Global| Apr 10 2015

Global| Apr 10 2015EMU IP Makes Progress Amid Unevenness

Summary

The European economics continue to show a good deal of interregional disparity, but for the most part trends in production are improving. In the EMU in February only three of the early reports showed monthly IP declines, down from [...]

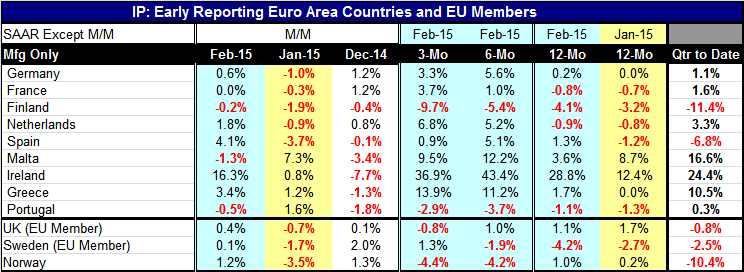

The European economics continue to show a good deal of interregional disparity, but for the most part trends in production are improving. In the EMU in February only three of the early reports showed monthly IP declines, down from five in January and six in December. Over three months and six months only two members show declines in IP while over 12 months four show weaker manufacturing sectors. But one year ago fully six had manufacturing sectors that were lower year over year. Progress is being made.

The European economics continue to show a good deal of interregional disparity, but for the most part trends in production are improving. In the EMU in February only three of the early reports showed monthly IP declines, down from five in January and six in December. Over three months and six months only two members show declines in IP while over 12 months four show weaker manufacturing sectors. But one year ago fully six had manufacturing sectors that were lower year over year. Progress is being made.

More topically the quarter-to-date data show IP declining in only two of nine EMU members while the three European non-EMU members in the table each are showing a drop in IP.

Spain is logging consistently positive growth rates. France is accelerating out of a period of weakness. German output is growing but without a clear trend. Over three months and six months Greece Ireland and tiny Malta have essentially double digit growth rates in IP. Yes, even as Greece protests austerity, it seems to be working to bring back the moribund Greek manufacturing sector.

Finland is showing pronounced steady deceleration in IP with negative growth rates. Portugal, too, is experiencing substantial persistent contraction. Outside of the EMU, the U.K. and Norway have consistently decelerating manufacturing sectors. Sweden is on an up swinging trend.

OECD Leading Indicators Provide Perspective

The recently released OECD leading economic indicators show the EMU region to be slowly improving as its LEI has ticked up for the last two months running through February. Within EMU Austria, Belgium and Germany are the only countries showing a weakening pattern over six months, the OECD's preferred horizon for inspecting these trends. Spain and Ireland have the two strongest uptrends in the EMU.

As for the global environment, the OECD region has dead flat momentum over six months. The EMU and Japan have some positive momentum, but the U.S. and the U.K., while still growing, have momentum slipping over six months along with China.

Globally inflation is low and our best economic minds are trying to sort out why we are stuck in this predicament. Each country has its own special circumstance, but there is no doubt that it is a worldwide morass. However, there is progress being made. Six months ago eight of 12 of these EMU countries had fading momentum; globally only the U.S. had a momentum upswing with the U.K., the EMU, Japan and China each in a state of withering momentum. Even though the current situation is uneven there has been progress with positive momentum now more the rule than the exception.

The risk to growth going forward is in managing the stresses that differing local policies have placed on the global economy. The dollar has become exceptionally strong with the euro and yen each weakened substantially. Using exchange rate policies to get a boost for growth is like robbing Peter to pay Paul. It merely redistributes the beneficiaries of growth and does not create and new growth for the global economy. The world economy still needs some real growth and it is not clear that despite having logged progress that what has worked over the last six months will continue to be effective over the next six months or more.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.