Global| May 15 2013

Global| May 15 2013EMU GDP Drops Again; Light at the End of the Tunnel?

Summary

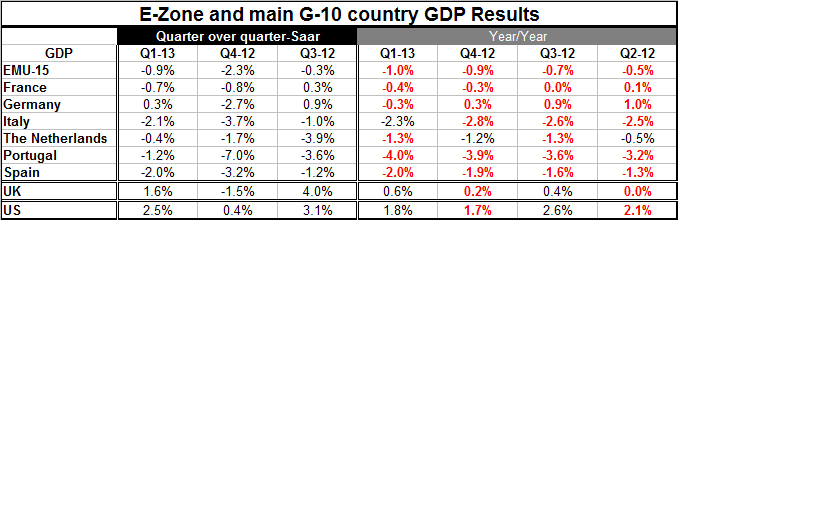

GDP growth in the European monetary union fell by 0.9% quarter-to-quarter expressed at an annual rate. This is a slightly reduced pace of decline compared to the -2.3% annual rate drop registered in the fourth quarter of 2012. Year- [...]

GDP growth in the European monetary union fell by 0.9% quarter-to-quarter expressed at an annual rate. This is a slightly reduced pace of decline compared to the -2.3% annual rate drop registered in the fourth quarter of 2012.

Year-over-year the rate of decline in GDP for EMU has accelerated to -1% from -0.9%. Quarterly, GDP in EMU has now declined for six-quarters in a row. Year-over-year growth has declined for five quarters in a row.

The table includes data from the early GDP reporters; among these six early-reporting EMU members only Germany has an increase in GDP in the first quarter of 2013. The UK, an EU member, also has GDP up by 1.6% after declining by 1.5% in the fourth quarter last year. For the past four-quarters UK domestic demand growth (Y/Y) has been leading the increases in GDP

Looking at year-over-year growth trends, year-over-year declines in GDP are in place for all six of these EMU member nations as well as in place for the EMU itself. The rate of decline of GDP in the first quarter 2013 indicates acceleration in the rate of decline for all members except Italy where the pace was reduced to -2.3% from -2.8% for year-over-year growth. Over the last four quarters for these six countries, plus the European Monetary Union itself, the GDP decline has been steadily accelerating with only three exceptions. Those are Italy in the first quarter of 2013, the Netherlands in the fourth quarter of 2012, and the Netherlands in the second quarter of 2012.

In the first quarter of 2013 the pace of the quarterly GDP decline abated for the EMU as a whole as well as in France, in Italy, in The Netherlands, in Portugal, and in Spain; while GDP actually increased in Germany after falling in the fourth quarter. This widespread reduction in the pace of the euro-wide GDP decline is good news and is somewhat consistent with the flattening out from the signals of the manufacturing and the services PMI indices. Still, this doesn't exactly make it a trend. In the fourth quarter the quarter-to-quarter GDP deceleration was greater than it had been in the third quarter for every country except the Netherlands. And, as we reported above, the year-over-year GDP declines are still accelerating every place except in Italy. The quarterly performance has not yet undone those trends.

The monthly metrics for consumer confidence, industrial activity, consumer spending, and the like, have not made a decisive move for the better. The best that we can say is that there are some indications that the monthly activity data have started to flatten out. In the case of Germany we've actually seen some evidence of gains for industrial new orders as well as manufacturing output.

Europe is still without banking sector reform and it continues to have severe problems with consumer confidence. A recent Pew poll that we reported on yesterday underscores how different Germany is from the rest of EMU members. Additional survey results in that poll also show how France is becoming more similar to the Mediterranean countries in Southern Europe and at the same time how France and Germany are growing to be more dissimilar.

There is evidence here of Europe approaching more of an end-game with its recession, but many problems remain. Were austerity to remain in force until these problems were solved the recession might go on and on for a number of member countries. However, it appears that as of the last G7 meeting that the yoke of austerity will be lifted to some extent. This fits in with the EU's decision to give countries like France an extension to reach its promised debt to GDP ratio, something that the economic commission announced before the G7 meeting.

Now we are simply unclear about what happens in Europe next. There remains a lot of work to do and while we can applaud the lifting of the severe austerity which has punished some of these countries, it's also clear that the countries that have been under the yoke of austerity need to continue to be watchful about government policies and need to make progress on improving private sector productivity.

I get the feeling that this is some kind of a turning point for the euro-Zone. I'm not quite able to put my finger on what it is. I'm convinced that the productivity and competitiveness differences that exist in the Zone are too great for it to simply generate growth and try to carry on. I'm not convinced that, with the yoke of austerity lifted, the countries that need to make more progress are going to do it on their own or that they are going to get much needed help to do it. Against that background it's not clear what a common banking union will mean for Europe given the diversity of problems faced by local banks. But it does look like there will be an end to what has seemed like this never ending down phase of the business cycle. We can only hope that the 'up-phase' will take us to some place that is not only better in the sense of having more growth but will put Europe on a road toward sustainability. If not, Europe will just find itself back in the same old soup.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief