | -40.8% | -28.6% | -23.8% |

| Memo: MFG | |||||||||

| Total Orders | -3.4% | -8.0% | -9.4% | -57.9% | -63.9% | -50.1% | -46.2% | -32.0% | -28.0% |

| E-13 Domestic MFG orders | -3.9% | -5.9% | -8.4% | -52.8% | -56.1% | -46.9% | -40.8% | -28.6% | -23.8% |

| E-13 Foreign MFG orders | -7.3% | -7.1% | -10.3% | -64.4% | -64.0% | -56.2% | -45.5% | -37.2% | -28.1% |

| Countries: | Jan-09 | Dec-08 | Nov-08 | 3-Mo | 3-Mo | 6-mo | 6-mo | 12-mo | 12-mo |

| Germany (MFG): | -7.6% | -8.1% | -7.5% | -61.9% | -61.3% | -52.5% | -46.3% | -35.0% | -30.3% |

| France (Ind): | -2.5% | -2.0% | -6.6% | -36.6% | -52.1% | -44.6% | -36.5% | -28.0% | -23.3% |

| Italy (Ind): | #N/A | -2.0% | -6.6% | #N/A | -47.2% | #N/A | -31.4% | #N/A | -18.4% |

| UK (Engineering Ind): | -25.2% | 26.1% | -11.9% | -52.3% | -33.0% | -39.7% | 5.0% | -34.4% | 1.7% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief