Global| Aug 14 2020

Global| Aug 14 2020EMU GDP Registers Broad, Deep Recession

Summary

GDP data still are not in for all counties in Q2. But, for most, the data are in and have undergone some revision and are beginning to stabilize the picture. It is not a pretty one. All the European countries in the table had severe [...]

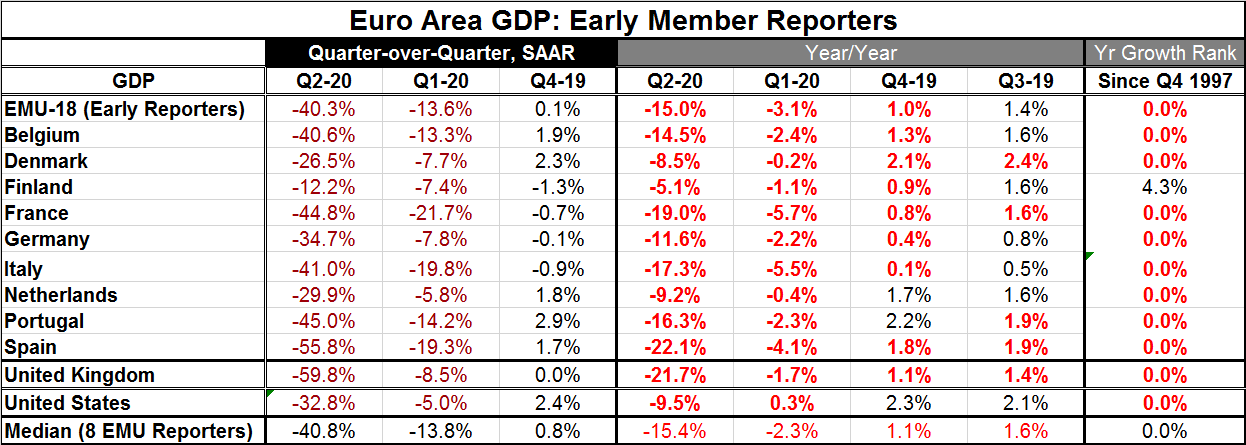

GDP data still are not in for all counties in Q2. But, for most, the data are in and have undergone some revision and are beginning to stabilize the picture. It is not a pretty one. All the European countries in the table had severe GDP declines in Q2 and all had GDP decline in Q1. That lays the groundwork for a recession call. Four countries Finland, France, Germany and Italy had GDP declines in Q4 2019 as well. Note the presence of many of the largest EMU economies in that mix. Despite that, the EMU as a whole squeaked out a GDP rise of 0.1%.

GDP data still are not in for all counties in Q2. But, for most, the data are in and have undergone some revision and are beginning to stabilize the picture. It is not a pretty one. All the European countries in the table had severe GDP declines in Q2 and all had GDP decline in Q1. That lays the groundwork for a recession call. Four countries Finland, France, Germany and Italy had GDP declines in Q4 2019 as well. Note the presence of many of the largest EMU economies in that mix. Despite that, the EMU as a whole squeaked out a GDP rise of 0.1%.

Recession severity

GDP is not simply falling in the most recent two or perhaps three quarters, but the fall in GDP is relatively severe. GDP is not just lower quarter-to-quarter, it is lower year-over-year for the EMU as well as for all eight the countries in the table; it is lower year–on-year in Q2 as well as in Q1 (except the U.S.). In Q4, growth was already decelerating everywhere except the Netherlands, Portugal and the U.S. All signs point to an encroaching weakness related to a pullback in international trade that was in progress before the virus struck out of the blue and sealed the case for recession.

About recessions

Recessions have three dimensions. To be a recession an economic downturn has to be (1) severe enough, (2) broad enough, and (3) last long enough. These three dimensions severity, breadth and duration are the key elements. If a downturn touches all those bases, it is a recession. Many use the metric GDP because it is the broadest measure of output in the economy. For severity, any decline in GDP will do. For length, two quarters are the usual minimum standard. By that metric, the EMU and all countries in the table satisfy the recession criteria. Countries often have statistical agencies or research houses that use more precise metrics since recessions are usually dated to begin and end by month; quarterly GDP data are insufficient for that task.

A strong start to recovery is likely, then...

The severity of the GDP decline in Q2 has an impressive impact on the year-on-year growth rates. Even with an extremely strong recovery in Q3 (which is likely), the year-on-year growth is going to remain negative in most countries in Q3. If recovery continues without backsliding, this recession may turn out to be very severe but only two to three quarters in length depending on the country. However, even with a jackrabbit start to the recovery in Q3 2020, the overall return to trend for GDP is likely to be an ordeal marking the recovery period as fretful. Recent recoveries from recession have been like that even when their recovery has not been so strong to start.

Recovery expectations in Germany

Germany, where the IFO just surveyed companies and turned in results saying that private sector firms expect a return to normalcy in about a year, has a different message from the Economics Ministry. The Ministry expects a strong recovery in Q3 but also expects a slower and extended process back to normalcy after that. The Ministry points to lagging growth abroad as a factor and notes that recovery will depend on the progress with the virus in Germany as well as abroad. Unlike the IFO’s private sector survey, it provides no timelines.

The uncertainty of the outlook is palpable

Policy is already providing as much thrust to growth as it can. But the virus undermines confidence and the way it is being dealt with is limiting recovery. If a vaccine is developed that is trusted, the recovery process might not just speed itself up but might also broaden itself. As long as the risk of contagion is in play, there are certain activities that will be on a banned or restricted list. Sweden has gotten around this by not fearing contagion except to the extent it might overwhelm its medical capabilities. A virus that spreads among a largely-healthy people, and does not kill them, or hospitalize them, is not much of a threat to society. This observation underlines how the obsession in much of the West with the spread of infection is off the mark. And the coronavirus has a very uneven impact on people depending on their state of health. Sweden, having allowed the virus to spread without imposing panicked lockdowns, has a broader incidence of infection; even there the spread of the virus seems to be slowing. If attitudes toward the virus change, perhaps to follow the Swedish model, and if Sweden continues to show progress, that also could impact the potential for recovery. On top of the usual economic effects, there are a lot of variables associated with the virus that come into play when making a forecast. We are best off being open minded about the potential for things to change. Quite apart from developing a vaccine we are learning a lot about this virus. The real question is how will we use what we have learned?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief