US Inflation: the Fed has more work to do

by:Ethan Harris

|in:Viewpoints

The surge in inflation in March is likely to be repeated in April and will continue as long as the Straits of Hormuz remains closed and energy inventories get tighter and tighter. The FOMC and its prospective new Chair have some work to do if they want to restore the Fed’s anti-inflation credibility.

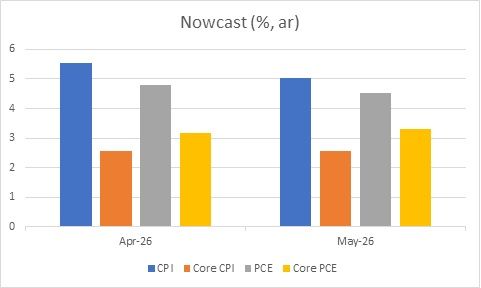

The Cleveland Fed publishes a “nowcast” for the next CPI and PCE inflation releases. For the core they simply extrapolate the recent trend. However, for food and energy they look at actual daily data and hence they get a good estimate of what headline inflation will look like.

https://www.clevelandfed.org/indicators-and-data/inflation-nowcasting

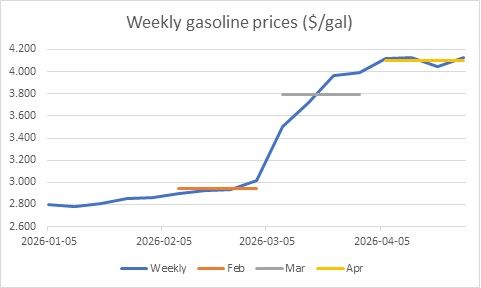

Recall that the consumer price survey is taken over the course of the month. Hence it reflects average prices rather than end-of-month prices. This is important today because food and energy prices rose over the month of March. Hence as the chart below illustrates, the CPI for gasoline will be higher in April than in March.

Source: U.S. Energy Information Administration

The chart below shows the nowcast for annualized April and May inflation. For both months the headline measures are running at about 4.5-4.5% and the cores are in a 2.5 to 3.3% range. The cumulative overshoot for the PCE since 2021 is 11% and rising.

Source: FRB Cleveland

Fed forgiveness

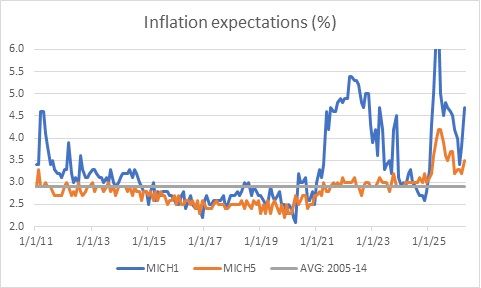

And yet, the Fed seems to be in a forgiving mood. There is a dovish asymmetry in the way the Fed has responded to under- and over-shooting its target. In 2015-20 inflation was persistently below target. As the chart below shows, this caused inflation expectations to dip below the 2005-14 average, a period of on-target inflation. The Fed was worried about an “unanchoring” of expectations to the downside. Hence, in their new 2020 “Framework” they adopted “inflation averaging,” explicitly seeking average inflation of 2% over time. Consistent with this, they sought a modest overshoot of the target to make up for some of the prior undershooting, nudging inflation expectations back to normal.

Source: University of Michigan

Now the Fed faces the opposite problem—an even bigger overshoot to the upside along with a rise in survey measures of inflation expectations. In response, in the 2025 Framework, the Fed dropped inflation averaging. This confirmed that they were not seeking a modest undershoot of the target, but only trying to return to target. The cumulative overshoot was treated as water under the bridge. As I pointed out at the time the shift made it appear that 2% was now a floor, suggesting inflation would average more the 2% over the long term.

What will Warsh do about it?

Kevin Warsh’s harshest critique of the Powell Fed is that it allowed inflation to run out of control so long that it seriously damaged its anti-inflation credibility. He argues that this failure is the real threat to Fed independence (not political pressure or threatening to put Fed officials in jail).

Warsh also argues that he is the man to restore the anti-inflation credibility of the Fed. What would that mean in practice? In the current context that means having a hawkish bias in several key respects:

• As I suggested above, seek to return inflation to target ASAP and ideally modestly undershoot the target. • Focus more on the inflation risks from the energy price shock than on the growth risks. Both risks matter, but this latest surge in prices could be the final straw in the unanchoring of inflation expectations. • Look at a range of measures of core inflation rather than zero in on the currently softest core metric, the trimmed mean. • Don’t wait for a potential productivity surge to solve the inflation problem. Make sure policy is tight enough to lower inflation on its own. If the productivity surge happens, the Fed can ease, but also let the productivity surge (and lower unit labor costs) lower inflation modestly below the target. • Be sure to start shrinking the balance sheet before cutting rates to avoid a short-term easing. • Finally, “caucus” with the three FOMC hawks who argue for a symmetric rather than a dovish directive.

Unfortunately, Warsh has not discussed any of these concrete steps as part of his “reform” agenda. Indeed, most of his commentary in the last year suggests he will join Governor Miran as an “uber-dove.”

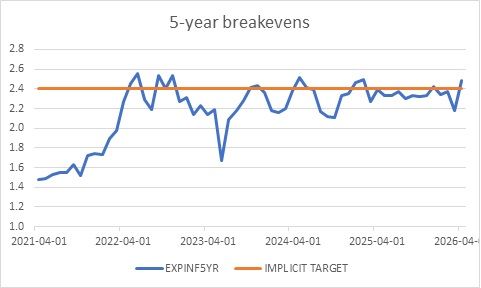

The bond market is not concerned about inflation. It continues to price in a quick return of inflation to target. For example, 5-year inflation “breakevens” continue to bounce around the implicit 2.4% target for the CPI (chart). I hope the market is correct, but I continue to see upside risks to both breakevens and nominal bond yields. The Fed and its prospective Chair have some work to do.

Source: FRB Cleveland

Ethan Harris

AuthorMore in Author Profile »Ethan Harris has a Ph.D. in Economics from Columbia University and was the Head of the Domestic Research Division at the NY Fed. He was Chief US Economist at Lehman Brothers from 1996 to 2008 and Head of Global Economics at Bank of America from 2009 to 2023. Currently he is the author of the blog Ethan on the Economy.

Global

Global