Global| Mar 08 2013

Global| Mar 08 2013e-Zone Trade Trends and Other Trends: What They May Mean

Summary

If the e-Zone trade numbers are telling, and I think that they are, EMU is going nowhere fast. Exports across categories have fallen in EMU in December. The growth rates show export growth getting increasingly weaker over shorter [...]

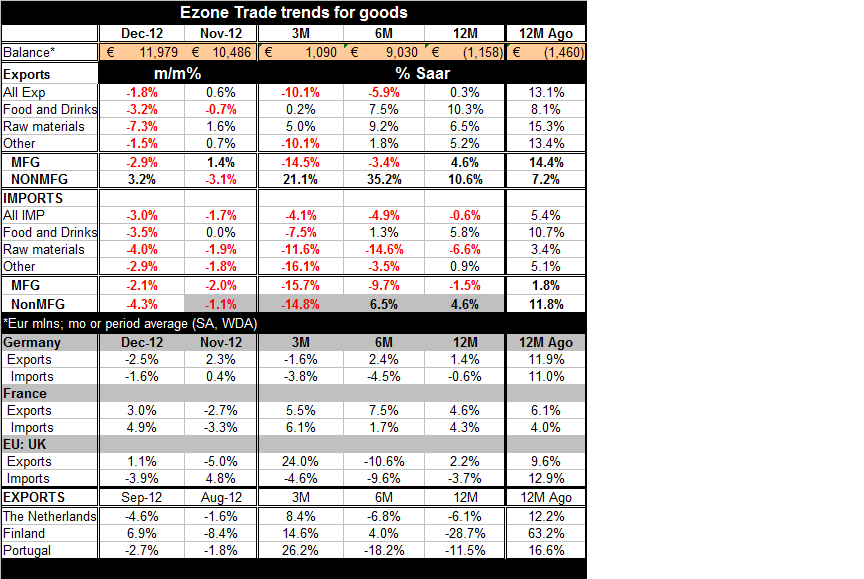

If the e-Zone trade numbers are telling, and I think that they are, EMU is going nowhere fast. Exports across categories have fallen in EMU in December. The growth rates show export growth getting increasingly weaker over shorter horizons. And that trend is even more extreme for manufacturing exports.

If the e-Zone trade numbers are telling, and I think that they are, EMU is going nowhere fast. Exports across categories have fallen in EMU in December. The growth rates show export growth getting increasingly weaker over shorter horizons. And that trend is even more extreme for manufacturing exports.

Imports fell more sharply than exports overall in December; for manufactures exports fell more sharply in December.

The table shows that import growth is more broadly weak and has been weaker longer than export growth in EMU over the past year. However, the deceleration, the change in the growth rate from one year ago, has been more severely negative for exports than for imports. The import change in growth has been -6% while for exports it has been -12.8% (subtracting year-over-year rates of growth for adjacent 12-month periods).

Imports like, other data, seem to show that France has bucked the trend of weakening. Imports, which tend to track domestic growth closely, have accelerated in France over the past three-months and are growing at a 6.1% annual rate. Other French reports show that France has been bucking the slowdown trend too slow until recently when some of the French reports, like its Markit PMI readings, have started to unravel fast. Either imports, too will start to show some sudden and sharp weakness or some past French data are likely to be revised weaker. Apart from France both the UK and German show import declines over three months and both show declines over 12-months.

We have a broader array of data for exports. German exports have just started to decline over the recent three months while UK exports have oddly picked up (but are still lower over six months, so this is probably just a bit of variability in the UK data). Both German and UK exports show weak nominal growth over 12-months. But, for the Netherlands, Finland, and Portugal exports are contracting over 12-months, even though each of these countries shows export growth over three-months.

Short term export growth can be fickle. But in the case of EMU the broader trends are quite clear. Both export and import growth are working their way lower. There is no evidence of any revival in domestic demand in the Zone as a whole or in its crucial overseas markets. Exports and imports both seem to have accelerated their downward move.

In Germany, while some data seem to show that the cascading negative impetus is losing momentum, other data do not. The PMI data a generally offer kinder treatment of Germany than do ordinary reports. Diffusion data, the type that PMI's are based on, can be very sensitive to shifts in economic growth rates.

In January German IP has gone flat. Its growth trends are on the mend, as the PMI data suggest, as IP is falling in Germany at a -1.2% pace over 12-months, a -5.3% pace over six months and that is converted to a 0.4% pace of increase over three-months. The decline in output is being arrested, But real German manufacturing orders are accelerating their drop from -2.1% over 12-mo, to a pace of -5.5% over six months and to -13.1% over three-months. Moreover, for Germany, orders explain over 80% of the variance in German year-over-year IP growth. It's not a good idea to set the German orders data aside.

So as we look at the Zone we can make a case for imports as charting a negative course for domestic demand in the Zone. Despite improving PMI data, there are question marks of some importance about Germany. Italy is embroiled in the kind of turmoil, rejecting austerity, that will have repercussions far and wide for the euro-Zone and yet NO ONE IS REACTING TO THAT.

DENIAL

It is much easier to sit home and sip your schnapps and assume that things will go back to normal when those crazy Italians simmer down. This Italy thing and the revival of Berlusconi is surely just a set-back, isn't it? Finding out that some Italians can say some 'good things' about Mussolini is just a passing phase. Or is it?

No one wants to confront the difficulties in the environment. It is easier and far more pleasant to see the US DJIA making new highs and to think that that signal is something good. But the Fed is purposely buying the safe assets to force the public to buy the more risky ones. Is this kind of propulsion usually good for the economy? In the end doesn't the use of artificial simulants catch up to you?

Meanwhile, the surprise from the US employment report for February is being ignored. Most want to look at the jobs headline and for this month alone-ignore that downward revision to January. But there is also a declining path in the growth rate of hours worked that is well entrenched in this same report. The only real job growth acceleration is from construction and in the month of February the shortest month of the year with the most holidays - that's not a reliable reading.

My message is to be careful what you choose to believe and what you filter out because you find it difficult to incorporate in your world outlook. If something does not fit in your world-outlook maybe you should change your outlook rather than to discard the piece of the puzzle that does not seem to fit. Increasingly there are more and more puzzle pieces that do not fit. If you find that happening maybe you are constructing the wrong picture.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief