Global| Jun 29 2007

Global| Jun 29 2007Construction Spending Up 0.9% in May, Much Better Than Expected

Summary

New construction put-in-place surged by 0.9% in May, following 0.2% in April and 0.1% in March. This was the best performance since February 2006 and compared with Action Economics' forecast survey that called for just 0.1%. This [...]

New construction put-in-place surged by 0.9% in May, following 0.2% in April and 0.1% in March. This was the best performance since February 2006 and compared with Action Economics' forecast survey that called for just 0.1%. This month's report includes annual revisions of the construction data; besides the usual seasonal adjustment changes, a new sampling procedure is being used for public construction projects. Other alterations were made. As seen in the first graph, the net result is a downward shift in construction spending in the most recent months, with April lower by 2%, although the peak in early 2006 is now seen to be somewhat higher than before.

Residential building continued its contraction, although May's 0.8% decrease and April's -0.4% were not as bad as many recent months. This sector has declined continuously beginning in March 2006 and the monthly shrinkage has averaged 1.6%. So, indeed, April and May definitely look "less bad" with their smaller losses. Among types of residential construction, multi-family eked out a 0.3% increase in May and home improvements were flat after a 0.9% rise in April. These helped steady the sector even as single-family home construction weakened somewhat to a 1.4% decline after two smaller monthly reductions.

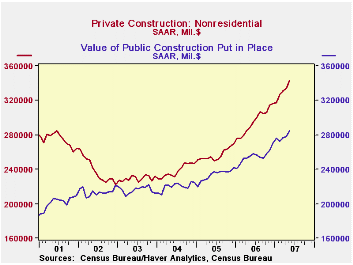

Private nonresidential and public construction both had impressive gains in May: 2.7% and 2.2%, respectively. And both have been strong for some time. Public construction has been up in 7 of the last 8 months, particularly at the state and local level. Private nonresidential has seen only 1 decrease since the middle of 2005. The wide range of building and structure types and uses probably helps this latter strength. Office building, for example, has slowed, but it is offset currently by advances in amusements and recreation. The biggest year-to-year growth is in hotel construction, up a whopping 65% over May 2006. There have been uptrends recently in communications and transportation. Health care and education spending, by contrast, are slowing.

These construction put-in-place data are in Haver's "flagship" USECON database. "Old" data, prior to the latest annual revisions, is in USARC07. The forecast of the monthly headline number comes from ASREP1NA, which includes Action Economics weekly forecast surveys and each indicator's initially reported figure for each period.

| Construction Put-in-Place | May 2007* | Apr 2007* | Mar 2007* | Year/ Year | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|---|

| Total | 0.9 | 0.2 | 0.1 | -3.2 | 5.3 | 10.6 | 11.1 |

| Former | -- | 0.1 | 0.6 | -- | 4.7 | 10.5 | 11.6 |

| Private Residential | -0.8 | -0.4 | -1.3 | -17.7 | 0.0 | 13.5 | 18.7 |

| Private Nonresidential | 2.7 | 0.9 | 1.4 | 18.2 | 15.2 | 7.6 | 4.0 |

| Public | 2.2 | 0.6 | 1.6 | 12.8 | 9.0 | 6.3 | 1.9 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief