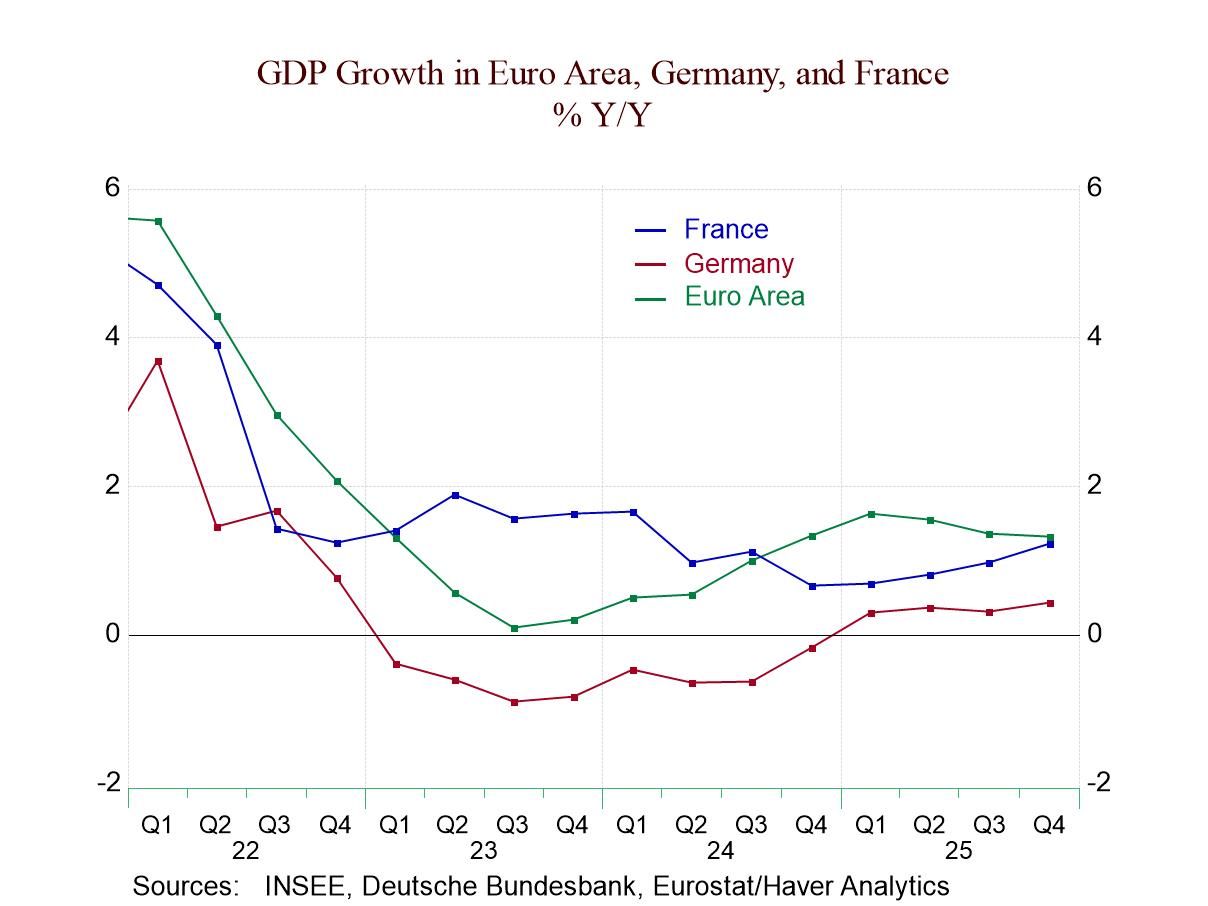

Weak GDP Growth in Europe and Selected Countries Carries On

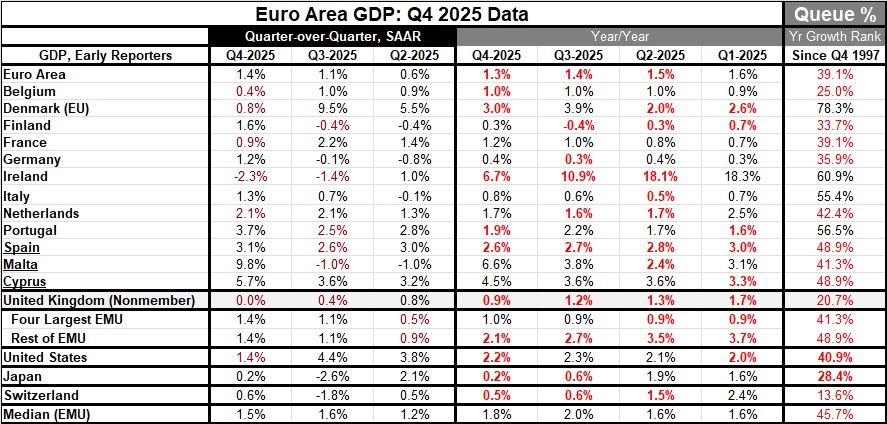

More countries have reported new results or firmed up their GDP results for 2025Q4. In the EMU, GDP grows by 1.3% year over year in the fourth quarter. The large EMU economies (Big Four) grow by 1% on that horizon, while the rest of the community grows at twice that pace, at 2.1%. U.S. growth on that timeline is 2.2%; Japan’s is 0.2%; and the United Kingdom grows by 0.9%. They are all weak compared to past standards. None of them rank at or above their respective 50th percentile standings on growth rates dating back to 1997.

In Europe, EMU nonmember Denmark’s growth at 3% has an over 50th percentile ranking, at 78.3 percentile mark. Ireland’s growth has a 60.9 percentile standing, while Italy and Portugal have growth rates near their respective 55th percentiles—above their respective medians but not by a lot.

The bigger they are, the slower they grow... Within the EMU, it is a durable finding that the smaller economies are growing faster than the larger ones. The good news here is that inflation seems to be really much more controlled and near to the target on a relatively broad basis. Headline inflation is broadly close to 2%, but core inflation rates are more stubbornly elevated. For now, the European Central Bank seems content to hold the line on inflation here. That decision is good for growth prospects. This may be because it can see that the community it services has some very different needs. And rather than holding the community’s feet to the fire to get inflation and core inflation to 2%, it has decided to allow some temporary overshooting and a longer glide path to 2%. This has been the U.S. strategy that is now coming under fire. The ECB may have adopted the charts and original targets of the old independent Bundesbank, but EMU-wide policy under the ECB looks very little like Germany policy used to when the Bundesbank results called the shots. This sort of overshoot would not have been tolerated and would not be ‘encouraged to live on’ with the compliant conduct of current policy. But then the ECB has this broader mandate of serving a huge area and with members that are not as inflation-fearing as Germany.

European nations generally have budgetary issues. Germany has been budget-careful. But its preference to pay down debt and stiff the U.S. on its request for Germany to put more money into NATO does not play well in retrospect. It has preserved some fiscal space for itself, and its fiscal house is very much in order…unlike France and nonmember U.K. who both are making policy under fiscal constraints.

For now, GDP growth is cruising along, and the EMU is logging weakish, tolerable, results. The big news so far is that growth has been enough to keep unemployment at an extremely low level. In some sense, the speed of GDP growth does not matter; it is anachronistic at least in the sense that what people think is good or enough draws from past experience, while the unemployment rate is a very here-and-now variable that might be affected by very different circumstances. Going ahead, there is a question of whether AI will be taking job growth away; it is a concern that is more advanced in the U.S. right now than in Europe. But it is still a nagging fear.

Still, we do not hear a lot of complaints about growth rates because the policy filter on GDP growth is employment growth and the unemployment rate. So far, those bells are not ringing out any warnings. So far...

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global