Global| May 16 2018

Global| May 16 2018EMU Inflation Bumps Up But Remains Well Below Target As Other Problems Boil Over

Summary

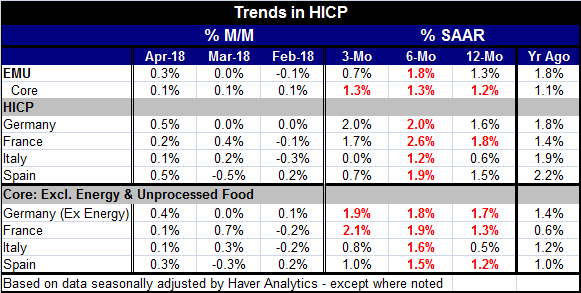

EMU core and headline inflation rates continue to grow at rates that are at a significant discount to their objective (which is just a bit below 2%). Headline inflation grew by 0.3% in April, but the core only rose by 0.1%. Still, [...]

EMU core and headline inflation rates continue to grow at rates that are at a significant discount to their objective (which is just a bit below 2%). Headline inflation grew by 0.3% in April, but the core only rose by 0.1%. Still, headline inflation at 1.3% year-over-year is below where it was one year ago at this time (1.8%). On the other hand, core inflation, despite its small uptick in April, is up by 1.2% year-on-year, a tick faster than its year-ago pace of 1.1%.

The inflation focus

Looked at by country, Germany and France are experiencing higher inflation calculated sequentially over 12-month to six-month to three-month. French inflation does decelerate again from six-month to three-month, but its three-month pace is nearly the same as its year-on-year pace. Italy and Spain both experienced higher inflation over six months than over 12 months, but then over three months, inflation dips back below the year-on-year pace and by substantial amounts.

Core inflation shows ‘unusual’ trends too

Core inflation finds German inflation brushing by at near target paces at 1.7% over 12 months, 1.8% over six months and 1.9% over three months. The all-important 12-month pace is the lowest at 1.7%. France also shows steady core acceleration with a 1.3% 12-month gain, a 1.9% six-month gain vs. a 2.1% three-month gain. Italy and Spain both show core inflation higher over six months than over 12 months. But both inflation is then lower over three months than for six months, and for each the three-month annualized rate of inflation is below 1%.

A Biblical twist on inflation

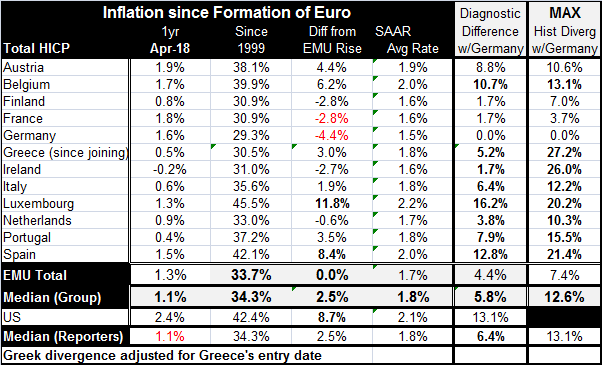

Looking at the full list of original EMU members, we see an interesting twist. Since the EMU was formed, only Germany and France have consistently run inflation rates below the weighted average for the EMU as a whole. But as of April, Germany has the fourth highest year-on-year rate in this group of 12 nations. Ireland shows price declines. Portugal, Italy and Greece currently have the next lowest rates of inflation among ‘original’ EMU members. With these results, the EMU has been turned on its head. The former low inflation country is now a high inflation country and the former high inflation country is now a low inflation country. The R-square relationship between year-on-year inflation and EMU formation-to-date calculated from the start of the EMU produces a value of 0.07- this is not significantly different from zero, implying no relationship. Historic inflation rankings among EMU members bear less than a 10% correlation to its past. It’s no wonder that the EMU has something of biblical proportions going on (the first shall be last and the last shall be first).

Still, it is not clear how long things will stay this way in the EMU. There have been restive movements in Greece that subsequently were quelled. Spain and Portugal also spawned their own movements of dissent. Perhaps these have come to be inspired by the U.K.’s departure from the EU. Spain’s Catalans have made one attempt at secession, one that may not have had the full support of all the Catalan residents. But these disturbances seem to be nothing compared to Italy, the euro area’s third largest economy where the Five Star movement is promising to declare war on the EU’s budget rules. It has a massive domestic spending agenda and has requested debt forgiveness equivalent to $294bln.

This may prove to be the sternest test of the EMU so far. Italian GDP peaked in Q1 2008. And I do mean Italian GDP, not its rate of growth. In the ensuing recession and ‘recovery’ Italy’s GDP is some 4.5% below its peak reached ten years ago.

This may prove to be the sternest test of the EMU so far. Italian GDP peaked in Q1 2008. And I do mean Italian GDP, not its rate of growth. In the ensuing recession and ‘recovery’ Italy’s GDP is some 4.5% below its peak reached ten years ago.

It is no wonder that there has been a huge backlash in Italy to the policies enforced by the EU under the supervision of the Germans who would not brook deviation from the rules. These are the same Germans that run persistent and massive current account surpluses and have prioritized fiscal surpluses choosing not to pay its annual fee to NATO (...again). Apparently, the Germans get to decide what rules will be obeyed and by whom.

Italian consumer confidence belies the unrest there

Italy’s Five Star movement and other obstreperous parties have been building strength amid the dissent in Italy that has been covered over by what have been strong consumer confidence readings! Clearly there has been a great deal of unrest in Italy that has found a political channel even as Italian consumers were giving ‘nice’ responses to consumer confidence surveys.

The importance of Italy

While all eyes are on North Korea, China Trade, Israel & Palestine, Brexit, NAFTA, and various Donald Trump issues in the U.S., what might be the biggest international disturbance of all is floating by unobserved right before our eyes. Italy is not Greece. It is not some messy toothpaste that can be crammed back into the tube as Greece was. Italy is still the third largest economy in the EMU. It is an important member of the EMU, a charter member and one whose interest in European integration goes back to the European Iron and Steel Community in 1951 formed by the Treaty of Paris. This arrangement is considered to be forbearer of the formation of the EU which was formally started under the treaty of Rome in 1957 coming into force in 1958. The loss of Italy to the EMU and EU would be the loss of not just a founding member but a country that historically has been a keystone to the formation of this community and what it stands for.

Is the winner determined by the scorekeeper?

It is too soon to tell how this will play out. Italy may be find a way to stay in the EU and EMU. But the rise of the Five Star movement and its drastic agenda is a testament to the warning I offered at the start of this process... that the incredible pressure that was put on these high inflation countries to make them conform with rules that has long been ignored could have profound consequences. What Europeans called ‘internal devaluation’ was a thinly disguised program of deflation that raged in Greece and also in Italy and has had substantial negative impact on Spain and Portugal as well. As much as the inflation results seem to speak of success, that is simply a statement about who is keeping score: the Germans. Were we to score this by unemployment rates, the losers are the former ‘high inflation’ group led by Greece, Spain and Italy. France is undergoing a national rail strike as it struggles to compete and its unemployment rate ranks as the fourth highest followed by Finland and Portugal. Finland has experimented with new welfare programs called a basic income plan and it has decided to not pursue it further. In many places in the EMU, things simply are not working. Germany is not one of them although Germany has its own issues.

The pressure of change

The EMU is under a lot of pressure. It is one of the reasons that the EMU is bargaining so hard with the U.K. There has been a fear in Europe that the U.K. opened Pandora’s box by allowing a referendum on EU membership. But now the EU has the Italian problem on its door step and it’s a problem made by the EU itself. And it’s one that will not go away. Historians may make the U.K. responsible for emboldening the Catalans in Spain and the Five Star Movement in Italy. And these events do help to explain why there is so much animosity in Europe toward the U.K. European leaders have been aware for some time of the grass roots opposition to what they are doing. Europe has simply not known what else to do. There is no plan B. With the Germans running the show, there would never be a ‘plan B’. There are only the rules and the need to capitulate to the rules. And that is why Europe is failing. It cannot bend with the times so it is at risk of breaking up.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief