Global| Sep 30 2008

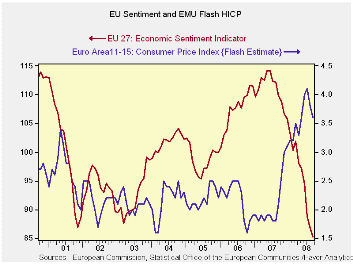

Global| Sep 30 2008CPI Soars as EMU Sentiment Tubes: Price Relief is Minor

Summary

Headline is turning sharply in a favorable direction; core remains high and ‘sticky’ In one of my favorite comedy skits of all times Dan Aykroyd of the US TV show “Saturday Night Live” was imitating Jimmy Carter at the height of the [...]

Headline is turning sharply in a favorable direction; core remains high and ‘sticky’

In one of my favorite comedy skits of all times Dan Aykroyd of the US TV show “Saturday Night Live” was imitating Jimmy Carter at the height of the US inflation bubble. He launched his ‘inflation is your friend’ skit urging people (while imitating Carter) to enjoy wearing $1,000 suits and living in million dollar houses and smoking $100 cigars. It was a great skit. But the view does not reflect the realities of policy.

Since those days central banks have made it a real business of stamping out inflation. But when oil prices spurt it is hard to keep a lid on inflation. Oil is just too important and people do not substitute away from it with enough vigor to damp its impact on overall prices. Central banks that target headline inflation or pose ceilings for it, have had their heads handed to them.

In the US the Fed has been criticized for its focus on CORE inflation (since people live in a headline inflation world) but, in the event, core inflation has been much more on track with the Fed’s professed comfort zone (not a formal target). And that eventually builds credibility.

In Europe the core rate is at 2.3% over three months and six months (lagged since we do not have the core yet for September) it is in improving shape even as it is at 2.6% Yr/Yr. That’s still a percentage point better than (up-to-date) headline inflation. Had Europe focused on this rate it would regard inflation as closer to the target. Instead, while headline inflation is decelerating (0.7% annual rate over three months) it is still running at a tortuous 3.6% Yr/Yr pace that is light years away from a 2% ceiling, tying the hands of the central bank.

I am not suggesting a shift to an ‘inflation is your friend’ monetary policy. But in targeting headline inflation the ECB has boxed itself in. It is not able to be preemptive and will only be able to cut rates once economic weakness is clearly in train and that will make the hammer of economic downturn hit harder.

When this is all over the ECB would do well to reconsider what

it targets. As a general rule it makes no sense to target something you

cannot hit or will not hit. And a headline inflation rate of 2% ‘MAX’

with oil prices moving as they have is something no central bank in the

world would try to hit. Europe needs to do some re-thinking to avoid a

policy re-stinking.

| Trends in EMU HICP; Flash Index | |||||||

|---|---|---|---|---|---|---|---|

| % mo/mo | % saar | ||||||

| Sep-08 | Aug-08 | Jul-08 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | |

| EMU-13 | 0.1% | -0.1% | 0.2% | 0.7% | 2.4% | 3.6% | 2.1% |

| Core | #N/A | 0.3% | 0.1% | 2.3% | 2.3% | 2.6% | 2.0% |

| Goods | #N/A | -0.4% | -0.9% | -3.4% | 4.0% | 4.6% | 1.2% |

| Services | #N/A | 0.3% | 0.9% | 6.0% | 4.3% | 2.7% | 2.6% |

| HICP | |||||||

| Germany | 0.2% | -0.2% | 0.4% | 1.5% | 2.1% | 3.0% | 2.6% |

| France | #N/A | -0.2% | 0.1% | 1.4% | 3.0% | 3.5% | 1.3% |

| Italy | -0.2% | 0.4% | -0.1% | 0.4% | 2.2% | 3.7% | 1.8% |

| UK | #N/A | 0.5% | 0.4% | #N/A | #N/A | #N/A | 1.7% |

| Spain | #N/A | -0.1% | 0.4% | 3.5% | 3.8% | 5.0% | 2.2% |

| Core:xFE&A | |||||||

| Germany | #N/A | 0.3% | 0.3% | 2.7% | 1.7% | 1.9% | 2.3% |

| Italy | #N/A | 0.7% | -0.2% | 3.4% | 3.2% | 3.2% | 2.0% |

| UK | #N/A | #N/A | 0.3% | #N/A | #N/A | #N/A | 1.8% |

| Spain | #N/A | 0.3% | 0.3% | 3.8% | 3.0% | 3.5% | 2.6% |

| Blue shaded area data trail by one month. | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief