Global| Mar 13 2009

Global| Mar 13 2009E- Area Retailing Remains Weak

Summary

The E-Area consumer remains under pressure and the retail sales picture reflects that. Even so, retailing is hardly the weakest sector in the Area. The output sector – factories- are much weaker. Exports are much weaker. Retail sales [...]

The E-Area consumer remains under pressure and the retail

sales picture reflects that. Even so, retailing is hardly the weakest

sector in the Area. The output sector – factories- are much weaker.

Exports are much weaker. Retail sales growth remains negative but the

three-month growth rate for sales shows less of a decline than for

six-months. The slowdown in retail sales actually is dissipating its

momentum even as European unemployment climbs and the recession

spreads. Since retail sales component data are not available through

the current month the trends for the components through December are

the most current: they show considerably more weakness.

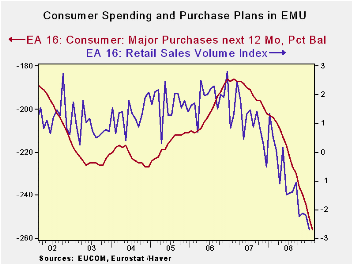

Consumer sentiment is weak and falling across the Area. It

would be a surprise if there was much recovery for the consumer in the

coming months as unemployment continues to rise. Spending plans by

consumers (see chart) continue to be cut to extremely low levels.

European ‘stimulus plans have not been targeted at the consumer

although they could be expected to help provide some buffering.

| Ezone (15) Retail Sales Volume | |||||||

|---|---|---|---|---|---|---|---|

| Jan-09 | Dec-08 | Nov-08 | 3-Mo | 6-MO | 12-Mo | ||

| Zone-15 Total | 0.1% | -0.3% | -0.1% | -1.4% | -2.6% | -2.7% | |

| Food | #N/A | -0.3% | -0.1% | -4.5% | -1.4% | -2.0% | |

| Non-Food | #N/A | -0.4% | -0.4% | -7.1% | -2.5% | -2.5% | |

| Textiles | #N/A | -0.6% | -0.6% | -16.0% | -2.8% | -3.0% | |

| Books news, etc | #N/A | -0.5% | -1.9% | -11.8% | -5.2% | -4.4% | |

| Pharma | #N/A | -0.1% | 0.1% | -2.2% | -0.4% | 0.2% | |

| Other NonSpec | #N/A | -1.2% | 0.2% | -4.2% | -2.8% | -3.8% | |

| Mail Order | #N/A | 3.9% | 0.0% | 8.0% | 9.4% | 3.4% | |

| Country Detail; Volume | |||||||

| Germany: Volx Auto | -0.6% | 0.5% | 0.0% | -0.4% | 0.0% | -1.3% | |

| Italy (Total; Value) | #N/A | 0.0% | -0.4% | -2.9% | -1.1% | -1.5% | |

| UK (EU): Vol | 0.8% | 1.6% | 0.3% | 11.3% | 6.7% | 3.6% | |

| Shaded areas calculated on a one-month lag due to lagging data | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief