Global| Apr 20 2016

Global| Apr 20 2016Biggest Year-on-Year German PPI Drop Since Jan 2010 Raises Questions

Summary

As we look at the weakest year-on-year German PPI drop since January 2010 -over six years ago- we are now deeper into a recovery and price conditions are worsening. There is some sort of lesson there. I am reminded of Gilda Radner's [...]

As we look at the weakest year-on-year German PPI drop since January 2010 -over six years ago- we are now deeper into a recovery and price conditions are worsening. There is some sort of lesson there. I am reminded of Gilda Radner's `It's always something.' I am next reminded of inspector Clouseau, of Pink Panther, fame who used to say `...and I do not know what I do not know.' Later Peter Sellers who played Clouseau, played the role of Chance Gardener in `Being There' and said such simple things that they were thought to be cryptic descriptions of the economy. He was mistaken as a financial genius instead of the simple man he really was. All of these observations offer topical lessons to us in our own strange economic days ahead. First of all, Gilda was right: `it's always something' and you can't always guess what it will be. Second of all, we don't know what we don't know and we should be very careful when some central banker who doesn't know more than we do offers to lead us through the mine field with us going first - of course. Thirdly, there is a lot of advice being given that masks as sage when it is not so. Be careful to vet financial advice for its ideology or simply for the sweet fragrance of fertilizer.

As we look at the weakest year-on-year German PPI drop since January 2010 -over six years ago- we are now deeper into a recovery and price conditions are worsening. There is some sort of lesson there. I am reminded of Gilda Radner's `It's always something.' I am next reminded of inspector Clouseau, of Pink Panther, fame who used to say `...and I do not know what I do not know.' Later Peter Sellers who played Clouseau, played the role of Chance Gardener in `Being There' and said such simple things that they were thought to be cryptic descriptions of the economy. He was mistaken as a financial genius instead of the simple man he really was. All of these observations offer topical lessons to us in our own strange economic days ahead. First of all, Gilda was right: `it's always something' and you can't always guess what it will be. Second of all, we don't know what we don't know and we should be very careful when some central banker who doesn't know more than we do offers to lead us through the mine field with us going first - of course. Thirdly, there is a lot of advice being given that masks as sage when it is not so. Be careful to vet financial advice for its ideology or simply for the sweet fragrance of fertilizer.

When it comes to oil, no one knows what is going to happen. OPEC destabilized the global economy when it was formed in the early 1970s as producers banded together to raise oil prices mightily. And while it currently lacks the grasp of oil supplies it once had, it influences enough supply to be a wild card in oil politics and economics. And with so many important members perched as they are the Middle East, there is no telling what happens there next. Saudi Arabia's current obsession is much more over Iran than even the price of oil as we saw at Doha where the Saudis put their strife with Iran ahead of their oil price stabilization goal.

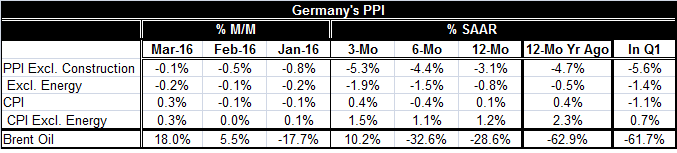

We profile Brent oil prices in the table to track what is going on in global oil prices as German PPI prices fluctuate. Clearly a lot of what has happened with the PPI has weak oil prices at its root. The German PPI is down by 3.1% year-over-year in March as the Brent price fell by 28.6% over 12-months. And as Brent prices rose in the months of February and March the German PPI continues to drop. German PPI trends are still lower; for the CPI prices are more stable but still low.

With a failed Doha meeting behind us and oil again getting weak as the temporary effect of a local strike in Kuwait fades on global oil prices, we could be looking at another down leg in oil prices. And with that renewed downward pressure could emerge on German as well as global PPI price trends.

The upshot is that we are still in an underperforming weak price environment. We cannot be sure that it is getting better.

Central bankers are planning for normalization. But are they right? They have been wrong so far. Every central bank that has embarked on a post financial crisis tightening has had to unwind it or put it on pause. Could this just be another Samuel Beckett play in the making? This time it's about a group of central bankers sitting around waiting for an event that will not happen instead of waiting for Godot, who will never show up?

One thought is that deflation is an oil and commodities price phenomenon. And it is surely that. But is that the exclusive issue here? There is also excess supply in the global economy and that means goods are in surplus supply and that will keep downward pressure on prices quite part from pressures on `costs.' Japan has had years of deflation without low or falling energy prices `to blame.'

Of course, there are lags in the deflation process, but Germany did not see an increase in producer prices when Brent rose for two months in row in February and March. True, the German PPI price only fell by 0.1% in March. But ex-energy price trends are still very weak and weakening.

We, like policymakers, need to keep our eye on the ball as the batter hits it rather than on the expected trajectory based on his batting average. The baseball analogy is apt. It may be smart to guess that a hitter will perform according to his average and hit home runs according to his `average.' But batters have slumps. Some players have extreme slumps. You can never know for sure what will happen so it is important to look at what really does happen, not just at expectations. In economics, we have less to go on than a batting average. And economists -even at our central banks -are burdened by their ideologies which simply may not be suited for these times (Imagine handicapping a game where every announcer thinks the batter has a different batting average). Everyone is assuming that some sort of `mean reversion' is going to occur. But revert to what? What if it takes two more years for it to happen if it happens at all? What if the world has changed? Remember at Jackson Hole Wyoming this year at the yearly K.C. Fed meeting, our knowledge of the inflation process was soundly taken to task as all approaches were found wanting. Yet we have this belief in mean reversion. How badly could policy misstep in the meantime, especially if this belief is wrong?

We need to realize that central bankers are fallible. They may speak cryptically like the Oracle at Delphi or even like Chance Gardener, but they are still fallible. They make policy based on some old fashioned homilies like `leaning against the wind', `taking away the punch bowl before the party gets into full swing,' also using highly technical models and ideas. The Germans have been successful running a policy of keeping inflation at or below 2% and not worrying about how low it gets. But are these policies right for the global economy today when demand is weak leverage is still high crimping consumption and when production exceeds consumption? Fiscal debts are high enough to have kept fiscal policy on the sidelines and maybe that has been the case for too long. How similar is out current time to the previous 50 years?

I suspect the real problem has been the growing need for international monetary reform because too many countries are just trying to game the system by siphoning off domestic demand from Western nations especially the U.S. Too much has been siphoned off and now it's more like excessive bloodletting. Several political candidates in the U.S. are running on such a platform but without a clear plan or remedy or with flawed or controversial `remedy.' There can be no doubt but that this system of fluctuating exchange rates did help us to get through the oil price shock and helped an emerging market like China to create growth more rapidly that it could have otherwise (under a fixed rate system). But when will show if it is able to support ongoing viable commerce with balanced payments conditions among its participants engaged in fair trade. Is that possible? And will change come about without pointed action to bring it about? I doubt it; something always gets in the way. It's always something.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief