Global| Nov 13 2019

Global| Nov 13 2019EMU IP Registers Second Monthly Gain in a Row

Summary

EMU area IP ticked up by the smallest amount in September, rising by 0.1% after August's 0.4% gain. Still, in the just completed quarter, IP is falling at a 3.5% annual rate. Manufacturing output is up for two months running by 0.4% [...]

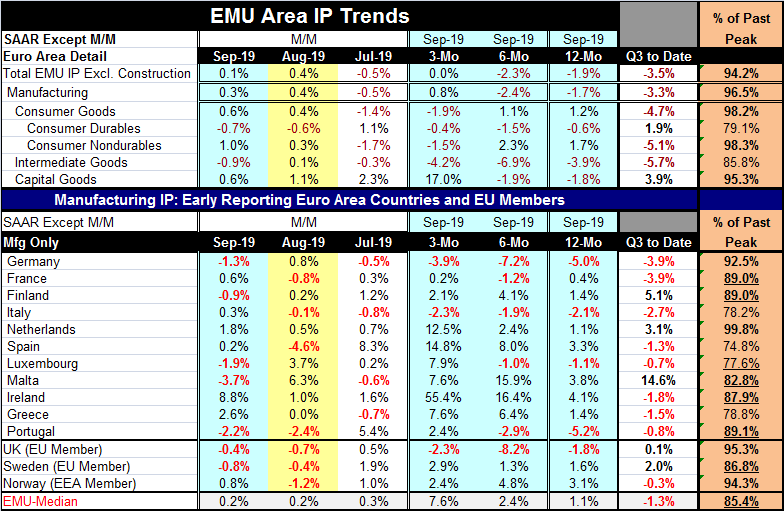

EMU area IP ticked up by the smallest amount in September, rising by 0.1% after August's 0.4% gain. Still, in the just completed quarter, IP is falling at a 3.5% annual rate. Manufacturing output is up for two months running by 0.4% and 0.3% but it is also falling at a 3.3% annual rate in Q3.

EMU area IP ticked up by the smallest amount in September, rising by 0.1% after August's 0.4% gain. Still, in the just completed quarter, IP is falling at a 3.5% annual rate. Manufacturing output is up for two months running by 0.4% and 0.3% but it is also falling at a 3.3% annual rate in Q3.

In the quarter-to-date, which is now the completed third quarter, output is falling in all IP categories except consumer durables and capital goods. The capital goods gain is robust and is all the result of a gain over the last three months.

Of the eleven EMU countries that report manufacturing IP in the table, five show output declines in September, four showed output declines in August and four in July.

Over three months, only Germany and Italy show declines in manufacturing IP. Over six months, Germany, France, Italy, Luxembourg and Portugal show output declines. Over 12 months, there are declines in Germany, Italy, Luxembourg and Portugal.

Accelerating vs. decelerating trends

Italy and Germany are the 'stalwarts of the output decline.' Moreover, a series of countries have output that is progressively accelerating from 12-months to six-months to three-months. Manufacturing output in six countries is persistently accelerating: The Netherlands, Spain, Luxembourg, Ireland, Greece, and Portugal. However, in opposition to this trend, output by sector across EMU shows consumer goods output progressively decelerating. Intermediate goods output is persistently declining but not quite decelerating. The output of capital goods is almost on an accelerating profile.

'Accounting' data show more firmness

The traditional accounting data approach that counts up output that allows calculations of rates of growth of output (the way IP data are gathered) now shows a better trend than even more up-to-date survey data. Survey data ask a question like 'is output higher, lower or the same?' then it creates an index out of such responses. This sort of survey is much less precise than adding up actual numbers representing sales or output, but such surveys are much more topical and easier for firms to answer. These sorts of surveys continue to show weakness. The ZEW survey of German financial experts' opinion showed a nearly unprecedented improvement in November, but those experts still saw output declines in most of the major G6 countries and in the EMU and a sour outlook. Even survey data are showing some tendency for conditions to improve. But there is still a question about how much growth will develop and how sustainable will it be.

Different results from different approaches

Other surveys also show weakness and rather widespread declines in manufacturing globally. The Markit PMI survey shows output is declining in the manufacturing sector in the EMU and in three of its four largest economies. A U.S. survey, the ISM, shows manufacturing output is declining. In a group of ten major Asian economies, only two have manufacturing PMI readings above 50, indicating expansion. So while the PMI readings are uniformly weak and mostly showing contraction, for manufacturing in EMU the accounting data that is real and that 'counts up' actual output shows that expansion has been in gear in the EMU for two months running.

The outlook

Monetary policy globally is already full-tilt on expansion. In Europe, conservative forces are trying to pull back on negative interest rates even though inflation in the EMU and across its largest economies is still significantly below its targeted rate. As central banks lose some of their fear of recession and as we have seen market interest rates rise especially in the U.S., where the inversion of the yield curve also has unwound, there is some danger that policy is losing its fear of economic weakness faster than the risk of economic weakness itself is dissipating.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief