Global| Aug 30 2017

Global| Aug 30 2017EMU Indexes Continue to Advance As Italy Joins the Parade

Summary

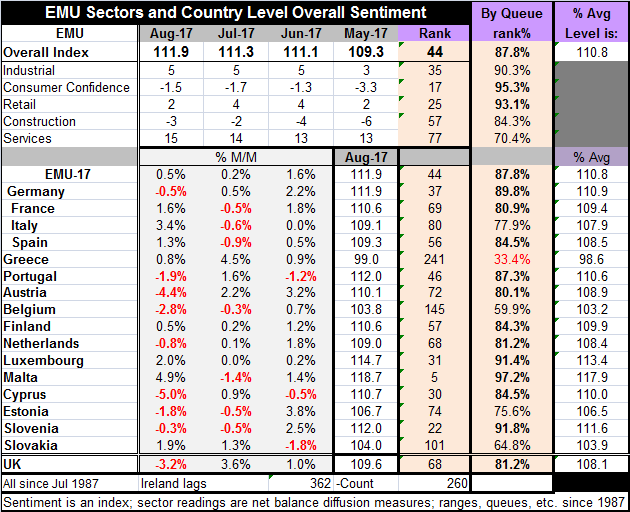

Perhaps the most surprising development this month is the sharp improvement in Italy's index. The overall EMU sentiment reading rose to 111.9 in August from 111.3 in July (a gain of 0.5%). The Italian gauge jumped by 3.4%, the second [...]

Perhaps the most surprising development this month is the sharp improvement in Italy's index. The overall EMU sentiment reading rose to 111.9 in August from 111.3 in July (a gain of 0.5%). The Italian gauge jumped by 3.4%, the second largest monthly gain by any member in the table this month (tiny Malta gained 4.9%). With its jump, the Italian queue standing leapt about 10 points to give Italy a queue standing reading comparable with the other four largest economies even though Italy's 77.9 percentile standing is still the weakest of the lot. It is not a lot weaker than France at 80.9%, but it is behind Spain at 84.5% and Germany at 89.8% and all of the EMU at 87.8%. Still, Italy is back in the pack.

Perhaps the most surprising development this month is the sharp improvement in Italy's index. The overall EMU sentiment reading rose to 111.9 in August from 111.3 in July (a gain of 0.5%). The Italian gauge jumped by 3.4%, the second largest monthly gain by any member in the table this month (tiny Malta gained 4.9%). With its jump, the Italian queue standing leapt about 10 points to give Italy a queue standing reading comparable with the other four largest economies even though Italy's 77.9 percentile standing is still the weakest of the lot. It is not a lot weaker than France at 80.9%, but it is behind Spain at 84.5% and Germany at 89.8% and all of the EMU at 87.8%. Still, Italy is back in the pack.

Monthly Changes

Out of the 16 reporting members eight saw setbacks this month. Among the four largest members only Germany weakened as it fell by 0.5%. Sharp losses were seen in Cyprus (-5.0%), Austria (-4.4%), Belgium (-2.8%), Portugal (-1.9%), and Estonia (-1.8%). Large gains were seen in Malta (4.9%), Italy (3.4%), Luxembourg (2.0%), and Slovakia (1.9%).

Current Standings

In terms of queue standings of the 17 reporting members, 12 have standings in their top 20th percentile (standings of 80% or higher). The exceptions are Italy (77.9%), Estonia (75.6%), Slovakia (64.8%), Belgium (59.9%), and Greece at (33.4%). On this basis, the ECBs policies have been relatively effective since 60% of these reporting EMU members have overall economic performance in the top 20th percentile of their historic ranges. That is a very respectable proportion. Another 17% have performance in the top 25th percentile of their respective historic queues of data. And only one country is below its median...Greece.

Compare to Unemployment Standings

However on an unemployment rate basis (on data updated through June of 2017) among the reporting 10 original EMU members, five still have rates of unemployment above their historic medians calculated back to 1991. Doing mostly poorly on this metric are Luxembourg, Italy, Austria, Portugal and France- all of which have unemployment rates above their historic medians. Doing best on the unemployment front are Germany, the Netherlands, Ireland, Finland, and Spain, each with an unemployment rate below its historic median. Recognize that these are in relative terms since Spain's 17.1% unemployment rate is quite high, but it is below its historic median. On a two month data lag, Greece stands with a high historic unemployment rate that is the 72nd queue percentile.

Apples and Oranges/Different Strokes

Interestingly, on a diffusion index gauge Europe appears to be quite solid even strong. But on a labor market gauge, it is much more varied and less successful overall. The U.S. has that in reverse. As its PMI gauges are modestly firm, but its unemployment rate gauges is especially strong. Japan follows a pattern more similar to the U.S.

The GDP Gauge

However, ranked on GDP growth rates since end 1997, eight of the original EMU members show that only two have growth rates near the top 10% of their historic queue of performance: The Netherlands (89.9%) and Portugal (88.4%). Italy also is in its top 30th percentile. Germany and France are in their top 40th percentile. Belgium and Finland are below their respective medians for the period.

Lessons?

One lesson from all this comparison shopping (done not using Google's site, the EU Commission will be glad to know) is that the diffusion surveys tend to give the highest scores. Jobs and GDP, more traditional statistical gauges are weaker.

Conclusion

This is a cautionary note about using surveys to make economic judgements. I think we would all agree that accounting style data (data that add up actual events like jobs or GDP or retail sales) are superior economic measures to any sort of diffusion index survey that essentially reports on breadth. The diffusion indices can be useful- even valuable- and I do use them myself. But we have to be careful to vet their message and to understand their intrinsic shortcomings. Right now the EU Commission's indexes are giving a more glowing assessment of conditions in the EMU than what is probably warranted. Beware.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief